- Skip to primary navigation

- Skip to main content

- Skip to primary sidebar

- Skip to footer

Diabetes Travel Insurance Guide

Modified: Jun 17, 2020 by Lianne Fachetti, ABA · This post may contain affiliate links ·

Let’s face it, traveling can be a nerve-wrecking experience. There are so many uncertainty factors that can occur and leave you stranded in a very undesirable situation. As a diabetes patient, you have even more to worry about other than catching the next flight, hoping they have your diabetic meal ready, and praying that your luggage will safety arrive at the destination ready for pickup.

You have to worry about how to handle unforeseen health problems that may arise during flight or while you are at your destination. But worrying can only cause unwanted stress and fluctuation of your blood level. Instead of spending the time to worry, why don’t you spend the time to better plan and prepare for your trip.

In this article, we will discuss about why it is a great idea to invest in a travel insurance in the first place. We will explain how your current Medicare plan policies are extremely limited regarding to foreign location health coverage, and why your Medigap supplement plan is simply insufficient for traveling emergency expense needs. We will introduce you to a list of insurance companies that are willing to overlook diabetes as a pre-existing condition, and provide you with three best policy choices in our opinion.

And to help you lower your insurance cost, we have provided you with some alternative options and suggestions that may be overlooked. We hope that by providing you with various solutions, you will be looking at traveling and travel health insurance at a new angle.

Reasons to Buy Travel Insurance

Do you really need travel health insurance, medigap isn’t for everyone, an overview of medigap plans, thediabetescouncil top 3 choices for travel insurance, what other options do i have.

One of the ways to ease your distress is to get yourself a travel insurance policy. By simply paying for the service ahead of time, you can end up saving a lot of money and easily resolve numerous traveling nightmares such as:

- You missed your flight or your flight has been canceled

- Your bags are lost and your medication is in it. You now need an emergency prescription

- Your wallet and passport are missing, and you need emergency cash and a replacement passport.

- You are in an accident and there is no adequate medical

- You need to cancel your trip due to illness, sudden emergency events or work complication

- Your cruise line, airline, or tour operator goes bankrupt, and you are stranded at your destination

- You have a medical emergency at your travel destination

- A terrorist attack occurs where you are planning to visit, and you wish to cancel your trip

- Sudden weather forces you to evacuate from your destination

I also recommend reading these related articles:

- Can Diabetes Bankrupt a Country?

- The Growing Impact of Diabetes

- Quality of Life: Privileges, Benefits, Rights?

- Everything You Need To Know About Traveling With Diabetes

- Can Diabetes Type 2 Be Reversed? Experts Answer

The answer is YES . For all the current Medicare diabetes patients who are not enrolled in Medigap Plans that cover foreign travel medical emergency services, Medicare will not pay for health care or supplies you get outside the United States.

The definition “outside of United States” means any place other than the 50 states of the United States, the District of Columbia, Puerto Rico, the U.S. Virgin Islands, Guam, American Samoa, and the Northern Mariana Islands. However, there are 3 exceptions to the rule that would allow you to receive coverage outside of United States under the Medicare Part A and Medicare Part B.

- You are in the United States when you have a medical emergency, and the foreign hospital is closer than the nearest United States hospital that can treat your illness or injury.

- You are traveling through Canada without unreasonable delay by the most direct route between Alaska and another state when a medical emergency occur, and the Canadian hospital is closer than the nearest United States hospital that can treat your illness or injury. Medicare determines what qualifies as “without unreasonable delay” on a case-by-case basis.

- You live in the United States and the foreign hospital is closer to your home than the nearest United States hospital that can treat your medical condition, regardless of whether it is an emergency.

And same as the policy applied to services in the United States, Medicare will only pay for the Medicare-covered services you receive in a foreign hospital. You will be responsible for any other treatments or medication you receive that are not covered by Medicare Part A and Part B.

Medigap sounds like the perfect solution for securing a traveling insurance. However this standardized supplementary plan isn’t available to everyone. In some States, the law requires that you must be at least 65 years old to qualify for the supplement plan.

Other States has made it a legal right for you to obtain at least one kind of Medigap coverage before you reach age 65. Here is the list of the States that will allow the enrollment of Medigap ( please note that there are specific restrictions to certain States ):

- California (excluding those under 65 and with end-stage renal disease)

- Connecticut

- Delaware (only available to those with end-stage renal disease)

- Massachusetts (only available to those with end-stage renal disease)

- Mississippi

- New Hampshire

- North Carolina

- Pennsylvania

- South Dakota

- Vermont (excluding those under 65 and with end-stage renal disease)

Depending on which Medigap Plan you have already enrolled in, you may be covered for any medical expense you have incurred in your travels.

The Medigap plans that includes foreign travel emergency service will pay 80% of the billed charged for covered services outside the United States after you meet a $250 deductible for the year. There is one exception; Plan F also offers a high-deductible plan.

If you choose this option, this means that you must pay for Medicare-covered costs up to the deductible amount of $2,180 in 2016 before your Medigap plan starts paying for anything. For all these Medigap plans, the foreign travel emergency coverage has a lifetime limit of $50,000 .

Please note that if you live in Massachusetts , Minnesota , or Wisconsin , you have a different standardized Medigap policy.

- Massachusetts:

Massachusetts’s Supplement 1 Plan covers foreign travel emergency.

The basic Medigap plan will cover 80% of your foreign travel emergency expense. And the Extended Basic Medigap Plan will cover 80% of your foreign travel emergency expense until you reach the $1,000 out-of-pocket cost for the calendar year. Afterwards, the plan covers 100% your foreign travel emergency covered services expense.

Plans known as "50% and 25% Cost-sharing Plans" are available. These plans are similar to standardized Plans K (50%) and L (25%). A high-deductible plan ($2,000) is also available. These policy will cover foreign travel emergency.

Lifetime Limit of $50,000 Is Not Enough

$50,000 really will not cover all the medical expenses should an emergency situation occurs. To give you a simple example, if you travel from California to British Columbia, Canada where you are faced with an emergency medical situation and require hospital care, one single night at the hospital will cost $100.

But with the medication and equipment use, you will need to pay much more than $100 per day depending on your needs. Instead of staying in Canada for the treatment, if you wish to fly home to California for the treatment, the special arrangement can easily be upward of $15,000.

This whole ordeal will quickly drain your lifetime limit and you will have to pay all the excess expense out of your own pocket. Afterward, you can never tap into the foreign travel emergency coverage ever again.

How does Pre-Existing Waiver Work?

Instead of relying solely on Medicare, there are many insurance companies that specialize in traveling insurance. Many will deny coverage for individuals with pre-existing conditions or exclude any claims related to the pre-existing condition.

But there are there are some companies that will cover medical expenses relative to your diabetic condition by offering a waiver. Depending on the insurance company, your pre-existing diabetes condition can be waivered if you fulfill these requirements:

- You must insure at least your trip’s full prepaid non-refundable cost (some companies do not require you to insure the full prepaid trip cost, but you still need to put down a deposit),

- Depending on the insurance company, you must get your policy within the limited days after you pay your earliest trip payment ,

- You must cover your trip’s full length, and

- You must be healthy enough and be able to take the trip on the set date. (If you insist on traveling against your doctor’s advice, the insurance company has the right to cancel your policy or refuse to cover your claims.)

Another factor you have to consider is the “ Lookback Period ” policy of the insurance company. In order to waive your pre-existing condition, you must have proof that your condition is “stable”. According to the policy definition, “stable” means that the person with the pre-existing condition has not already taken a turn for the worse, and not in a state where any changes are foreseen, known, or expected that could cause the person to “take a turn for the worse”. Depending on the company, the Lookback Period can be 60, 90, 180, or even 365 days prior to the travel insurance policy’s effective date.

According to the policy definition, “stable” means that the person with the pre-existing condition has not already taken a turn for the worse, and not in a state where any changes are foreseen, known, or expected that could cause the person to “take a turn for the worse”. Depending on the company, the Lookback Period can be 60, 90, 180, or even 365 days prior to the travel insurance policy’s effective date.

List of Insurance Policies that Includes Pre-Existing Waiver:

#1 Top Choice: CSA Travel Protection Custom Luxe

The company will waive the pre-existing conditions provided that you meet the following requirements:

- Coverage is purchased prior to or within 24 hours of your final trip payment,

- You are medically and physically able to travel at the time the coverage is purchased, and

- You insure 100% of your prepaid trip costs that are subject to cancellation penalties or restrictions

CSA Travel Protection is easily the top choice as they are the only traveling insurance company that allows the purchase of a policy within 24-hour of final trip payment date. Even though the company requires that you have to pre-insure your trip cost in case of trip interruption (their trip interruption coverage is 175% of trip cost), you can claim the cost as $0 if you are willing to go without cancellation or trip interruption coverage. If you do decide to purchase the policy ahead of time, you have a 10 day free look period. Should you find a better policy elsewhere, they are happy to refund your money. Besides that, CSA has two unique features. The first being the maximum trip length as 356 days. Second, they have a 24-hr hotline with a stand-by doctor to answer your questions and concern. Should an emergency situation occur, you are always a phone call away from assistance. The only drawback of CSA Travel Protection is that they have a very limited selection of policies, and their Lookback Period is 180 days.

#2 Second Choice: HTH TripProtector Preferred

The HTH TripProtector Company will waive the pre-existing conditions provided that you:

- Purchase the policy within 21 calendar days after your initial trip deposit date,

- Insure your trip’s full prepaid, non-refundable cost, and

- You are medically able to travel at the date of the trip

HTH TripProtector Preferred is the second runner-up in our selection. Although you are required to purchase a policy within 21 days after your initial trip deposit date, HTH offers many advantages. The first big selling point is that their policy will accept up to $100,000 for pre-existing condition coverage and $500,000 for Secondary Emergency Medical coverage. Another big selling point is that their Lookback Period for pre-existing conditions is only 60 days. Unlike many other insurance companies, HTH will cover trips to Cuba.

#3 Third Choice: MH Ross Complete

The MH Ross Company will waive the pre-existing conditions provided that you:

- Purchase the policy within 15 calendar days after your initial trip deposit date,

- Insure part of your full prepaid trip cost as set by the company policy, and

Similar to HTH TripProtector, MH Ross Complete policy will accept up to $100,000 for pre-existing condition coverage and has a Lookback Period of only 60 days. But unlike the first and second choices, the MH Ross Company does not require you to insure the full prepaid trip cost but only a percentage of the cost. At the same time, they offer an option of advance payment to a hospital to secure your admission in case of emergency.

This is a great policy for busy working individuals as cancellation due to work reasons coverage is included. The downside for this policy is that there is no lower price for children coverage. So if your child is the diabetic patient who requires the waiver, you will have to pay full price for his or her coverage.

Depending on where you are traveling, choosing to purchase a traveling insurance policy at your travel destination may be cheaper and “friendlier”. For example, Canada Manulife CoverMe Travel Insurance allows coverage of diabetic patients provided that their condition is stable in the 180 days before the effective date of insurance. As stated in their policy, changing in medication brands and routine adjustment of insulin dosage are allowed as long as the prescriptions are not newly prescribed or stopped.

