At Morgan Stanley, we lead with exceptional ideas. Across all our businesses, we offer keen insight on today's most critical issues.

Personal Finance

Learn from our industry leaders about how to manage your wealth and help meet your personal financial goals.

Market Trends

From volatility and geopolitics to economic trends and investment outlooks, stay informed on the key developments shaping today's markets.

Technology & Disruption

Whether it’s hardware, software or age-old businesses, everything today is ripe for disruption. Stay abreast of the latest trends and developments.

Sustainability

Our insightful research, advisory and investing capabilities give us unique and broad perspective on sustainability topics.

Diversity & Inclusion

Multicultural and women entrepreneurs are the cutting-edge leaders of businesses that power markets. Hear their stories and learn about how they are redefining the terms of success.

Wealth Management

Investment Banking & Capital Markets

Sales & Trading

Investment Management

Morgan Stanley at Work

Sustainable Investing

Inclusive Ventures Group

Morgan Stanley helps people, institutions and governments raise, manage and distribute the capital they need to achieve their goals.

We help people, businesses and institutions build, preserve and manage wealth so they can pursue their financial goals.

We have global expertise in market analysis and in advisory and capital-raising services for corporations, institutions and governments.

Global institutions, leading hedge funds and industry innovators turn to Morgan Stanley for sales, trading and market-making services.

We offer timely, integrated analysis of companies, sectors, markets and economies, helping clients with their most critical decisions.

We deliver active investment strategies across public and private markets and custom solutions to institutional and individual investors.

We provide comprehensive workplace financial solutions for organizations and their employees, combining personalized advice with modern technology.

We offer scalable investment products, foster innovative solutions and provide actionable insights across sustainability issues.

From our startup lab to our cutting-edge research, we broaden access to capital for diverse entrepreneurs and spotlight their success.

Core Values

Giving Back

Sponsorships

Since our founding in 1935, Morgan Stanley has consistently delivered first-class business in a first-class way. Underpinning all that we do are five core values.

Everything we do at Morgan Stanley is guided by our five core values: Do the right thing, put clients first, lead with exceptional ideas, commit to diversity and inclusion, and give back.

Morgan Stanley leadership is dedicated to conducting first-class business in a first-class way. Our board of directors and senior executives hold the belief that capital can and should benefit all of society.

From our origins as a small Wall Street partnership to becoming a global firm of more than 80,000 employees today, Morgan Stanley has been committed to clients and communities for 87 years.

The global presence that Morgan Stanley maintains is key to our clients' success, giving us keen insight across regions and markets, and allowing us to make a difference around the world.

Morgan Stanley is differentiated by the caliber of our diverse team. Our culture of access and inclusion has built our legacy and shapes our future, helping to strengthen our business and bring value to clients.

Our firm's commitment to sustainability informs our operations, governance, risk management, diversity efforts, philanthropy and research.

At Morgan Stanley, giving back is a core value—a central part of our culture globally. We live that commitment through long-lasting partnerships, community-based delivery and engaging our best asset—Morgan Stanley employees.

As a global financial services firm, Morgan Stanley is committed to technological innovation. We rely on our technologists around the world to create leading-edge, secure platforms for all our businesses.

At Morgan Stanley, we believe creating a more equitable society begins with investing in access, knowledge and resources to foster potential for all. We are committed to supporting the next generation of leaders and ensuring that they reflect the diversity of the world they inherit.

Why Morgan Stanley

How We Can Help

Building a Future We Believe In

Get Started

Stay in the Know

For 88 years, we’ve had a passion for what’s possible. We leverage the full resources of our firm to help individuals, families and institutions reach their financial goals.

At Morgan Stanley, we focus the expertise of the entire firm—our advice, data, strategies and insights—on creating solutions for our clients, large and small.

We have the experience and agility to partner with clients from individual investors to global CEOs. See how we can help you work toward your goals—even as they evolve over years or generations.

At Morgan Stanley, we put our beliefs to work. We lead with exceptional ideas, prioritize diversity and inclusion and find meaningful ways to give back—all to contribute to a future that benefits our clients and communities.

Meet one of our Financial Advisors and see how we can help you.

Get the latest insights, analyses and market trends in our newsletter, podcasts and videos.

- Opportunities

- Technology Professionals

Experienced Financial Advisors

We believe our greatest asset is our people. We value our commitment to diverse perspectives and a culture of inclusion across the firm. Discover who we are and the right opportunity for you.

Students & Graduates

A career at Morgan Stanley means belonging to an ideas-driven culture that embraces new perspectives to solve complex problems. See how you can make meaningful contributions as a student or recent graduate at Morgan Stanley.

Experienced Professionals

At Morgan Stanley, you’ll find trusted colleagues, committed mentors and a culture that values diverse perspectives, individual intellect and cross-collaboration. See how you can continue your career journey at Morgan Stanley.

At Morgan Stanley, our premier brand, robust resources and market leadership can offer you a new opportunity to grow your practice and continue to fulfill on your commitment to deliver tailored wealth management advice that helps your clients reach their financial goals.

- Dec 21, 2022

2023 Outlook: Business Travel Bounces Back

Corporate travel budgets are recovering to pre-covid levels, our new survey finds. see where companies are spending in the year ahead..

After grinding to a near halt during the COVID-19 pandemic, business trips—and profits for hotels and airlines catering to higher-paying corporate clients—are bouncing back even beyond pre-pandemic levels, per a recent survey from Morgan Stanley Research.

Despite higher airfares and room rates, the survey of 100 global corporate travel managers found that many respondents believe their company's travel expenditures are already back to pre-pandemic levels and will continue to grow. The biggest demand is coming from small companies, which means lower-cost airlines may benefit the more than their bigger peers.

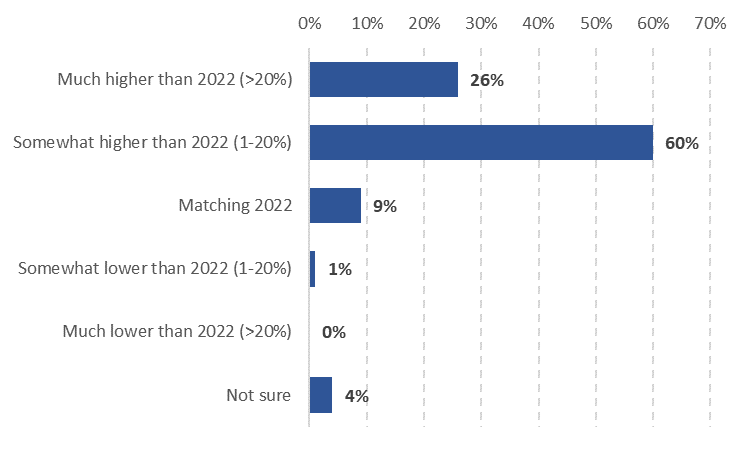

“Travel budgets are expected to see a noticeable improvement in 2022, with 2023 nearly back to ‘normal,’” says Ravi Shanker, an equity analyst covering North American transportation. “Most interesting is that nearly half of the respondents expect 2023 budgets to increase versus 2019 overall. And of those that expect an increase in budgets, the majority believe 2023 budgets will be between 6% to 10% higher than 2019.”