There are a few companies in the UK that will provide similar policies as well. However, if you do choose to go with this option, make sure you plan and purchase ahead of time as some policies will require a 24 hour activation period in which the company is not obligated to cover you should any emergency event occurs.

Another option to explore is to ask your credit card companies about any insurance policies included with your Visa or Mastercard. For some credit card companies, members will have free enrollment to traveling insurance policy should they purchase the trip on their credit card.

This will include cancellation of the ticket, rebooking of flight, lost luggage expenses, and even luggage replacement. With added purchase, health insurance may be included as well. This way, you can purchase a lower coverage waiver policy and only use it for your diabetes emergency needs.

Enjoy your Trip

Your trip should be filled with great memories of fun. By doing your research early on and paying for a traveling health insurance policy, you will have a much better control of any unplanned situations. While you are choosing the right plan, remember to read the policy thoroughly and make sure you are reading the correct State policy.

At the same time, ask lots of questions from different sources. By knowing the policy details, you can plan ahead what to do should specific health problem arises. This way, you can take the best advantage of your coverage without having to pay out of your own pocket for unnecessary expenses.

Please post any further suggestions for articles down below in the comments section.

TheDiabetesCouncil Article | Reviewed by Dr. Sergii Vasyliuk MD on June 02, 2020

References:

- https://www.cdc.gov/diabetes/library/features/traveling-with-diabetes.html

- https://www.cdc.gov/diabetes/ndep/vacation.html

More Guides

About Lianne Fachetti, ABA

Lianne Fachetti holds a degree in Biopsychology. With a keen interest in both psychological and biological aspects of behavior forming, she has worked as a researcher at the UBC Brain Research Centre for seven years focusing on the research of memory formation, neural damage from epilepsy, and hormones' effects on behavioral changes. She is also a certified ABA therapist for autistic children.

Connect with us!

- Anti-Spam Policy

- Terms & Conditions

- Privacy Policy

Travel Insurance for Diabetics: Travel Worry-Free

Written and researched by Michael Kays (Travel Insurance Expert) | Fact Checked by Danya Kristen (Insurance Agent).

As an older individual living with diabetes, you might be a bit hesitant about venturing out to explore the world. But there’s no reason to miss out on exciting new experiences, as long as you plan ahead and ensure you have the proper travel insurance coverage .

In this article, we’ll guide you through the ins and outs of travel insurance for diabetics, so you can confidently set out on your next adventure without breaking a sweat (unless you’re dancing the night away, of course!).

In this article...

Why Bother with Travel Insurance for Diabetics?

You might wonder if travel insurance is worth the fuss. Here are some reasons why it’s essential for diabetics:

- Unpredictable medical expenses: Health care abroad can be costly, especially if you need urgent diabetes-related care. Better safe than sorry!

- Coverage for pre-existing conditions : Some travel insurance policies cover pre-existing conditions, such as diabetes, offering you protection if you need medical attention during your trip.

- Trip cancellation or interruption: If your diabetes unexpectedly causes you to cancel or cut short your journey, travel insurance can help recover non-refundable costs.

- Peace of mind: With travel insurance, you can focus on enjoying your trip, knowing that you’re covered for any diabetes-related incidents.

Safe Travels USA Cost Saver

Safe Travels USA Comprehensive

Patriot Platinum

Visitors Care

Patriot International

Patriot America

Recommended plans.

✅ Atlas America

Up to $2,000,000 of Overall Maximum Coverage, Emergency Medical Evacuation, Medical coverage for eligible expenses related to COVID-19, Trip Interruption & Travel Delay.

✅ Safe Travels Comprehensive

Coverage for in-patient and out-patient medical accidents up to $1 Million, Coverage of acute episodes of pre-existing conditions, Coverage from 5 days to 364 days (about 12 months).

✅ Patriot America Platinum

Up to $8,000,000 limits, Emergency Medical Evacuation, Coinsurance for treatment received in the U.S. (100% within PPO Network), Acute Onset of Pre-Existing Conditions covered.

Pre-existing Conditions and Travel Insurance: The Nitty-Gritty

As a diabetic, understanding pre-existing conditions coverage in travel insurance policies is crucial:

- What it means: A pre-existing condition is any medical issue you had before purchasing your travel insurance, including diagnosed or undiagnosed conditions.

- Stability is key: Insurers often require your diabetes to be stable and well-managed for a certain period (e.g., three to six months) before offering coverage for pre-existing conditions.

- Read the fine print: Some policies exclude coverage for pre-existing conditions, so be sure to find one that covers your diabetes needs.

Tips for Finding a Diabetic-Friendly Travel Insurance Policy

To find the perfect travel insurance policy for your needs, follow these tips:

- Shop around: Compare different travel insurance policies to find one that provides comprehensive coverage for pre-existing conditions, including diabetes.

- Seek specialized providers: Some insurance companies cater to individuals with specific medical needs, like diabetes. These providers may offer more customized policies and coverage options.

- Check reviews: Look for feedback from fellow diabetic travelers who’ve used the travel insurance provider to gauge their reliability and customer service.

- Consult your doctor: Talk to your healthcare provider about your travel plans and ask for recommendations on the type of coverage and support you might need.

Managing Diabetes on the Go

With the right travel insurance policy in hand, it’s also essential to manage your diabetes effectively while traveling:

- Bring extra supplies: Always pack more medication and diabetes supplies than you think you’ll need to account for any unexpected situations.

- Keep an eye on your blood sugar: Travel can impact your glucose levels, so monitor them regularly, especially with changes in diet, activity, or time zones.

- Be prepared for emergencies: Carry a medical ID and a letter from your doctor outlining your diabetes, medications, and any special considerations, just in case.

- Share with your travel buddies: Inform your travel companions about your diabetes and teach them how to help you in case of an emergency.

Conclusion:

Traveling with diabetes in your golden years may require some extra preparation, but it’s entirely possible with the right travel insurance policy and careful diabetes management.

By understanding the importance of travel insurance for diabetics, finding the right policy, and keeping your condition in check, you can fully embrace the joy of traveling, creating lasting memories, and discovering new experiences.

Don’t let diabetes hold you back from seeing the world and enjoying your well-deserved retirement years.

Keeping Your Health in Check: Travel Tips for Diabetics

In addition to having the right travel insurance, here are some helpful tips for maintaining your health while traveling with diabetes:

Plan your meals: Research local cuisine and restaurants at your destination, so you can make healthier food choices and keep your blood sugar levels steady.

Stay hydrated: Drink plenty of water during your trip, as dehydration can affect blood sugar levels.

Keep snacks handy: Carry healthy snacks with you to prevent low blood sugar episodes when you’re out and about.

Maintain a routine: Try to stick to your regular schedule for meals, medication, and blood sugar monitoring as much as possible, even when you’re on vacation.

Frequently Asked Questions

Travel Insurance for Diabetics Here are some common questions older individuals with diabetes may have about travel insurance:

Q: Can I purchase travel insurance if my diabetes isn’t well-managed?

A: It depends on the insurance provider. Some insurers may still offer coverage, but at a higher premium or with limited benefits . It’s always best to work with your healthcare provider to manage your diabetes effectively before traveling.

Q: What should I do if I experience a diabetes-related emergency while traveling?

A: Contact your travel insurance provider’s emergency assistance hotline for guidance and support. They can help you locate the nearest medical facility, provide language assistance, or coordinate necessary medical services.

Q: How do I disclose my diabetes to my travel insurance provider?

A: When applying for travel insurance, you’ll need to complete a medical questionnaire that includes questions about your diabetes. Be honest and thorough when providing information, as inaccurate or incomplete disclosure could impact your coverage.

So, pack your bags, grab your travel insurance, and set out on your next adventure with the confidence and security that comes with proper planning and coverage.

Enjoy your golden years and make the most of your travels, knowing that you’re well-prepared to manage your diabetes and any challenges that may arise. Happy travels!

Get Free Consultation

January 24, 2020

January 23, 2020

January 22, 2020

Patriot America Plus

January 21, 2020

Atlas America

January 16, 2020

Nationwide Prime Travel Insurance Review

September 21, 2023

Nationwide Luxury Cruise Travel Insurance Review

Nationwide choice cruise travel insurance review, nationwide universal cruise travel insurance plan review, nationwide essential travel insurance plan review, all clear travel insurance – all you need to know.

August 4, 2023

CoverMore Travel Insurance: Everything You Need to Know

Staysure travel insurance: everything you need to know, post office travel insurance – everything you need to know, argentina expatriate health insurance – ultimate guide.

August 2, 2023

Visitcover.com is a travel insurance review portal that will help you choose the right travel insurance plan for your next trip. By bringing you unbiased, fact-checked, verified information about travel insurance companies, plans, claim processes, and everything that's usually mentioned in the fine print. Make informed decisions, with us!

Opening hours

09.00 - 22.00

09.00 - 18.00

09.00 - 16.00

4422 Flamingo Villas, Ajman Media City, United Arab Emirates

Call Us: +1-972-985-4400

© 2023 VisitCover.com

- Help and Support

Travel insurance for people with diabetes

Article contents.

Tegan Oldfield

24 October 2023 | Updated 2 November 2023 | 4 minute read

Travelling with diabetes can need a little extra preparation. Getting a travel insurance policy that will protect you financially if you become ill on your trip is important.

We’ve broken down everything you need to know about travel insurance for travellers with diabetes and some advice on how to prepare for your trip.

Why do people with diabetes need travel insurance?

People with diabetes mostly need holiday insurance for the same reason everyone else does. It gives you financial protection if certain things go wrong on your trip.

If you have any medical condition, including diabetes, you may be more likely to fall ill on holiday. This means you need an insurance policy in place to cover medical costs.

What should travel insurance for travellers with diabetes cover?

A travel insurance policy should cover:

- emergency medical costs

- repatriation if it’s medically necessary for you to return to the UK

- lost, stolen or damaged medication (like your insulin)

- costs if you need to cut your trip short or cancel it completely due to illness caused by your diabetes

Do I have to declare diabetes when buying travel insurance?

Yes. Diabetes is a pre-existing medical condition , so you’ll need to tell your insurer about it when buying your policy.

It’s possible that changes in diet, environment and activity can affect blood glucose levels and lead to medical issues.

Insurers need to know about your condition to make sure you get the right treatment quickly if you become ill on your trip.

If you don’t tell us and then need to claim for medical expenses, we won’t cover all or some of the costs even if your claim isn’t related to your diabetes.

What will my insurer ask during the screening process?

We'll ask you about:

- the medications you take for your diabetes

- whether you’ve been hospitalised with your condition recently

- if you have any associated conditions, like high blood pressure

Everything you tell us is strictly confidential. It’s simply to make sure we can give you the right cover.

How much is travel insurance for people with diabetes?

The price of travel insurance will generally be higher if you have pre-existing medical conditions which includes diabetes or any diabetes-related conditions.

However, paying for your own medical care abroad would be significantly more expensive.

The price of your policy will always depend on:

- where you’re going

- how long you’re going for

- what you’re going to get up to on your trip

- the nature of your pre-existing condition

Does a Global Health Insurance Card (GHIC) cover my diabetes?

A GHIC or the old European Health Insurance Card (EHIC) allows you to access medical treatment while you’re in certain countries in Europe.

If you need treatment for any diabetes-related issues, the GHIC or EHIC can reduce the cost of treatment or make it free in some instances.

It’s important to remember that the GHIC is not a stand-in for travel insurance. It doesn’t apply everywhere and only works at clinics that are in a reciprocal agreement with the UK.

It also doesn’t cover you for any of the other associated costs, like the cost of cancelling or cutting short your trip or the cost of repatriation.

Read our guide on the EHIC/GHIC cards , including where and when you can use them.

What preparations should I make for travelling with diabetes?

You should check with your GP or diabetic consultant before you travel. This is so you can:

- get a prescription for twice the amount of your regular medication – this allows for any unexpected delays or losses

- get advice on when you should be taking your insulin – especially if you’re travelling to another time zone

You may also use additional devices, like monitoring equipment. You should get a doctor’s letter to take with you on your trip, which explains:

- the medication you take

- the monitoring and dispensing devices you use

- any other necessary equipment like needles or syringes

You can show this letter to customs or security staff when travelling. If you have any medical issues, you can also show this to the medical professionals treating you.

Read our guide on travelling with your prescription medication .

Flying with diabetes

You should:

- pack your insulin in a cool bag and keep it in your hand luggage so it’s always accessible

- pack snacks in case you experience delays

- get to the airport in plenty of time so you can tell the airline and security staff about your medication and equipment

What should I do if I become ill while abroad?

You should contact the emergency services, go to the nearest hospital or seek the medical assistance you need immediately.

You need to contact your insurer’s emergency service or helpline as soon as possible. If you’re with us, our 24-hour emergency helpline is 0292 010 777.

Share with your friends...

Check out our related articles.

20 Oct 2023

Ultimate guide to travel vaccinations

03 Aug 2023

Travelling with medication

24 Oct 2022

Ultimate guide to hand luggage restrictions

5 star defaqto rated platinum level travel insurance.

https://admiral.com/magazine/guides/travel/travel-insurance-for-people-with-diabetes

- Travel Insurance

- RoamRight Home

Will travel insurance cover diabetes?

Living with diabetes shouldn’t stop you from traveling. Whether you have type 1 or type 2 diabetes, you deserve to have fun and relax on vacation as much as anyone else. However, when it comes to insuring your trip, there are a few things to keep in mind.

Is diabetes considered a pre-existing medical condition?

Travel insurance generally excludes pre-existing medical conditions. This means that if you need to cancel your trip due to a situation related to your diabetes, you may not have coverage.

For most Arch RoamRight plans, a pre-existing condition is defined as:

Any illness, disease, or other condition during the 180 day period immediately prior to the Effective Date of Your coverage for which You or Your Traveling Companion, Business Partner or Family Member: 1) received or received a recommendation for a test, examination, or medical treatment; or 2) took or received a prescription for drugs or medicine. Item (2) of this definition does not apply to a condition which is treated or controlled solely through the taking of prescription drugs or medicine and remains treated or controlled without any adjustment or change in the required prescription throughout the 180 day period before Your coverage is effective under this policy.

The 180-day “look back” period may vary based on the plan selected (Pro and Pro Plus plans have a shorter, 60-day look back period).

In summary, if you have diabetes and in the past 180 days, have not had or been recommended for any test, examinations or medical treatments for the disease, AND your prescription medications have not changed, your diabetes is not classified as a pre-existing condition. Therefore, travel insurance coverage may be available.

How to purchase travel insurance if your diabetes is a pre-existing condition

If your medical situation has changed recently, such as having tests recommended and medication changes, you may still be able to have travel insurance coverage.

With most Arch RoamRight plans, the clause that excludes pre-existing conditions can be waived when certain criteria are met. These criteria are:

- You purchase your policy within 21 days of making the initial payment on your trip;

- You insure all of the Travel Arrangements that are subject to cancellation penalties and restrictions;

- You are not disabled from travel when you purchase your travel insurance policy; and

- The booking for this trip is your first and only booking for this travel period and destination.

When you meet all four of these conditions, any trip cancellations or travel medical emergencies related to your diabetes may be covered.

Diabetes and Travel Insurance Coverage during Severe Emergencies

Rest assured – there are two cases where travel insurance can provide coverage for complications from diabetes, regardless of whether it is considered a pre-existing condition or not. These are Emergency Medical Evacuations and Repatriation of Remains.

You may be in good health, safely managing your condition when you plan to go on a trip. However, medical emergencies can still occur. If you experience diabetic complications and need emergency medical treatment that cannot be provided in the local area, you may be covered for an emergency medical evacuation.

It’s happened before – just watch this story about a man who experience major complications due his diabetes while he was in Antarctica.

Learn More about Traveling with a Medical Condition

There are several places where you can get more information about traveling with a medical condition. You may be interested in these posts found here in on the Arch RoamRight Travel Insurance Blog:

- When Travel Insurance May Cover Pre-Existing Conditions

- Will Your Health Insurance Cover You Abroad?

Note: Available plans and coverages may have changed since this blog was published.

- travel insurance

- Trip Planning

Related Posts

Arch RoamRight recently launched two plans on our website; learn the differences between the plans.

Volcanic eruptions are natural disasters that may be covered events under Arch RoamRight travel protection plans. From minor disruptions to catastrophic events, volcanos can affect travelers around the world.

- New Requirements for U.S. Citizens Traveling to Europe Starting in 2021 Starting in 2021, Americans visiting many popular European countries will need to go through the ETIAS process.

About the Author

Adele dirende.

Adele DiRende is a Marketing Intern currently pursuing a degree in Mass Communications at Towson University. Although the wallet of a college student is not kind to those with a passion for travel, Adele has experience in international travel to places like Italy and the UK, as well as domestic travel around the U.S. In addition to travel, Adele enjoys photography, music, and creative writing. Connect with her on LinkedIn .

Get A Free Travel Insurance Quote

Travel smarter with travel insurance from RoamRight. Get your free, no-obligation quote online today.

- Coverage For: -- Optional -- General Travel Annual

Top Blog Authors

- Diana Lambdin Meyer

- Erin De Santiago

- Jessica Festa

- Keryn Means

- Norbert Figueroa

- Stephanie Yoder

- Stephen Schreck

- Terri Marshall

View all Blog Authors

- Puerto Rico

- United Kingdom

- United States of America

View Countries with Blogs

Stay Connected!

Sign up for RoamRight's FREE monthly email newsletter to get travel tips, tricks, news, ideas, and inspiration!

- About RoamRight

- Money-Back Guarantee

- Privacy Policy

- Terms of Use

- Fraud Notices

The RoamRight mark is used by Arch Insurance Company and owned by its parent company, Arch Capital Group (U.S.). Insurance coverages are underwritten by Arch Insurance Company, NAIC #11150, under certain policy series, including LTP 2013 and amendments thereto. Certain terms, conditions, restrictions and exclusions apply and coverages may vary in certain states. In the event of any conflict between your policy terms and coverage descriptions on this website, the terms and conditions of your policy shall govern. Click here for privacy notice .

Copyright© 2024 Arch Insurance Company. All rights reserved.

21 Tips for Traveling With Diabetes

Plan ahead for more fun and fewer worries.

Don’t let good diabetes management go on vacation just because you did. Traveling to new places gets you out of your routine—that’s a big part of the fun. But delayed meals, having unfamiliar food, being more active than usual, and being in different time zones can all disrupt your diabetes management. Plan ahead so you can count on more fun and less worry on the way and when you get to your destination.

Before You Go

- How your planned activities could affect your diabetes and what to do about it.

- How to adjust your insulin doses if you’re traveling to places in a different time zone.

- To provide prescriptions for your medicines in case you lose or run out of them.

- If you’ll need any vaccines.

- To write a letter stating that you have diabetes and why you need your medical supplies.

- Just in case, find pharmacies and clinics close to where you’re staying.

- Get a medical ID bracelet that states you have diabetes and any other health conditions you may have.

- Buy travel insurance in case you miss your flight or need medical care.

- Order a special meal in advance for the flight that fits with your meal plan, or pack your own.

- Put your diabetes supplies in a carry-on bag (insulin could get too cold in your checked luggage). Think about bringing a smaller bag to have at your seat for insulin, glucose tablets, and snacks.

- Pack twice as much medicine as you think you’ll need. Carry medicines in the original pharmacy bottles, or ask your pharmacist to print out extra labels you can attach to plastic bags.

- Be sure to pack healthy snacks, like fruit, raw veggies, and nuts.

- Get an optional TSA notification card [PDF – 23.8KB] to help the screening process go more quickly and smoothly.

- Good news: people with diabetes are exempt from the 3.4 oz. liquid rule for medicines, fast-acting carbs like juice, and gel packs to keep insulin cool.

- A continuous glucose monitor or insulin pump could be damaged going through the X-ray machine. You don’t have to disconnect from either; ask for a hand inspection instead.

- Visit CDC’s Travelers’ Health site for more helpful resources.

- Doctor’s letter and prescriptions

- Snacks and glucose tablets

- Extra insulin and diabetes medicines

While You’re Traveling

- If you’re driving, pack a cooler with healthy foods and plenty of water to drink.

- Don’t store insulin or diabetes medicine in direct sunlight or in a hot car; keep them in the cooler too. Don’t put insulin directly on ice or a gel pack.

- Heat can also damage your blood sugar monitor, insulin pump, and other diabetes equipment. Don’t leave them in a hot car, by a pool, in direct sunlight, or on the beach. The same goes for supplies such as test strips.

- Fruit, nuts, sandwiches, yogurt

- Salads with chicken or fish (skip the dried fruit and croutons)

- Eggs and omelets

- Burgers with a lettuce wrap instead of a bun

- Fajitas (skip the tortillas and rice)

Say goodbye to worry when you pack your diabetes supplies in a carry-on bag.

- Stop and get out of the car or walk up and down the aisle of the plane or train every hour or two to prevent blood clots (people with diabetes are at higher risk).

- Set an alarm on your phone for taking medicine if you’re traveling across time zones.

Once You’re There

- Your blood sugar may be out of your target range at first, but your body should adjust in a few days. Check your blood sugar often and treat highs or lows as instructed by your doctor or diabetes educator.

- If you’re going to be more active than usual, check your blood sugar before and after and adjust food, activity, and insulin as needed.

- Food is a huge highlight (and temptation!) on a cruise. Avoid the giant buffet, and instead order off the spa menu (healthier choices) or low-carb menu (most ships have one) or order something tasty that fits in your meal plan from the 24-hour room service.

- Don’t overdo physical activity during the heat of the day. Avoid getting a sunburn and don’t go barefoot, not even on the beach.

- High temperatures can change how your body uses insulin. You may need to test your blood sugar more often and adjust your insulin dose and what you eat and drink. Get more hot-weather tips here .