Overall travel budgets show an improvement over previous surveys, with 2023 budgets expected to be 98% of 2019 levels on average.

Survey Highlights

- Smaller companies lead demand for corporate travel. More than two-thirds (68%) of companies with under $1 billion in annual revenue expect travel budgets to increase next year, versus just 41% of companies with annual revenues over $16 billion. Similarly, 32% of smaller companies said travel budgets had returned to pre-pandemic levels compared with 23% of big firms. “This trend could likely favor low-cost carriers, as smaller enterprises tend to be more localized and require less long-haul travel,” says Shanker. “However, the legacy carriers with strong corporate exposure should see gains as well.”

Nearly a quarter of both large and small companies say their firms are already back to pre-COVID travel levels, and 34% anticipate a full recovery by the end of 2023.

ESG Rate of Change

Holiday budgets hit by inflation, seeing a peak for food prices.

- Airfares are higher, but that’s not a drag on bookings. On average, corporate airfares are expected to be about 9% higher than pre-pandemic prices. “Clearly the expected increase in corporate airfares is not having a major impact on corporate travel as passenger volume is expected to be basically flat versus 2019,” says Shanker.

- Room rates will continue to rise, though not as fast as they have recently. As of this October, market room rates had spiked 20% to 25% over 2019. Next year they will rise even more, though by an average of just 8%, say respondents (9% in the U.S. and U.K.; 5% to 6% in Latin America, Asia and Africa).

- Hotels face economic and competitive headwinds. While overall travel budgets are growing, companies are cutting costs by trading down when it comes to accommodations. (Historically, budget hotels outperform upscale lodging in tough economic times.) Alternative sources of accommodation also threaten traditional hotels, with 31% of respondents saying they intend to use short-term rental services in the next year.

- Virtual meetings aren’t going away. Almost 18% of corporate travel will be replaced with virtual meetings, falling slightly to 17% in 2024, suggesting a degree of permanence in the shift with companies recognizing the benefits of virtual meetings ranging from cost savings to lower carbon footprints. Expect companies providing collaboration software to gain from this shift.

For more Morgan Stanley Research insights and analysis on global travel, ask your Morgan Stanley representative or Financial Advisor for the full reports, “Global Corporate Travel Survey: Snapping Back" (Nov. 8, 2022) and “Global Corporate Travel Survey: 2023 Travel Budgets Nearly Back to 2019 Levels, but ~20% of Meetings Could Still Shift to Virtual” (Nov. 8. 2022). Morgan Stanley Research clients can access the reports directly here and here . Plus more Ideas from Morgan Stanley’s thought leaders.

Sign up to get Morgan Stanley Ideas delivered to your inbox.

*Invalid email address

Thank You for Subscribing!

Would you like to help us improve our coverage of topics that might interest you? Tell us about yourself.

Dividends: A Volatility Shield

Dividend-paying stocks with steady distribution growth can offer outsized contributions to long-term portfolio returns.

Global Outlook: Tech & Beyond

Disruption in connected advertising, a digital-driven economic boom in India and more trends in tech, media and telecom.

Building Credit for Immigrants

Wemimo Abbey and Samir Goel present credit solutions for immigrants financially marginalized by America’s credit validation system.

After slow end to 2022, the business travel outlook is turning more positive for 2023

There is a growing sense that lower levels of business flying are here to stay, with many still expecting top executives to set corporate flying reduction targets, driven by cost savings, changing travel habits and sustainability needs.

Messaging regarding the recovery of the business travel segment remains mixed.

Since the onset of the COVID-19 pandemic, a number of the industry's leading voices have claimed that business travel will never fully recover due to changing working habits - namely, remote working and digital nomadism; company cost reduction; and a growing awareness of environmental issues.

Indeed, international business travel has been recovering at a much slower rate than leisure tourism.

- Recovery in business travel slowed in 2H2022, but a rapid recovery is expected for 2023.

- Confidence in business travel has nearly fully recovered to pre-pandemic levels.

- Suppliers are highly optimistic about the outlook for business travel, with expectations of increased spending by corporate customers.

- Customer meetings and new business prospects are expected to drive business travel investment.

- The recovery in US business travel spending has been driven by increased prices for airfares, car rentals, and accommodation.

- COVID-19 has brought changes to the demand for business travel, including hybrid and remote working arrangements, additional layers of corporate travel approvals, and sustainability considerations.

- Recovery in business travel slowed in 2H2022...but rapid recovery is expected for 2023.

- Confidence in business travel nearly fully recovered to the levels from before the COVID-19 pandemic.

- Suppliers are highly optimistic about the outlook for business travel; higher spend trend echoed by travel buyers and procurement professionals.

- Customer meetings and new business prospects to hold weight of business travel investment.

- A large part of the recovery in US business travel spending has been due to the growth of prices - such as for airfares, car rentals and accommodation.

- COVID-19 has produced a range of changes that have modified the landscape of demand for business travel globally.

- Hybrid and remote working arrangements have persisted for a large proportion of workforces globally.

- Additional layers of corporate travel approvals and duty of care arrangements introduced during the pandemic have proved stubborn to remove.

- Sustainability considerations are also weighing much more heavily on travel activity.

Recovery in business travel slowed in 2H2022...

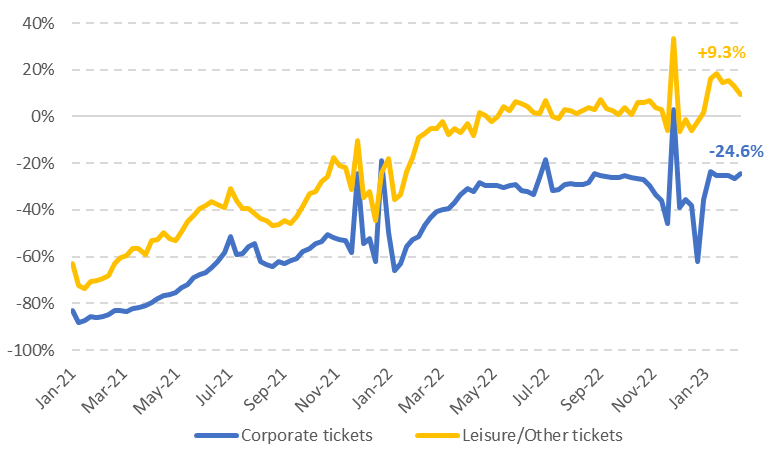

The global recovery in business travel experienced a pause over much of 2H2022.

After a rapid bounce-back of business travel during 1H2022, the expectation had largely been that the sector would have a continued, if steady, recovery over the second half of the year. However, in the face of rising travel costs due to inflationary pressures, airline operational chaos across multiple regions, and wider concerns about the macroeconomic outlook - businesses revised their plans and travel and budgets were largely static.

This was clearly evident when listening to comments from some of the leading airlines in the US , where business travel recovery had been strong.

In early Dec-2022 United Airlines CEO Scott Kirby stated that business travel had "plateaued" in late 2022, adding that this was "indicative of pre-recessionary behaviour". Delta Air Lines President Glen Hauenstein reported at the start of Jan-2023 that corporate travel demand had been "steady" over 4Q2022, with domestic corporate sales recovering to 80% of 4Q2019 levels.

Alaska Airlines CEO Ben Minicucci reported that large Silicon Valley technology companies had largely "turned off" business travel in late 2022.

Airlines Reporting Corporation : US corporate and leisure ticket bookings (percentage vs 2019), 2021-2023

Source: Airlines Reporting Corporation .

...but rapid recovery expected for 2023

Despite the recent slowing performance, there is an increasing undercurrent of positive expectations for business travel for 2023.

Airlines, corporate travel management organisations, travel agencies and business travel associations are now pointing to a rapid recovery for 2023, particularly when it comes to business spending.

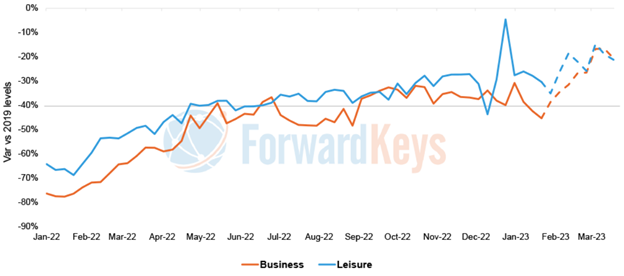

Global forward-ticketing data from Forward Keys indicates that after a slowing in business ticket sales over 2H2022, forward sales indicate that corporate air travel is due to accelerate through the early part of 2023.

ForwardKeys: forward business and leisure air ticket data, 2022-2023

Source: ForwardKeys.

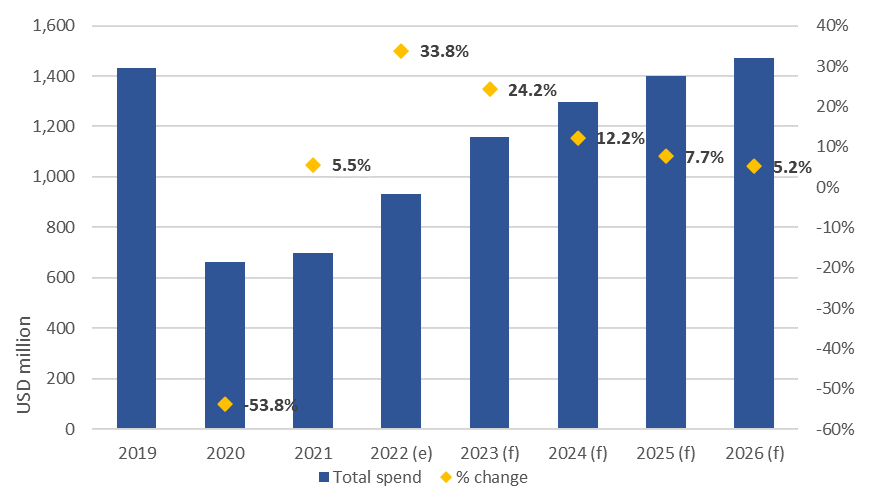

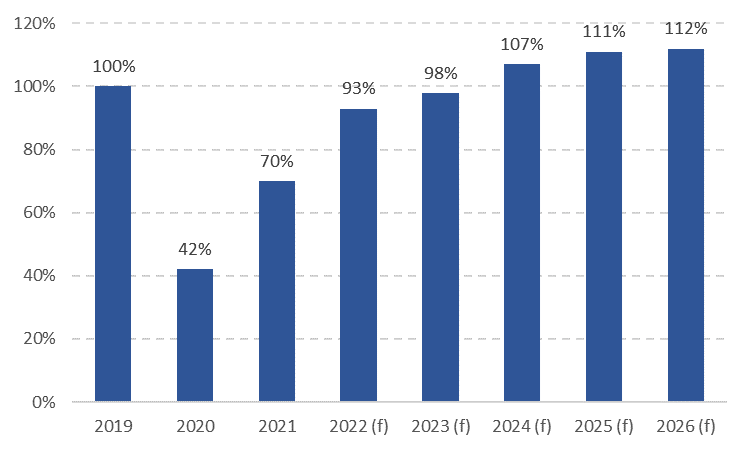

The Global Business Travel Association (GNTA) projects global business travel spending of just under USD1.2 trillion in 2023.

While this is still down, around USD273 billion down on 2019 levels (-19.1%), the outlook is for overall spending to increase 24.2% year-on-year for 2023.

GBTA : business travel spending outlook, 2019-2026

Source: Global Business Travel Association .

Confidence in business travel nearly fully recovered to levels before the pandemic

GBTA 's Business Travel Outlook Poll for 1Q2023 found expectations for business travel in 2023, with confidence nearly fully recovered to levels before the COVID pandemic.

Of travel buyers - 91% reported that they feel that employees at their company are now either 'somewhat willing' or 'very willing' to travel for work in the current environment.

This is up from just 64% of reported workers who were willing to travel in Feb-2022, and 86% in Oct-2022.

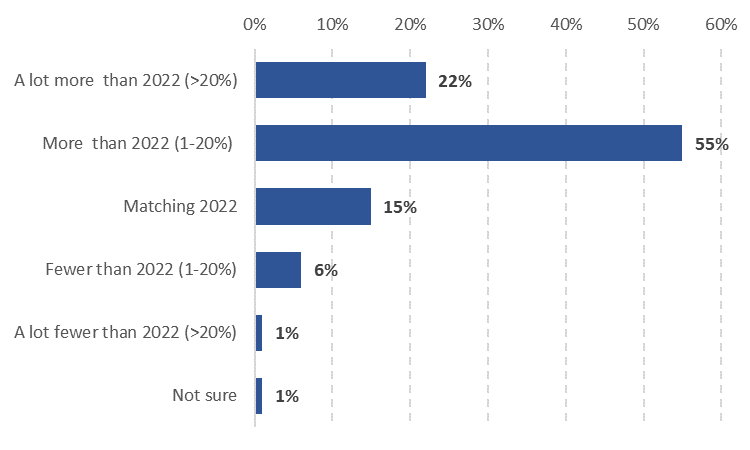

According to GBTA 's polling, 78% travel managers globally expect their companies will engage in more business travel in 2023.