- You may be unable to find everything you need to manage your diabetes when you are away from home, especially in another country. Learn some useful phrases in the local language, such as “I have diabetes” and “where is the nearest pharmacy?”

- If your vacation is in the great outdoors, bring disposable wipes so you can clean your hands before you check your blood sugar.

Making Memories

Diabetes can make everyday life and travel more challenging, but it doesn’t have to keep you close to home. The more you plan ahead, the more you’ll be able to relax and enjoy all the exciting experiences of your trip.

- CDC’s Health Information for Travelers

- Diabetes Basics

- Living With Diabetes

- Diabetes Features

- CDC Diabetes on Facebook

- @CDCDiabetes on Twitter

To receive updates about diabetes topics, enter your email address:

- Diabetes Home

- State, Local, and National Partner Diabetes Programs

- National Diabetes Prevention Program

- Native Diabetes Wellness Program

- Chronic Kidney Disease

- Vision Health Initiative

- Heart Disease and Stroke

- Overweight & Obesity

Exit Notification / Disclaimer Policy

- The Centers for Disease Control and Prevention (CDC) cannot attest to the accuracy of a non-federal website.

- Linking to a non-federal website does not constitute an endorsement by CDC or any of its employees of the sponsors or the information and products presented on the website.

- You will be subject to the destination website's privacy policy when you follow the link.

- CDC is not responsible for Section 508 compliance (accessibility) on other federal or private website.

The best travel insurance policies and providers

It's easy to dismiss the value of travel insurance until you need it.

Many travelers have strong opinions about whether you should buy travel insurance . However, the purpose of this post isn't to determine whether it's worth investing in. Instead, it compares some of the top travel insurance providers and policies so you can determine which travel insurance option is best for you.

Of course, as the coronavirus remains an ongoing concern, it's important to understand whether travel insurance covers pandemics. Some policies will cover you if you're diagnosed with COVID-19 and have proof of illness from a doctor. Others will take coverage a step further, covering additional types of pandemic-related expenses and cancellations.

Know, though, that every policy will have exclusions and restrictions that may limit coverage. For example, fear of travel is generally not a covered reason for invoking trip cancellation or interruption coverage, while specific stipulations may apply to elevated travel warnings from the Centers for Disease Control and Prevention.

Interested in travel insurance? Visit InsureMyTrip.com to shop for plans that may fit your travel needs.

So, before buying a specific policy, you must understand the full terms and any special notices the insurer has about COVID-19. You may even want to buy the optional cancel for any reason add-on that's available for some comprehensive policies. While you'll pay more for that protection, it allows you to cancel your trip for any reason and still get some of your costs back. Note that this benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

In this guide, we'll review several policies from top travel insurance providers so you have a better understanding of your options before picking the policy and provider that best address your wants and needs.

The best travel insurance providers

To put together this list of the best travel insurance providers, a number of details were considered: favorable ratings from TPG Lounge members, the availability of details about policies and the claims process online, positive online ratings and the ability to purchase policies in most U.S. states. You can also search for options from these (and other) providers through an insurance comparison site like InsureMyTrip .

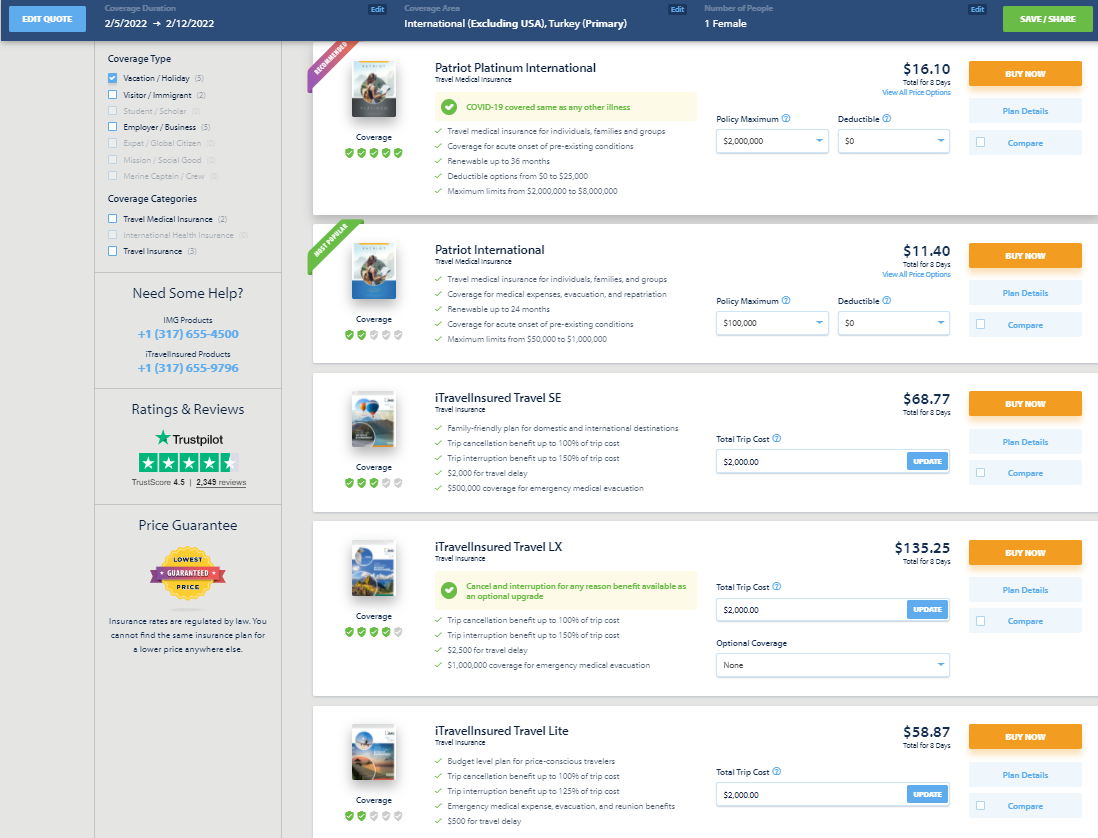

When comparing insurance providers, I priced out a single-trip policy for each provider for a $2,000, one-week vacation to Istanbul . I used my actual age and state of residence when obtaining quotes. As a result, you may see a different price — or even additional policies due to regulations for travel insurance varying from state to state — when getting a quote.

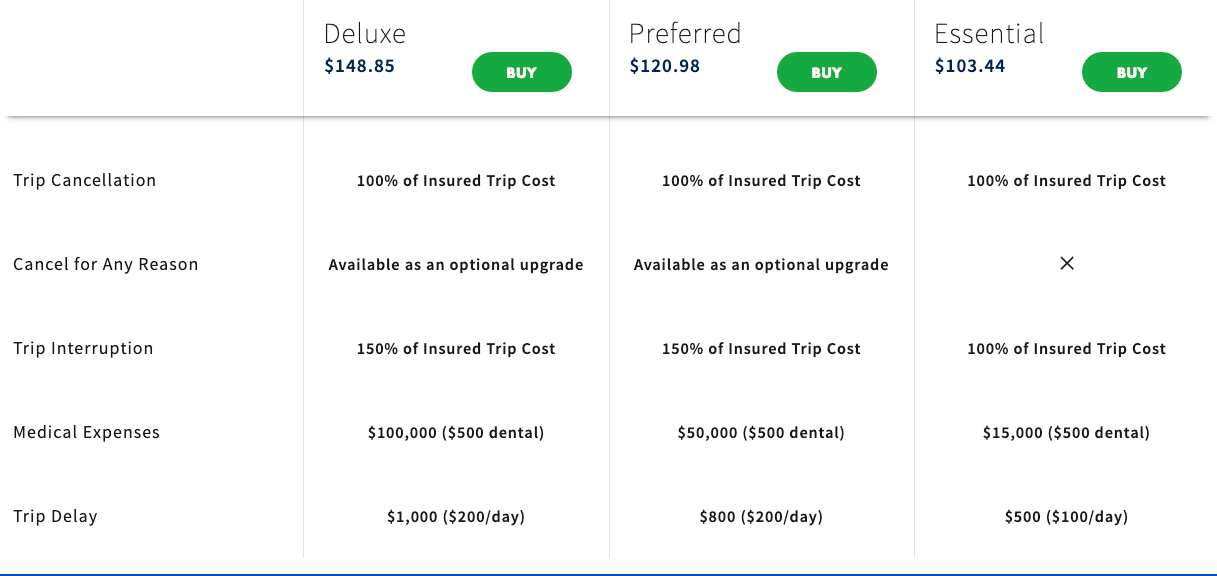

AIG Travel Guard

AIG Travel Guard receives many positive reviews from readers in the TPG Lounge who have filed claims with the company. AIG offers three plans online, which you can compare side by side, and the ability to examine sample policies. Here are three plans for my sample trip to Turkey.

AIG Travel Guard also offers an annual travel plan. This plan is priced at $259 per year for one Florida resident.

Additionally, AIG Travel Guard offers several other policies, including a single-trip policy without trip cancellation protection . See AIG Travel Guard's COVID-19 notification and COVID-19 advisory for current details regarding COVID-19 coverage.

Preexisting conditions

Typically, AIG Travel Guard wouldn't cover you for any loss or expense due to a preexisting medical condition that existed within 180 days of the coverage effective date. However, AIG Travel Guard may waive the preexisting medical condition exclusion on some plans if you meet the following conditions:

- You purchase the plan within 15 days of your initial trip payment.

- The amount of coverage you purchase equals all trip costs at the time of purchase. You must update your coverage to insure the costs of any subsequent arrangements that you add to your trip within 15 days of paying the travel supplier for these additional arrangements.

- You must be medically able to travel when you purchase your plan.

Standout features

- The Deluxe and Preferred plans allow you to purchase an upgrade that lets you cancel your trip for any reason. However, reimbursement under this coverage will not exceed 50% or 75% of your covered trip cost.

- You can include one child (age 17 and younger) with each paying adult for no additional cost on most single-trip plans.

- Other optional upgrades, including an adventure sports bundle, a baggage bundle, an inconvenience bundle, a pet bundle, a security bundle and a wedding bundle, are available on some policies. So, an AIG Travel Guard plan may be a good choice if you know you want extra coverage in specific areas.

Purchase your policy here: AIG Travel Guard .