Expectations about travel volumes increases are almost uniform between the North America , Latin America , Europe and the Asia Pacific regions.

Just 7% of travel managers expect reduced travel.

Reduced travel expectations are lowest with travel managers in North America (6%) and the Asia Pacific (7%), and higher with managers in Europe (10%) and Latin America (13%).

Travel buyer/procurement: professional expectations for 2023 business travel volumes

More travel suppliers expect increased spending on travel by their corporate customers

Further to this, GBTA 's data shows that 86% of travel suppliers expect spending on travel by their corporate customers will increase in 2023 - up from 80% in the association's Oct-2022 survey.

This confidence is high, regardless of region - all travel suppliers surveys in the Asia Pacific expect spending to be somewhat or much higher than it was in 2022, followed by 91% in Latin America , 90% in Europe and 85% in North America .

Just 1% expect reduced spending by corporate customers.

Travel supplier/travel management company: expectations for 2023 business travel spending

Suppliers are also highly optimistic about the outlook for business travel.

According to GBTA polling, 24% report feeling 'very optimistic' about the industry's path to recovery, and 65% are optimistic. Just 3% report they are pessimistic about the outlook.

Travel suppliers expectations about higher spend are echoed by travel buyers and procurement professionals. Of those polled, 46% expect a higher budget for travel programmes for 2023 when compared to 2022, while 41% expect budgets will be about the same as the previous year.

Customer meetings and new business prospects to hold weight of business travel investment

The key area for business travel spending in 2023 is expected to be for trips for sales staff or account managers to meet with customers or new business prospects.

On average, travel managers estimate that their companies will allocate 28% of their travel spend for these purposes in 2023. This is followed by spending on trips for internal company meetings (19%) and spending on attending conferences, trade shows and other industry events (18%).

North American business travel to return to close to normal in 2023

The US Travel Association (USTA) project that the volume of business travel by air will recover to around 98% of pre-pandemic levels in 2023, with recovery back above 100% in 2024.

Domestic travel is at or above pre-pandemic levels, but international arrivals are still in recovery mode.

For 2022, inbound arrivals by foreign nationals into the US were down 24% compared to 2109. This was chiefly due to the slow rebound of traffic from the Asia Pacific , as well as some sluggishness in the early part of the year in Europe and parts of Latin America .

As of the start of Feb-2023, arrivals from mainland China were down 97% when compared to 2019, and arrivals from Hong Kong were still down by 80%.

Inbound travel from Japan was down 41.6%, and from Australia it was down 30.4%.

From Europe , UK arrivals were down 18.5%, while arrivals from Italy were still 14.2% below pre-pandemic levels and German arrivals were down 7%. Of the main Latin American markets, arrivals from Brazil were still a third below 2019 levels.

USTA estimates for Dec-2022 were that US business travel spending would be USD97 billion, which was an increase of 3% compared to pre-pandemic levels.

US business travel forecast: volume, percentage of 2019 levels, 2019-2026

Source: US Travel Association.

A large part of the recovery in US business travel spending has been due to the growth of prices, such as for airfares, car rentals and accommodation.

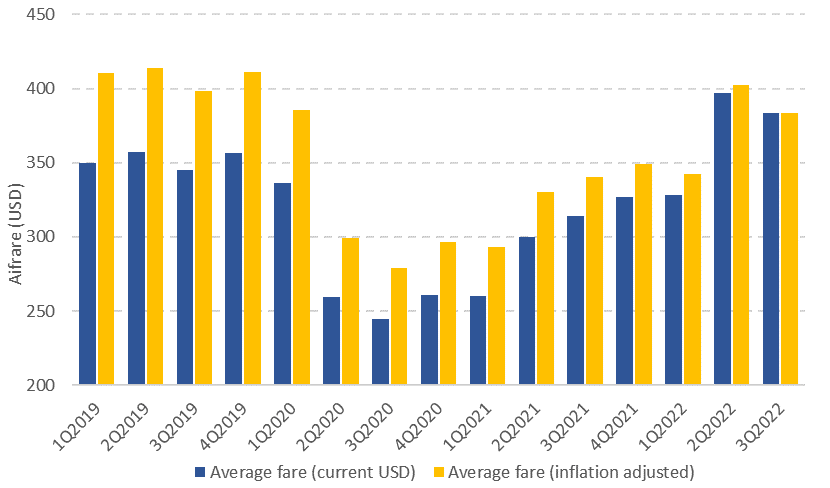

According to the USTA, airfares rose 28.5% year-on-year for the full year 2022.

US Bureau of Transport Statistics data shows US domestic fares averaged USD384 in 3Q2022. This is up from an (inflation adjusted) average domestic fare of USD279 in 3Q2020, an increase of 37.4% over the two-year period, and up 12.8% over the past 12 months.

US average domestic round trip airfares, by quarter, 1Q2019- 3Q2022

Source: US Bureau of Transportation Statistics.

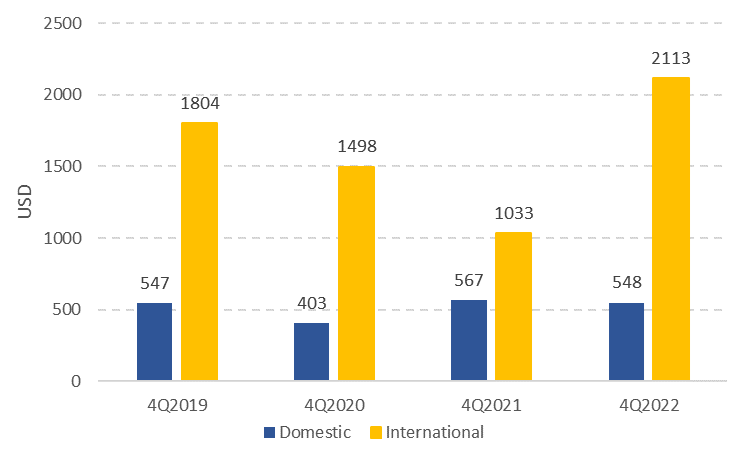

Data from the corporate travel solutions provider Emburse shows that average spend per round trip domestic business travel by air for 4Q2022 was USD548, putting it just ahead of 4Q2019 levels.

Spend per round trip on international business travel was significantly higher: USD2113 in 4Q2022, vs USD1804 in 4Q2019 (an increase of 17.1%).

Domestic and international air travel: average spend per round trip, 4Q2019-4Q2022

Source: Emburse.

New hope for full recovery in 2023

COVID-19 has produced a range of changes that have altered the landscape of demand for business travel globally - some of which have slowed the recovery, and others that are contributing to business travel coming back, albeit in modified form or with higher spending.

Hybrid and remote working arrangements have persisted for a large proportion of workforces globally, cutting into historical business travel volumes, while at the same time creating greater demand for 'bleisure' travel.

Although video conferencing technology became ubiquitous during the pandemic, enterprises continue to report strong demand for face-to-face meetings, particularly given the uncertainties in global supply chains and the need to train new staff working from remote locations.

Additional layers of corporate travel approvals and duty of care arrangements introduced during the pandemic have proved stubborn to remove - particularly in large corporations. The response has been to consolidate multiple smaller business trips into larger - and often more costly - single trips.

In this same vein, sustainability considerations are also weighing much more heavily on travel activity, but businesses have also shown greater willingness to spend money to be good corporate citizens and offset the impact of their travel.

Despite the structural trends and concerns about an economic slowdown in developed economies, business travel has renewed its upwards trend.

Although the recovery is happening more slowly than expected, and is still well below where most airlines would like it to be, there is renewed confidence in the recovery outlook for 2023.

Want More Analysis Like This?

Advertisement

Supported by

Business Travel’s Rebound Is Being Hit by a Slowing Economy

By the early fall, domestic business travel was back up to nearly two-thirds of its prepandemic level. But companies have now begun to cut back.

- Share full article

By Jane L. Levere

Business travel came back this year more strongly than most industry analysts had predicted in the depths of the pandemic, with domestic travel rebounding by this fall to about two-thirds of the 2019 level.

But in recent weeks, it appears to have hit a new hurdle — companies tightening their spending in a slowing economy.

Henry Harteveldt, a travel industry analyst for Atmosphere Research, said that corporate travel managers have told him in the last few weeks that companies have started to ban nonessential business travel and increase the number of executives needed to approve employee trips. He said he was now predicting that corporate travel would soften slightly for the rest of the year and probably remain tepid into the first quarter of 2023.

Mr. Harteveldt also said his conversations led him to believe that business travel would “come in below the levels airline executives discussed in their third-quarter earnings calls.”

Airlines were bullish on those earnings calls, a little over a month ago. Delta Air Lines, for one, said 90 percent of its corporate accounts “expect their travel to stay the same or increase” in the fourth quarter. United Airlines, too, said its strong third-quarter results suggested “durable trends for air travel demand that are more than fully offsetting any economic headwinds.”

Hotels, too, were optimistic. Christopher J. Nassetta, president and chief executive of Hilton, said on his earnings call that overall occupancy rates had reached more than 73 percent in the third quarter, with business travel showing growing strength.

The change in mood has come as the economy has more visibly slowed. Technology companies, in particular, have been announcing significant layoffs. Housing lenders have also been reducing staff, as rising mortgage rates cut into their business.

The travel industry has long relied on business travel for both its consistency and profitability, with companies often willing to spend more than leisure travelers. When the pandemic almost completely halted business travel in 2020, people were forced to meet via teleconference, and many analysts predicted that the industry would never fully recover.

But business travel did come back. As the economy reopened, companies realized that in-person meetings serve a purpose. In a survey taken in late September by the Global Business Travel Association, a trade group, corporate travel managers estimated that their employers’ business travel volume in their home countries was back up to 63 percent of prepandemic levels, and international business travel was at 50 percent of those levels.

One reason international business travel has not come back as strongly, Mr. Harteveldt said, is that some employers have imposed restrictions on high-priced business-class airline tickets for long-haul flights. He said employers are instead requiring travelers to take a cheaper connecting flight or to fly nonstop in premium economy or regular economy class.

“Travelers are telling managers they won’t fly long-haul in economy if they have to go directly to a meeting when they arrive,” Mr. Harteveldt said.

What will business travel look like in the next year?

Pandemic travel restrictions will probably play less of a role. A survey by Tourism Economics, U.S. Travel Association and J.D. Power released in October found that 42 percent of corporate executives had policies in place restricting business travel because of the pandemic, down from 50 percent in the second quarter. Over half expected pandemic-related business travel policies to be re-evaluated in the first half of 2023.

With Americans able to work remotely, many are combining professional and leisure travel, airline and hotel executives said on recent earnings calls. That was a big reason travel did not drop off in September, when the peak vacation period ended, as it used to in years past.

Jan Freitag, national director for hospitality market analytics at CoStar Group, said hotel occupancy by business travelers currently varies by market, with occupancies high in markets like Nashville, Miami and Tampa, Fla. — places where business travelers may well be taking “bleisure” trips. But hotel occupancies by business travelers are low in markets like Minneapolis, San Francisco and Houston.

Mr. Freitag said the lower hotel occupancies in some cities may reflect a lower return-to-office rate in those places, which reduces the ability to have in-person business meetings.

Mr. Freitag said he was “very bullish on group travel, trips for meetings, association events, to build internal culture.” Those trips will recover more quickly, he predicted, than individual business travel.

“It’s all about building relationships,” he said. “It’s very hard to do that online.”

On the other hand, short business meetings and employee training sessions may continue to be conducted online, which is less expensive than in person, said Grant Caplan, president of Procurigence, a consulting firm in Houston that advises companies on their spending for business travel, meetings and events.

Even as business travel has resumed, hotels, airlines and airports still have inadequate staffing. A survey of hoteliers by the American Hotel and Lodging Association, a trade group, released in October found that 87 percent of respondents were experiencing staffing shortages. Although that was an improvement over May , when 97 percent of respondents said they were short-staffed, the current findings do not bode well for smooth hotel stays.

Disruptions in flying, particularly in the United States and Europe — because of weather delays, inadequate flight crews or air traffic control and security issues at airports — have been notoriously high, particularly earlier this year.

Although “we can’t say that these disruptions have discouraged business travel, they have clearly complicated” the experience for travelers, said Kathy Bedell, senior vice president of the Americas and affiliate program for BCD Travel, a travel management company.

Kellie Kessler, a pharmaceutical clinical researcher in Raleigh, N.C., said the travel disruptions she faced this year were too much. She changed jobs recently to take one that requires her to travel on business 10 percent of the time, compared with 80 percent in her previous position.

“The reason I took a nontravel position is that I can count on one hand the number of on-time flights I had this year,” she said.

And flight disruptions have led to a decline in some road warriors’ loyalty to airlines, even those who have accrued elite status in the carriers’ frequent-flier programs.