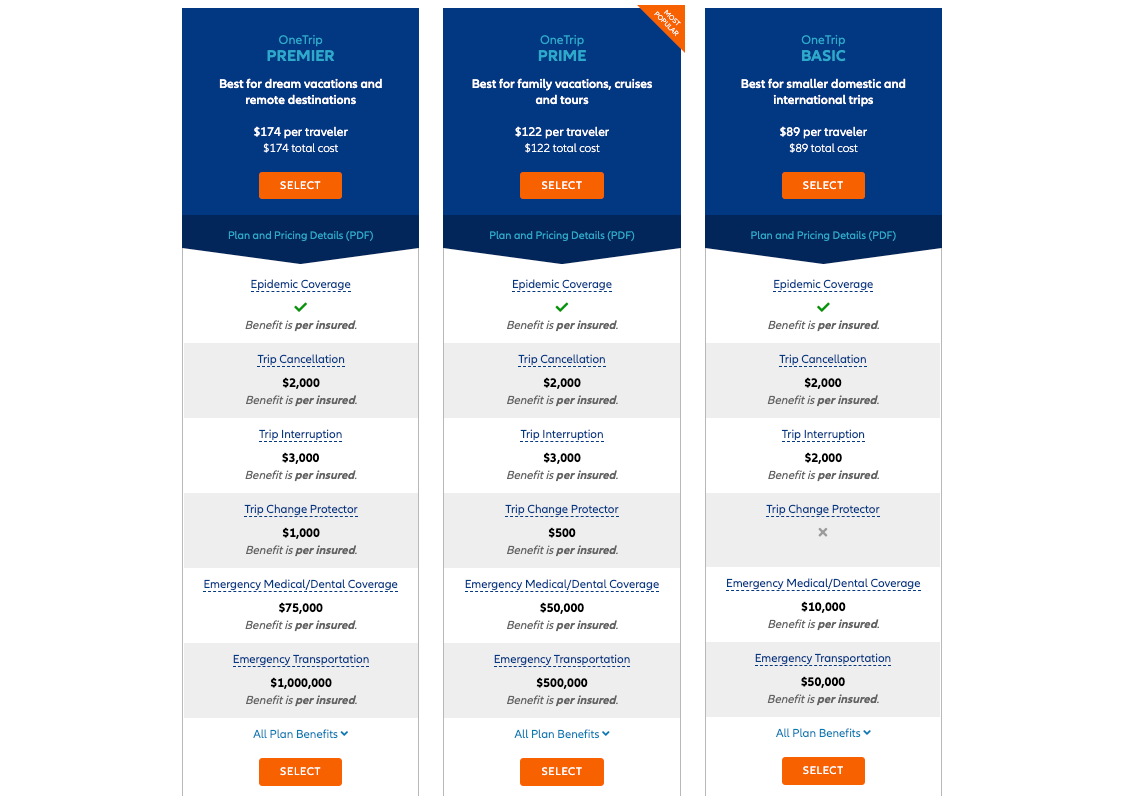

Allianz Travel Insurance

Allianz is one of the most highly regarded providers in the TPG Lounge, and many readers found the claim process reasonable. Allianz offers many plans, including the following single-trip plans for my sample trip to Turkey.

If you travel frequently, it may make sense to purchase an annual multi-trip policy. For this plan, all of the maximum coverage amounts in the table below are per trip (except for the trip cancellation and trip interruption amounts, which are an aggregate limit per policy). Trips typically must last no more than 45 days, although some plans may cover trips of up to 90 days.

See Allianz's coverage alert for current information on COVID-19 coverage.

Most Allianz travel insurance plans may cover preexisting medical conditions if you meet particular requirements. For the OneTrip Premier, Prime and Basic plans, the requirements are as follows:

- You purchased the policy within 14 days of the date of the first trip payment or deposit.

- You were a U.S. resident when you purchased the policy.

- You were medically able to travel when you purchased the policy.

- On the policy purchase date, you insured the total, nonrefundable cost of your trip (including arrangements that will become nonrefundable or subject to cancellation penalties before your departure date). If you incur additional nonrefundable trip expenses after purchasing this policy, you must insure them within 14 days of their purchase.

- Allianz offers reasonably priced annual policies for independent travelers and families who take multiple trips lasting up to 45 days (or 90 days for select plans) per year.

- Some Allianz plans provide the option of receiving a flat reimbursement amount without receipts for trip delay and baggage delay claims. Of course, you can also submit receipts to get up to the maximum refund.

- For emergency transportation coverage, you or someone on your behalf must contact Allianz, and Allianz must then make all transportation arrangements in advance. However, most Allianz policies provide an option if you cannot contact the company: Allianz will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Allianz Travel Insurance .

American Express Travel Insurance

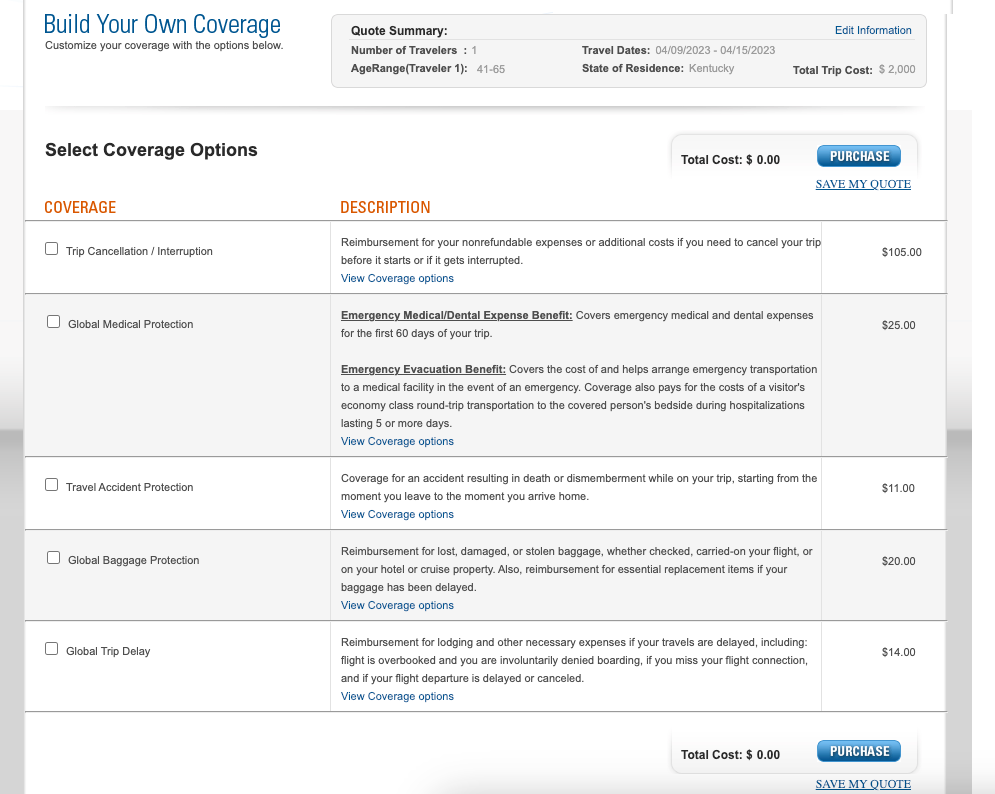

American Express Travel Insurance offers four different package plans and a build-your-own coverage option. You don't have to be an American Express cardholder to purchase this insurance. Here are the four package options for my sample weeklong trip to Turkey. Unlike some other providers, Amex won't ask for your travel destination on the initial quote (but will when you purchase the plan).

Amex's build-your-own coverage plan is unique because you can purchase just the coverage you need. For most types of protection, you can even select the coverage amount that works best for you.

The prices for the packages and the build-your-own plan don't increase for longer trips — as long as the trip cost remains constant. However, the emergency medical and dental benefit is only available for your first 60 days of travel.

Typically, Amex won't cover any loss you incur because of a preexisting medical condition that existed within 90 days of the coverage effective date. However, Amex may waive its preexisting-condition exclusion if you meet both of the following requirements:

- You must be medically able to travel at the time you pay the policy premium.

- You pay the policy premium within 14 days of making the first covered trip deposit.

- Amex's build-your-own coverage option allows you to only purchase — and pay for — the coverage you need.

- Coverage on long trips doesn't cost more than coverage for short trips, making this policy ideal for extended getaways. However, the emergency medical and dental benefit only covers your first 60 days of travel.

- American Express Travel Insurance can protect travel expenses you purchase with Amex Membership Rewards points in the Pay with Points program (as well as travel expenses bought with cash, debit or credit). However, travel expenses bought with other types of points and miles aren't covered.

Purchase your policy here: American Express Travel Insurance .

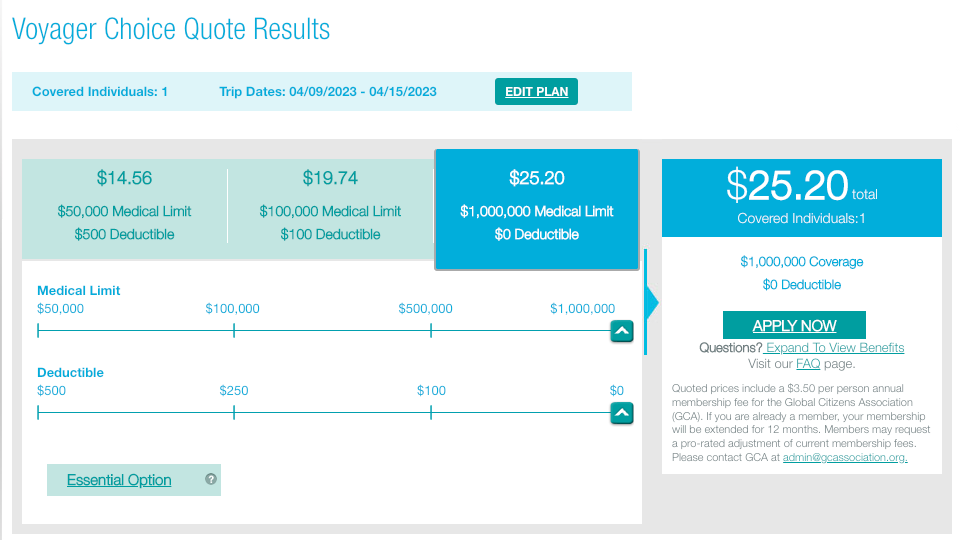

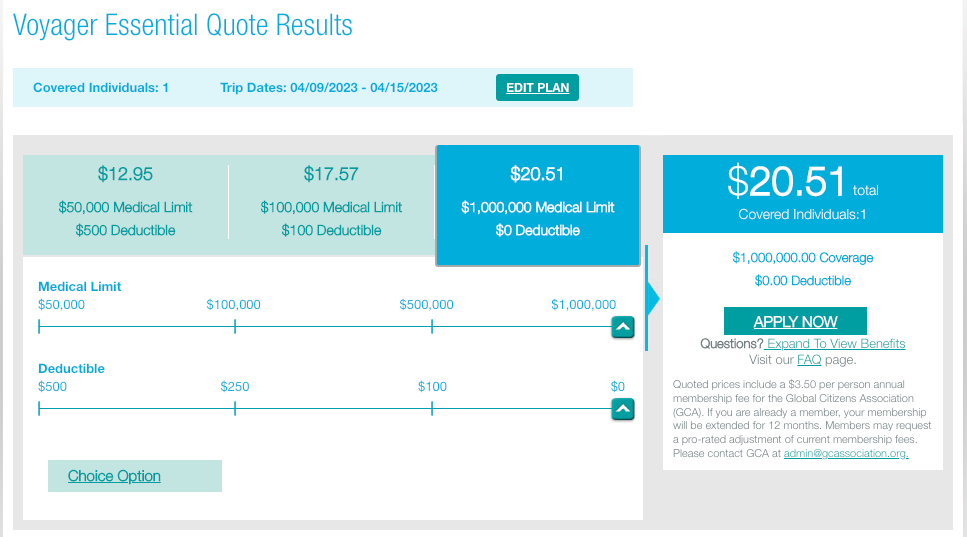

GeoBlue is different from most other providers described in this piece because it only provides medical coverage while you're traveling internationally and does not offer benefits to protect the cost of your trip. There are many different policies. Some require you to have primary health insurance in the U.S. (although it doesn't need to be provided by Blue Cross Blue Shield), but all of them only offer coverage while traveling outside the U.S.