“The disruptions overall have caused me to be less loyal to any one airline,” said Trey Thriffiley, chief executive of QIS Aviation Group a consulting company in Savannah, Ga., that advises individuals and companies about their use of private jets. He is also an elite member of the loyalty programs at Delta, United and American Airlines. “Instead of searching by preferred airline or even cheapest price,” he said, “I search for direct flights or connecting flights to cities closest to where I live that I can drive home from if I need to.”

Airlines’ bullish forecasts notwithstanding, some experts find prospects for business travel this fall and next year extremely murky.

They say they cannot accurately predict how strong business travel will be and what airfares and hotel room rates will look like because of many unknowns, including the duration of the war in Ukraine and its impact on the European and global economies; increasing gasoline and jet fuel prices; and rising inflation, recession fears and political uncertainty.

Mr. Harteveldt, the travel industry analyst, said the recovery of business travel varies by geographic region, with the United States rebounding faster than Europe.

He said the Chinese government could be using its reopening strategy “in a geopolitical way,” adding, “If a country is more friendly, China will grant access to that country’s business and leisure travelers rather than to travelers from countries with which China has greater political differences.”

He predicted that 2023 would be a “difficult year” for business travel unless the war in Ukraine “comes to an abrupt end and there is more certainty about oil and the price of jet fuel.” Also a factor, he said, could be decisions by companies that may have added too much staff during the pandemic to save money by reducing business travel rather than by laying people off.

“If there’s a symbol that can be used to describe the outlook for business travel in 2023, it’s a question mark,” he said. “No airline, travel management company or travel manager can be 100 percent certain what 2023 will bring right now. It’s one of the most confounding, confusing times to be in business travel, perhaps in decades.”

In a report issued in August, Mike Eggleton, director of research and intelligence at BCD Travel, had a similar take on the immediate future for business travel. “Producing a credible travel pricing forecast in the current environment is incredibly difficult,” he wrote. “The near-term travel outlook is more uncertain than ever. Volatility has never been so high and seems likely to persist. There’s vast variation in market performance and outlook.”

Going forward, Ms. Bedell said, perhaps the overriding question about business travel will be whether the trip is necessary.

“Client-facing and revenue-generating travel is taking a priority over internal meetings,” she said.

- Serviced Accommodation Guide 2023

- TMC Guide 2023

- The Knowledge

- Speaking Out

- Talking Travel

- Diary of a CTO

- Accommodation

- Sustainability Specialists

- Business Travel People Awards 2023

- Events calendar

- Business Travel People Awards

- People Awards: Meet the winners

- Destinations

- Latest issues

2023 Global Business Travel Forecast

The price of flights, hotels, ground transportation, and meetings and events will continue to rise this year and next, says a report from CWT and the GBTA

Global travel prices will continue to rise significantly in the remaining months of 2022 and throughout 2023, according to a report out today from CWT and the GBTA.

The price of meetings and events is expected to climb particularly sharply this year, while air fares and hotel rates are also being pushed up, driven by soaring fuel prices, staff shortages and inflationary pressures in raw material costs.

According to the 2023 Global Business Travel Forecast, prices will continue to rise next year but not at such a dramatic rate.

“Demand for business travel and meetings is back with a vengeance, of that there is absolutely no doubt,” said Patrick Andersen, CWT Chief Executive Officer.

“Labour shortages across the travel and hospitality industry, rising raw material prices, and greater awareness for responsible travel are all having an impact on services, but predicted pricing is, on the whole, on par with 2019.”

The report says the main forces exerting pressure on the economy and the business travel industry are Russia’s invasion of Ukraine, other geopolitical uncertainties, inflationary pressures, and the risk of further Covid outbreaks that could restrict business travel.

It also highlights that greater visibility at the point of sale for greener travel options, as well as carbon foot-printing and environmental impact assessment, as an opportunity for the travel industry to actively assist in responsible choice-making.

Meetings and events

The cost-per-attendee for meetings and events in 2022 is expected to be around 25% higher than 2019 and is forecast to rise by a further 7% in 2023.

Alongside pent-up demand, corporate events are now competing with many other types of events that were cancelled in 2020.

Demand is also being fuelled by the move to remote working, which means companies are now booking meeting spaces when staff gather in person.

Shorter lead times for events, varying from one to three months versus six to 12 months, are also contributing to this perfect storm, perhaps underscored by corporate concerns that the situation they face today could change very rapidly.

Air fares are expected to rise 48.5% in 2022 compared to 2021, but even with this steep price increase prices are expected to remain below pre-pandemic levels until 2023.

Following an increase of 48.5% in 2022, prices are expected to rise 8.4% in 2023.

Premium class tickets comprised over 7% of all tickets purchased in 2019. The share of premium class tickets fell to 6.5% in 2020 and to 4.5% in 2021 but have started to rise in 2022.

Through the first half of the year, premium tickets made up 6.2% of all tickets purchased.

The report says following two years of minimal to no expenditure, business travellers are likely to be willing to spend more on tickets, especially as availability reduces due to labour shortages.

Hotel rates

Hotel prices fell 13.3% in 2020 from 2019 and a further 9.5% in 2021, however the report expects them to rise 18.5% in 2022 followed by an 8.2% lift in 2023.

Hotel prices have already eclipsed 2019 levels in some areas such as Europe, the Middle East & Africa and North America and are expected do so globally by 2023.

Hotel rates have risen sharply in parts of the world including a 22% rise in North America – and a forecast 31.8% across Europe, the Middle East & Africa – driven by an accelerated recovery coupled with continued capacity constraints.

Hotel rate increases were initially driven by strong leisure travel in 2021 but group travel for corporate meetings and events is improving and transient business travel is similarly gaining healthy pace, putting further pressure on average daily hotel rates.

Ground transportation

Global car rental prices fell 2.5% in 2020 from 2019, before rising 5.1% in 2021.

Prices are expected to increase 7.3% in 2022, hitting new highs, and rise a further 6.8% in 2023.

The vehicle industry remains capacity constrained and rental agencies that reduced fleet sizes in the wake of the pandemic have not yet fully recovered – due in part to component shortages and supply chain disruptions that have reduced global auto production.

Rental agencies have reverted to buying used vehicles to increase fleet sizes and are keeping their vehicles longer.

Some agencies are also buying vehicles from auto-makers outside of their historically supported brands.

Skyrocketing prices, vehicle shortages and the need for visibility into carbon emissions from door-to-door are driving corporate travel managers to factor ground transport into full trip planning from the beginning.

* The 2023 Global Business Travel Forecast uses anonymised data generated by CWT and GBTA , with publicly available industry information, and econometric and statistical modelling developed by the Avrio Institute .

EDITOR'S CHOICE

Team tactics, paying the price, work and play, sustainability trends, more than a magazine.

For everyone involved in booking, buying, managing or arranging business travel and meetings.