Two single-trip plans are available if you're traveling for six months or less. The Voyager Choice policy provides coverage (including medical services and medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger and already have a U.S. health insurance policy.

The Voyager Essential policy provides coverage (including medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger, regardless of whether they have primary health insurance.

In addition to these options, two multi-trip plans cover trips of up to 70 days each for one year. Both policies provide coverage (including medical services and medical evacuation for preexisting conditions) to travelers with primary health insurance.

Be sure to check out GeoBlue's COVID-19 notices before buying a plan.

Most GeoBlue policies explicitly cover sudden recurrences of preexisting conditions for medical services and medical evacuation.

- GeoBlue can be an excellent option if you're mainly concerned about the medical side of travel insurance.

- GeoBlue provides single-trip, multi-trip and long-term medical travel insurance policies for many different types of travel.

Purchase your policy here: GeoBlue .

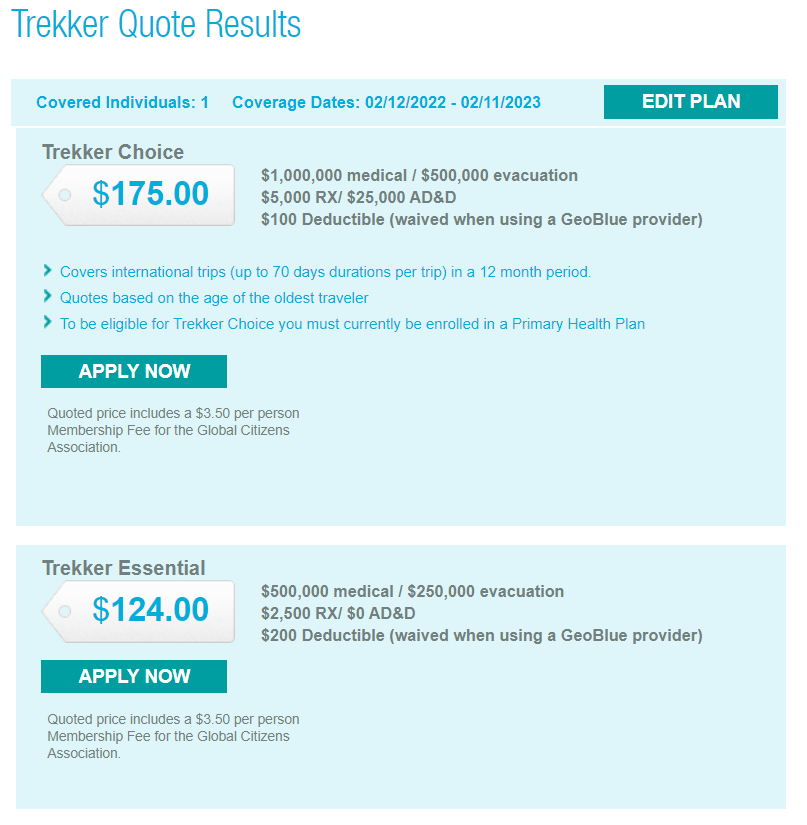

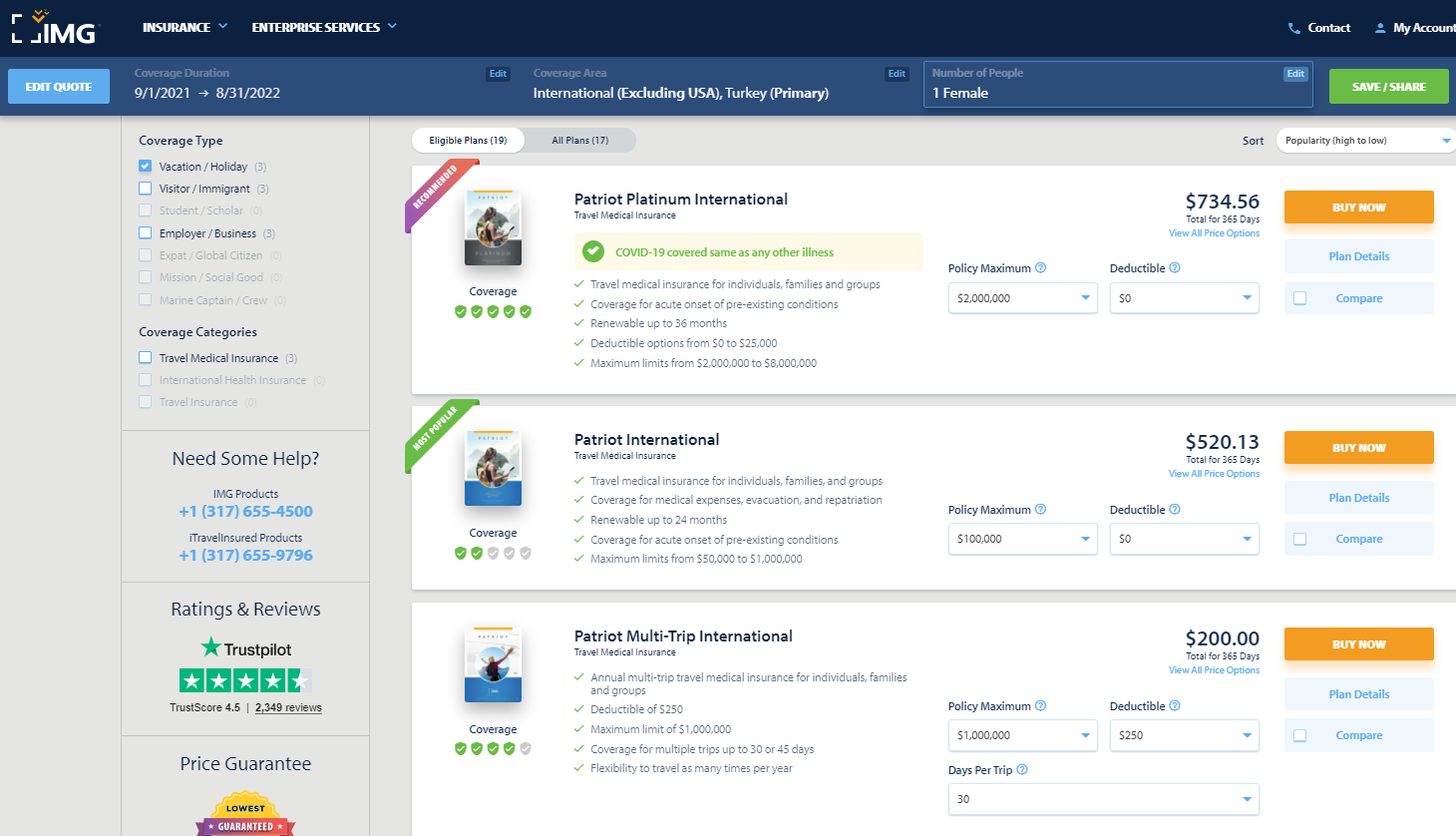

IMG offers various travel medical insurance policies for travelers, as well as comprehensive travel insurance policies. For a single trip of 90 days or less, there are five policy types available for vacation or holiday travelers. Although you must enter your gender, males and females received the same quote for my one-week search.

You can purchase an annual multi-trip travel medical insurance plan. Some only cover trips lasting up to 30 or 45 days, but others provide coverage for longer trips.

See IMG's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Most plans may cover preexisting conditions under set parameters or up to specific amounts. For example, the iTravelInsured Travel LX travel insurance plan shown above may cover preexisting conditions if you purchase the insurance within 24 hours of making the final payment for your trip.

For the travel medical insurance plans shown above, preexisting conditions are covered for travelers younger than 70. However, coverage is capped based on your age and whether you have a primary health insurance policy.

- Some annual multi-trip plans are modestly priced.

- iTravelInsured Travel LX may offer optional cancel for any reason and interruption for any reason coverage, if eligible.

Purchase your policy here: IMG .

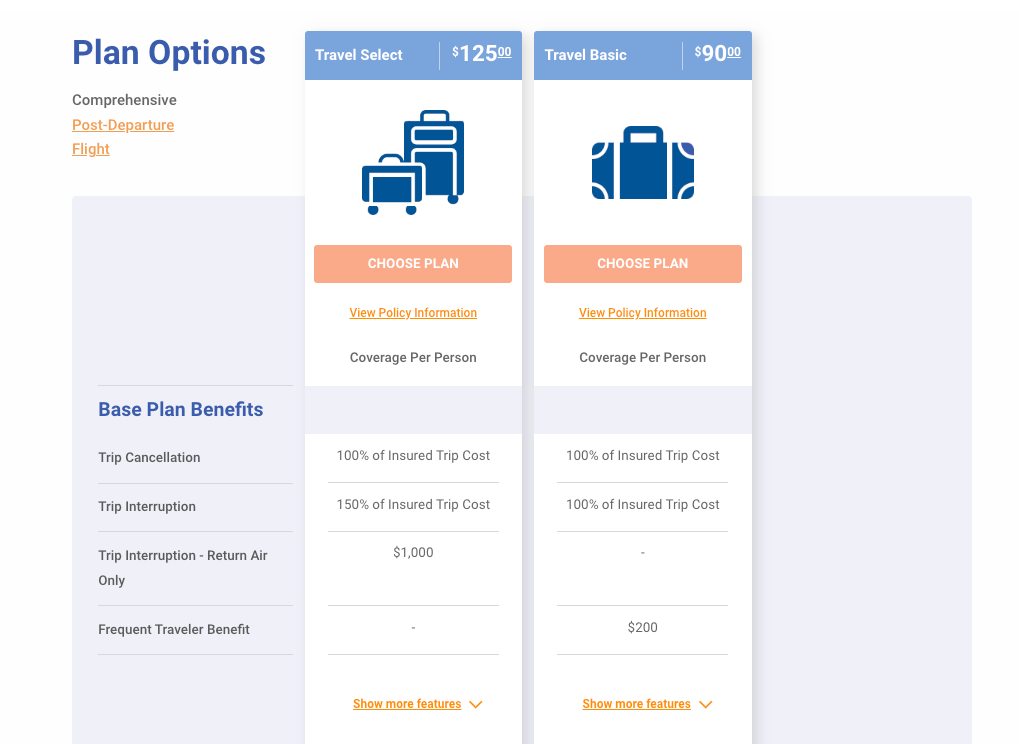

Travelex Insurance

Travelex offers three single-trip plans: Travel Basic, Travel Select and Travel America. However, only the Travel Basic and Travel Select plans would be applicable for my trip to Turkey.

See Travelex's COVID-19 coverage statement for coronavirus-specific information.

Typically, Travelex won't cover losses incurred because of a preexisting medical condition that existed within 60 days of the coverage effective date. However, the Travel Select plan may offer a preexisting condition exclusion waiver. To be eligible for this waiver, the insured traveler must meet all the following conditions:

- You purchase the plan within 15 days of the initial trip payment.

- The amount of coverage purchased equals all prepaid, nonrefundable payments or deposits applicable to the trip at the time of purchase. Additionally, you must insure the costs of any subsequent arrangements added to the same trip within 15 days of payment or deposit.

- All insured individuals are medically able to travel when they pay the plan cost.

- The trip cost does not exceed the maximum trip cost limit under trip cancellation as shown in the schedule per person (only applicable to trip cancellation, interruption and delay).

- Travelex's Travel Select policy can cover trips lasting up to 364 days, which is longer than many single-trip policies.

- Neither Travelex policy requires receipts for trip and baggage delay expenses less than $25.

- For emergency evacuation coverage, you or someone on your behalf must contact Travelex and have Travelex make all transportation arrangements in advance. However, both Travelex policies provide an option if you cannot contact Travelex: Travelex will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Travelex Insurance .

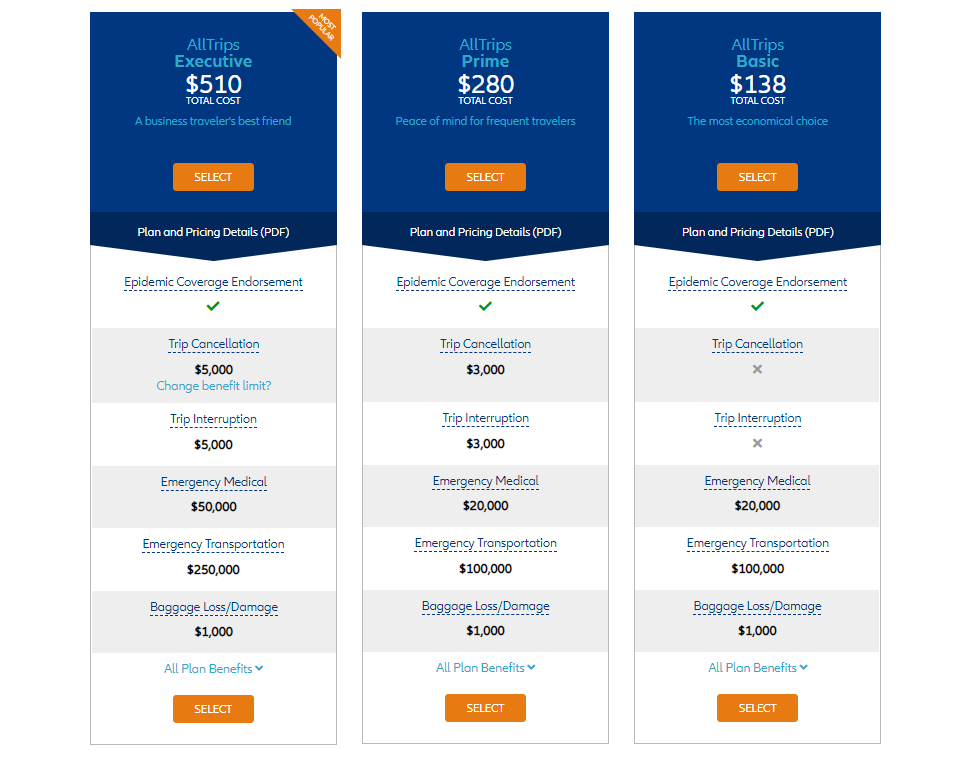

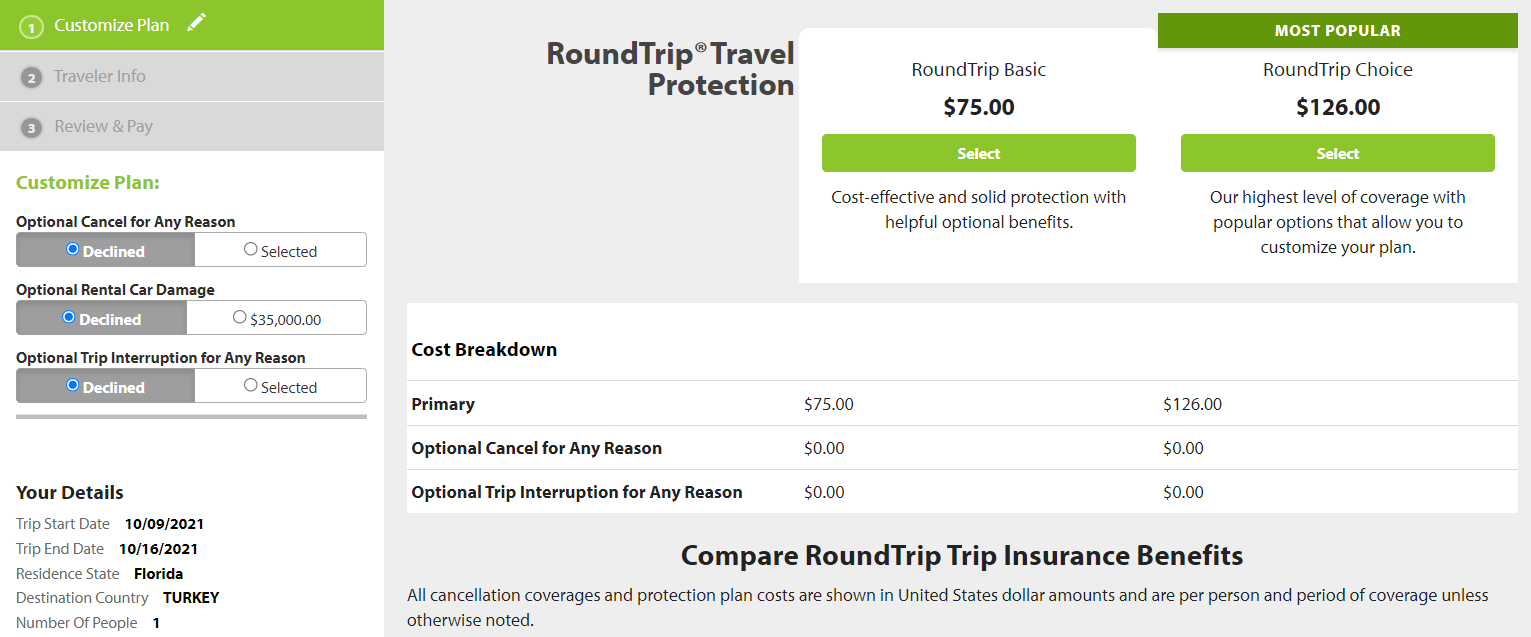

Seven Corners

Seven Corners offers a wide variety of policies. Here are the policies that are most applicable to travelers on a single international trip.

Seven Corners also offers many other types of travel insurance, including an annual multi-trip plan. You can choose coverage for trips of up to 30, 45 or 60 days when purchasing an annual multi-trip plan.

See Seven Corner's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Typically, Seven Corners won't cover losses incurred because of a preexisting medical condition. However, the RoundTrip Choice plan offers a preexisting condition exclusion waiver. To be eligible for this waiver, you must meet all of the following conditions:

- You buy this plan within 20 days of making your initial trip payment or deposit.

- You or your travel companion are medically able and not disabled from travel when you pay for this plan or upgrade your plan.

- You update the coverage to include the additional cost of subsequent travel arrangements within 15 days of paying your travel supplier for them.

- Seven Corners offers the ability to purchase optional sports and golf equipment coverage. If purchased, this extra insurance will reimburse you for the cost of renting sports or golf equipment if yours is lost, stolen, damaged or delayed by a common carrier for six or more hours. However, Seven Corners must authorize the expenses in advance.

- You can add cancel for any reason coverage or trip interruption for any reason coverage to RoundTrip plans. Although some other providers offer cancel for any reason coverage, trip interruption for any reason coverage is less common.

- Seven Corners' RoundTrip Choice policy offers a political or security evacuation benefit that will transport you to the nearest safe place or your residence under specific conditions. You can also add optional event ticket registration fee protection to the RoundTrip Choice policy.

Purchase your policy here: Seven Corners .

World Nomads

World Nomads is popular with younger, active travelers because of its flexibility and adventure-activities coverage on the Explorer plan. Unlike many policies offered by other providers, you don't need to estimate prepaid costs when purchasing the insurance to have access to trip interruption and cancellation insurance.

World Nomads offers two single-trip plans.

World Nomads has a page dedicated to coronavirus coverage , so be sure to view it before buying a policy.

World Nomads won't cover losses incurred because of a preexisting medical condition (except emergency evacuation and repatriation of remains) that existed within 90 days of the coverage effective date. Unlike many other providers, World Nomads doesn't offer a waiver.

- World Nomads' policies cover more adventure sports than most providers, so activities such as bungee jumping are included. The Explorer policy covers almost any adventure sport, including skydiving, stunt flying and caving. So, if you partake in adventure sports while traveling, the Explorer policy may be a good fit.

- World Nomads' policies provide nonmedical evacuation coverage for transportation expenses if there is civil or political unrest in the country you are visiting. The coverage may also transport you home if there is an eligible natural disaster or a government expels you.

Purchase your policy here: World Nomads .

Other options for buying travel insurance

This guide details the policies of eight providers with the information available at the time of publication. There are many options when it comes to travel insurance, though. To compare different policies quickly, you can use a travel insurance aggregator like InsureMyTrip to search. Just note that these search engines won't show every policy and every provider, and you should still research the provided policies to ensure the coverage fits your trip and needs.

You can also purchase a plan through various membership associations, such as USAA, AAA or Costco. Typically, these organizations partner with a specific provider, so if you are a member of any of these associations, you may want to compare the policies offered through the organization with other policies to get the best coverage for your trip.

Related: Should you get travel insurance if you have credit card protection?

Is travel insurance worth getting?

Whether you should purchase travel insurance is a personal decision. Suppose you use a credit card that provides travel insurance for most of your expenses and have medical insurance that provides adequate coverage abroad. In that case, you may be covered enough on most trips to forgo purchasing travel insurance.

However, suppose your medical insurance won't cover you at your destination and you can't comfortably cover a sizable medical evacuation bill or last-minute flight home . In that case, you should consider purchasing travel insurance. If you travel frequently, buying an annual multi-trip policy may be worth it.

What is the best COVID-19 travel insurance?

There are various aspects to keep in mind in the age of COVID-19. Consider booking travel plans that are fully refundable or have modest change or cancellation fees so you don't need to worry about whether your policy will cover trip cancellation. This is important since many standard comprehensive insurance policies won't reimburse your insured expenses in the event of cancellation if it's related to the fear of traveling due to COVID-19.