OTHER TITLES

The Business Travel Magazine is published by BMI Publishing Ltd: 501 The Residence, No. 1 Alexandra Terrace, Guildford, GU1 3DA. Tel: 020 8649 7233

© BMI Publishing Plugged In Media

Business Travel Trends in 2023

While doing business face-to-face is bouncing back after the pandemic, the corporate travel industry is still very much in recovery. Here’s what to expect from business travel trends in 2023.

>> Related: Corporate Travel Trends from Our Survey with Skift <<

Source: Bloomberg Law

While there is no longer a shortage of travelers, there are new challenges:

- 87% of hotels have persistent staff shortages ( source )

- The United States has a deficit of about 8,000 pilots, or 11% of the total workforce ( source )

- TSA is in a hiring crisis amid stagnant wages ( source )

- Airfares are rising 5x faster than the overall inflation rate ( source )

- Hotel rates are up 19%

The net impact on business travelers? One in four flights have been delayed in 2023, and travel is costing ~30% more per trip.

Higher travel costs and unreliable flights will strain businesses in 2023

Unfortunately inflation, staffing shortages, and uncertain flights will affect not just the traveling employee, but also their manager and the finance department.

Business travelers should:

- Plan for long check-in and security lines at the airport, even with TSA pre check.

- Prepare for flights to sell out quickly. Book as soon as you can.

- Expect flights to be delayed – be conservative with your itinerary, and don’t schedule optimistic meetings or airport transfers.

- Prepare to rebook canceled flights. Save your company’s travel agency number in your phone so you don’t have to wait in line with hundreds of other stranded passengers.

>>Related: The New Era of Corporate T&E <<

Managers should:

- Prepare to manually field far more policy-exceptions for expensive flights.

- Triage travel or re-allocate budgets – with each trip costing ~30% more, you’ll exhaust travel and expense budgets faster.

Finance departments should:

- Urgently update travel policies, pricing limits, and per diems to reflect 2023 pricing.

- Create dynamic policy parameters that aren’t capped at arbitrary or outdated prices.

- Partner with travel agencies that have seasoned agents available 24/7 to rebook canceled flights.

- Explore incentives and reward employees who book under budget . On average, we see businesses trim 30% of their travel budget after implementing rewards.

Your California Privacy Choices

We use technologies, such as cookies, that gather information on our website. That information is used for a variety of purposes, such as to understand how visitors interact with our websites, or to serve advertisements on our websites or on other websites. The use of technologies, such as cookies, constitutes a ‘share’ or ‘sale’ of personal information under the California Privacy Rights Act. You can stop the use of certain third-party tracking technologies that are not considered our service providers by clicking on “Opt-Out” below or by broadcasting the global privacy control signal.

Note that due to technological limitations, if you visit our website from a different computer or device, or clear cookies on your browser that store your preferences, you will need to return to this screen to opt-out and/or rebroadcast the signal. You can find a description of the types of tracking technologies, and your options with respect to those technologies, by clicking “Learn more” below.

You have successfully opted-out.

Before you go, be sure you know:

This link takes you to an external website or app, which may have different privacy and security policies than TravelBank. We don't own or control the products, services or content found there.

Security Talk

The state of business travel in 2023.

As business travel slowly recovers, enterprise security teams must assess the evolving threat landscape to determine where their organization may be impacted.

LumiNola / E+ via Getty Images

Three years since the COVID-19 pandemic began, business travel spend remains below 2019 levels, according to a 2023 Deloitte report .

The firm’s survey of executives in U.S. and Europe found that businesses expect their travel spend to return to 71% of pre-COVID-19 levels by the end of the year, with a full return predicted for 2024 or 2025. The report notes that a return to 2019 levels could represent a 10% to 20% deficit in the business travel market overall, given the effects of inflation and lost gains.

Mapping business travel since the COVID-19 pandemic

In 2022, enterprise considerations for business travel revolved around vaccination rates, the emergence of COVID-19 variants, hospitalization rates and testing access, according to the “Adapting to Endemic COVID-19: The Outlook for Business Travel” report from the World Travel and Tourism Council and McKinsey & Company. According to Deloitte, travel restrictions also played a significant role in business travel plans, being ranked as the top factor slowing business travel in 2021 and 2022.

In 2023, factors limiting business travel have shifted toward economic considerations, with travel restrictions taking a lower priority in travel planning, according to the Deloitte report. The Deloitte report identified higher travel costs as the top inhibitor to business travel in 2023, followed by travel restrictions, reduced travel budgets, and client and employee unwillingness to travel.

Adapting security to current needs

It’s critical for security leaders to align themselves with their organization’s risk appetite for travel, especially as enterprise priorities regarding business travel continue to shift. Security magazine has followed a number of industry trends in this rapidly evolving threat landscape.

Travel risk management programs

As business travel outlooks shift, corporate security professionals looking to bolster their travel risk management practices can update existing or develop new internal standards for travel using current threat intelligence and risk appetites.

“To be truly effective, [the travel risk management program] needs to fully encompass proactive and reactive measures and be part of a company-wide approach to risk. It needs to involve numerous internal and external stakeholders working to the same end,” says Cal Pratt, Managing Director of Anvil Group.

Security leaders can work alongside stakeholders to mitigate risk holistically across the business, drawing in relevant departments to ensure a consistent approach to business travel.

Cybersecurity risks

In conversations about business travel returning to “normal,” security leaders should monitor for current threats, including those that have newly emerged or increased since 2019. In 2022, a Kryptowire report highlighted the cybersecurity risks of a number of travel apps, including Uber, Waze, Southwest Airlines and others.

Although business travel may have slowed over the past three years, the cybersecurity threat landscape hasn’t. Security leaders can incorporate cybersecurity best practices into their travel risk management programs to help reduce cyber risk, including monitoring application access via employee devices and consistently updating apps connected to the enterprise network.

Planning for resilience in business travel

Looking ahead, enterprise security leaders can prepare for the next evolution of business travel by monitoring shifts in the international threat landscape, cooperating with internal and external stakeholders on travel risk management, and tracking and mitigating emerging threats.

Extend the power of security by collaborating across and outside of the organization on resilience planning; geopolitical, physical and cyber threat intelligence; and preparing employees for a safe return to business travel.

Share This Story

Restricted Content

You must have JavaScript enabled to enjoy a limited number of articles over the next 30 days.

Related Articles

Mitigating the risks of business travel during the pandemic

Countering the Effects of New Age Terrorism on Business and Travel

Utah Governor Orders Visitors to the State to Reveal Travel Plans

Get our new emagazine delivered to your inbox every month., stay in the know on the latest enterprise risk and security industry trends..

Copyright ©2024. All Rights Reserved BNP Media.

Design, CMS, Hosting & Web Development :: ePublishing

Small and medium companies to boost business travel rebound in 2023

- Medium Text

Sign up here.