However, if you book a nonrefundable trip and want to maintain the ability to get reimbursed (up to 75% of your insured costs) if you choose to cancel, you should consider buying a comprehensive travel insurance policy and then adding optional cancel for any reason protection. Just note that this benefit is time-sensitive and has eligibility requirements, so not all travelers will qualify.

Providers will often require CFAR purchasers insure the entire dollar amount of their travels to receive the coverage. Also, many CFAR policies mandate that you must cancel your plans and notify all travel suppliers at least 48 hours before your scheduled departure.

Likewise, if your primary health insurance won't cover you while on your trip, it's essential to consider whether medical expenses related to COVID-19 treatment are covered. You may also want to consider a MedJet medical transport membership if your trip is to a covered destination for coronavirus-related evacuation.

Ultimately, the best pandemic travel insurance policy will depend on your trip details, travel concerns and your willingness to self-insure. Just be sure to thoroughly read and understand any terms or exclusions before purchasing.

What are the different types of travel insurance?

Whether you purchase a comprehensive travel insurance policy or rely on the protections offered by select credit cards, you may have access to the following types of coverage:

- Baggage delay protection may reimburse for essential items and clothing when a common carrier (such as an airline) fails to deliver your checked bag within a set time of your arrival at a destination. Typically, you may be reimbursed up to a particular amount per incident or per day.

- Lost/damaged baggage protection may provide reimbursement to replace lost or damaged luggage and items inside that luggage. However, valuables and electronics usually have a relatively low maximum benefit.

- Trip delay reimbursement may provide reimbursement for necessary items, food, lodging and sometimes transportation when you're delayed for a substantial time while traveling on a common carrier such as an airline. This insurance may be beneficial if weather issues (or other covered reasons for which the airline usually won't provide compensation) delay you.

- Trip cancellation and interruption protection may provide reimbursement if you need to cancel or interrupt your trip for a covered reason, such as a death in your family or jury duty.

- Medical evacuation insurance can arrange and pay for medical evacuation if deemed necessary by the insurance provider and a medical professional. This coverage can be particularly valuable if you're traveling to a region with subpar medical facilities.

- Travel accident insurance may provide a payment to you or your beneficiary in the case of your death or dismemberment.

- Emergency medical insurance may provide payment or reimburse you if you must seek medical care while traveling. Some plans only cover emergency medical care, but some also cover other types of medical care. You may need to pay a deductible or copay.

- Rental car coverage may provide a collision damage waiver when renting a car. This waiver may reimburse for collision damage or theft up to a set amount. Some policies also cover loss-of-use charges assessed by the rental company and towing charges to take the vehicle to the nearest qualified repair facility. You generally need to decline the rental company's collision damage waiver or similar provision to be covered.

Should I buy travel health insurance?

If you purchase travel with credit cards that provide various trip protections, you may not see much need for additional travel insurance. However, you may still wonder whether you should buy travel medical insurance.

If your primary health insurance covers you on your trip, you may not need travel health insurance. Your domestic policy may not cover you outside the U.S., though, so it's worth calling the number on your health insurance card if you have coverage questions. If your primary health insurance wouldn't cover you, it's likely worth purchasing travel medical insurance. After all, as you can see above, travel medical insurance is often very modestly priced.

How much does travel insurance cost?

Travel insurance costs depend on various factors, including the provider, the type of coverage, your trip cost, your destination, your age, your residency and how many travelers you want to insure. That said, a standard travel insurance plan will generally set you back somewhere between 4% and 10% of your total trip cost. However, this can get lower for more basic protections or become even higher if you include add-ons like cancel for any reason protection.

The best way to determine how much travel insurance will cost is to price out your trip with a few providers discussed in the guide. Or, visit an insurance aggregator like InsureMyTrip to quickly compare options across multiple providers.

When and how to get travel insurance

For the most robust selection of available travel insurance benefits — including time-sensitive add-ons like CFAR protection and waivers of preexisting conditions for eligible travelers — you should ideally purchase travel insurance on the same day you make your first payment toward your trip.

However, many plans may still offer a preexisting conditions waiver for those who qualify if you buy your travel insurance within 14 to 21 days of your first trip expense or deposit (this time frame may vary by provider). If you don't need a preexisting conditions waiver or aren't interested in CFAR coverage, you can purchase travel insurance once your departure date nears.

You must purchase coverage before it's needed. Some travel medical plans are available for purchase after you have departed, but comprehensive plans that include medical coverage must be purchased before departing.

Additionally, you can't buy any medical coverage once you require medical attention. The same applies to all travel insurance coverage. Once you recognize the need, it's too late to protect your trip.

Once you've shopped around and decided upon the best travel insurance plan for your trip, you should be able to complete your purchase online. You'll usually be able to download your insurance card and the complete policy shortly after the transaction is complete.

Related: 7 times your credit card's travel insurance might not cover you

Bottom line

Not all travel insurance policies and providers are equal. Before buying a plan, read and understand the policy documents. By doing so, you can choose a plan that's appropriate for you and your trip — including the features that matter most to you.

For example, if you plan to go skiing or rock climbing, make sure the policy you buy doesn't contain exclusions for these activities. Likewise, if you're making two back-to-back trips during which you'll be returning home for a short time in between, be sure the plan doesn't terminate coverage at the end of your first trip.

If you're looking to cover a sudden recurrence of a preexisting condition, select a policy with a preexisting condition waiver and fulfill the requirements for the waiver. After all, buying insurance won't help if your policy doesn't cover your losses.

Disclaimer : This information is provided by IMT Services, LLC ( InsureMyTrip.com ), a licensed insurance producer (NPN: 5119217) and a member of the Tokio Marine HCC group of companies. IMT's services are only available in states where it is licensed to do business and the products provided through InsureMyTrip.com may not be available in all states. All insurance products are governed by the terms in the applicable insurance policy, and all related decisions (such as approval for coverage, premiums, commissions and fees) and policy obligations are the sole responsibility of the underwriting insurer. The information on this site does not create or modify any insurance policy terms in any way. For more information, please visit www.insuremytrip.com .

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

11 Best Travel Insurance Companies in April 2024

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

If the past few years have shown us anything, it’s that travelers need to be prepared for the unexpected — from a pandemic to flight troubles to the crowded airport terminals so many of us have encountered.

Whether you’re looking for an international travel insurance plan, emergency medical care or a policy that includes extreme sports, these are the best travel insurance providers to get you covered.

How we found the best travel insurance

We looked at quotes from various companies for a 10-day trip to Mexico in September 2024. The traveler was a 55-year-old woman from Florida who spent $3,000 total on the trip, including airfare.

On average, the price of each company’s most basic coverage plan was $126.53. The costs displayed below do not include optional add-ons, such as Cancel For Any Reason coverage or pre-existing medical condition coverage.

Read our full analysis about the average cost of travel insurance so you can budget better for your next trip.

However, depending on the plan, you may be able to customize at an added cost.

As we continue to evaluate more travel insurance companies and receive fresh market data, this collection of best travel insurance companies is likely to change. See our full methodology for more details.

Best insurance companies

Types of travel insurance

What does travel insurance cover, what’s not covered, how much does it cost, do i need travel insurance, how to choose the best travel insurance policy, what are the top travel destinations in 2024, more resources for travel insurance shoppers, methodology, best travel insurance overall: berkshire hathaway travel protection.

Berkshire Hathaway Travel Protection

- ExactCare Value (basic) plan is among the least expensive we surveyed.

- Speciality plans available for road trips, luxury travel, adventure activities, flights and cruises.

- Company may reimburse claimants faster than average, including possible same-day compensation.

- Multiple "Trip Delay" coverage types might make claims confusing.

- Cheapest plan only includes fixed amounts for its coverage.

Under the direction of chair and CEO Warren Buffett, Berkshire Hathaway Travel Protection has been around since 2014. Its plans provide numerous opportunities for travelers to customize coverage to their needs.

At $135 for our sample trip, the ExactCare Value (basic) plan from Berkshire Hathaway Travel Protection offers protection roughly $10 above the average price.

Want something cheaper? Air travelers looking for inexpensive, less comprehensive protections might opt for a basic AirCare plan that includes fixed amounts for its coverage .

Read our full review of Berkshire Hathaway .

What else makes Berkshire Hathaway Travel Protection great:

Pre-existing medical condition exclusion waivers available at no extra cost.

Plans available for travelers going on a cruise, participating in extreme sports or taking a luxury trip.

ExactCare Value (basic) plan was among the least expensive we surveyed.

Best for emergency medical coverage: Allianz Global Assistance

Annual or single-trip policies are available.

- Multiple types of insurance available.

- All plans include access to a 24/7 assistance hotline.

- More expensive than average.

- CFAR upgrades are not available.

- Rental car protection is only available by adding the One Trip Rental Car protector to your plan or by purchasing a standalone rental car plan.

Allianz Global Assistance is a reputable travel insurance company offering plans for over 25 years. Customers can choose from a variety of single and annual policies to fit their needs. On top of comprehensive coverage, some travelers might opt for the more affordable OneTrip Cancellation Plus, which is geared toward domestic travelers looking for trip protections but don’t need post-departure benefits like emergency medical or baggage lost.

For our test trip, Allianz Global Assistance’s basic coverage cost $149, about $22 above average.

What else makes Allianz Global Assistance great:

Annual and single-trip plans.

Plans are available for international and domestic trips.

Stand-alone and add-on rental car damage product available.

Read our full review of Allianz Global Assistance .

Best for travelers with pre-existing medical conditions: Travel Guard by AIG

Travel Guard by AIG

- Offers last-minute coverage.

- Pre-Existing Medical Conditions Exclusion Waiver available at all plan levels.

- Plan available for business travelers.

- Cancel For Any reason coverage only available for higher-level plans, and only reimburses up to 50% of the trip cost.

- Trip interruption coverage doesn't apply to trips paid for with points and miles.

Travel Guard by AIG offers a variety of plans and coverages to fit travelers’ needs. On top of more standard trip protections like trip cancellation, interruption, baggage and medical coverage, the Cancel For Any Reason upgrade is available on certain Travel Guard plans, which allows you to cancel a trip for any reason and get 50% of your nonrefundable deposit back as long as the trip is canceled at least two days before the scheduled departure date.

At $107 for our sample trip, the Essential plan was below average, saving roughly $20.

What else makes Travel Guard by AIG great:

Three comprehensive plans and a Pack N' Go plan for last-minute travelers who don't need cancellation benefits.

Flight protection, car rental, and medical evacuation coverage, as well as annual plans available.

Pre-existing medical conditions exclusion waiver available on all plan levels, as long as it's purchased within 15 days.

Read our full review of Travel Guard by AIG .

Best for those who pack expensive equipment: Travel Insured International

Travel Insured International

- Higher-level plan include optional add-ons for event tickets and for electronic equipment

- Rental car protection add-on for just $8 per day, even on lower-level plan.

- Many of the customizations are only available on the higher-tier plan.

- Coverage cost comes in above average in our latest analysis.

Travel Insured International offers several customization options. For instance, those going to see a show may want to add on event ticket registration fee protection. Traveling with expensive gear?Consider adding on coverage for electronic equipment for up to $2,000 in coverage.