Reporting by Allison Lampert in Montreal and Abhijith Ganapavaram in Bangalore, editing by Ben Klayman and Bill Berkrot

Our Standards: The Thomson Reuters Trust Principles. New Tab , opens new tab

Thomson Reuters

Abhijith leads a team of reporters who cover aviation, legacy automakers, conglomerates, transportation and travel in the United States. An economics graduate, Abhijith has written stories across the manufacturing file with a focus on the aviation industry. In his previous role, he was part of the team that won the Reuters Journalist of the Year award under the speed category.

Barclays' annual shareholder meeting was disrupted by activists protesting against its alleged indirect links to violence in Gaza, with the bank's chair telling security staff to eject them from the event in Glasgow on Thursday.

Business Chevron

Trump vows to target EVs, LNG exports in meeting with oil CEOs, report says

Republican presidential candidate Donald Trump vowed to reverse dozens of the Biden administration's environmental rules and policies at a meeting with top U.S. oil executives, where he also asked them to raise $1 billion for his presidential campaign, the Washington Post reported on Thursday.

Expected Business Travel Trends in 2023

Business travel has always been an industry subject to constant change.

The travel and tourism industry has rightly prided itself on its ability to adapt to new circumstances and requirements, adopt innovative technology and working methods and pioneer new approaches to making the life of the business traveller more efficient, safe and productive.

However, in recognising that ability to be fleet of foot and welcoming to business travel trends, it’s also important to highlight the many significant challenges which travel managers have had to face and will continue to confront in maintaining high standards of global business travel .

How has business travel changed over the past few years?

It would be difficult to identify many – if any – sectors of the business world which have been unaffected by the pandemic.

But for the business travel industry and, particularly for international business travelers, the impact of the global health crisis has been genuinely unprecedented.

By its nature, the corporate travel market and the business trips which it enables, depend on the ability to move freely across cities, countries and continents.

That ability was, of course, severely limited at the height of the pandemic and, even now, restrictions remain due to the continued threat which the COVID-19 virus poses to global health.

That was highlighted again at the beginning of 2023 with the introduction by a number of European countries, including the UK, of COVID testing for passengers arriving from China.

It was a move which signaled how swiftly the corporate travel industry can be affected by events beyond its control and emphasised how important it is for travel management companies to be aware of the threat of similar health crises in future.

Besides the complexities with these health risks, we have seen various other changes off the back of the pandemic, some of which are listed below:

Depleted capacity of resource in airports, airlines & hotels causing problems with travel delays.

Frequent cancellations & adjustments to travel schedules due to the capacity issue.

Disruption is no longer limited to peak times, making it harder for business travellers to plan their business trips.

A need to overhaul travel policies.

Increased focus on sustainability.

On the plus side, the travel industry’s response once the worst of the pandemic had passed demonstrates how resilient the business travel sector is despite the challenges it faces.

At the same time, the pandemic is just one of many external events which has had – and will continue to have - a significant impact on travel companies and corporate travelers and on the way in which business trips are organised.

In the last year alone, further upheaval has been created as a result of unanticipated events such as the Russian attack on Ukraine, the cost of living crisis and the huge rise in energy prices. Not to mention various cyber attacks on SAS airlines and multiple rail & airline strikes which has led to capacity caps at numerous airports.

Added to that, the UK’s departure from the EU continues to create issues for business travellers and for the industry’s ability to retain and attract the people it requires to match the growing demand.

All these factors have, to some extent, led to a scenario in which many corporate travelers are now seeing airports, airlines, hotels and car fleets on their business trip all affected by reduced capacity and resources as well as more frequent cancellations and schedule changes.

And, like many other sectors, the corporate travel industry continues to work diligently to become more sustainable and to find ways to service business professionals while also reducing its carbon footprint.

In summary, the world of corporate travel management has changed immeasurably in the past two years alone and there is nothing to suggest that the pace of change will slacken in the years ahead.

Is corporate travel still important for business success?

All the indications are that, despite challenging economic and geopolitical circumstances over the past few years, demand for corporate travel is showing signs of strong recovery for 2023.

While earlier predictions of a $1.4 trillion annual spend have now been revised, the Global Business Travel Association (GBTA) has forecast a $1.2 trillion spend for business travel in 2023.

The simple reason for that is that business travel remains absolutely essential because of its key role in reconnecting organisations both internally but, equally importantly, with external stakeholders in the commercial marketplace.

The enormous increase in remote working since the pandemic has been well documented and while many companies have now adopted a hybrid model which combines office and home working, it’s clear that, for an increasing number of organisations, working remotely is an option which many people want or expect and one which is here to stay.

However, making personal connections is invaluable in the commercial world and there is no replacement for a face-to-face meeting, whether the purpose of that is employee motivation and bonding, securing new business, closing a deals or assessing a potential new suppliers or customers.

In short, the business travel market and effective corporate travel management remains integral to economic growth.

Can we expect further growth for business travel over the next 12-months?

A recent poll conducted by the GBTA states three in four travel managers expect their company will make more business trips in 2023 and is expected to increase significantly compared 2022.

However, as we’ve already seen, forecasting likely trends in the corporate travel market for the year ahead, while always an inexact science, is even more challenging at present due to global economic and political circumstances.

That said, there are a number of areas in which clear trends are emerging.

Sustainability

The demand for more sustainable ways to travel is expected to accelerate in 2023, meaning businesses will be even more keen to demonstrate their commitment to sustainability . Travel managers will need to prioritise environmentally-friendly options when arranging flights & accommodation.

Businesses will need to be more conscious about investing in better & greener choices when travelling for business. This could involve choosing a more sustainable mode of transport, selecting accommodation that has a sustainability policy in place or it could even be as simple as having digitalised travel documents to cut down on the amount of paper being used.

In addition, many companies will have the option to participate in a carbon offsetting scheme, in order to compensate for their own carbon emissions produced via business travel activity. This can be done through either existing suppliers or separate green projects.

All in all, the world of business travel will have an increasing focus on sustainability as the year progresses.

Are Travel budgets Making their way back to 2019 levels?

Despite the challenges of recent times, business travel bookings and spending continue to make their way back to pre-covid levels. According to the GBTA, travel buyers have estimated that their companies' domestic business travel bookings have returned to 68% of their 2019 spend levels, which is up from 63% in Q4 2022.

However, companies that do not have an extensive travel budget, will have to come up with solutions to cut down on spend when employee travel is absolutely necessary for the business. Many businesses may look to send their employees on longer haul trips, with multiple layovers to make their trip more efficient, while reducing the number of travel bookings needed.

Ideally, your travel manager should be looking to assist you in formulating a clear, effective travel policy which provides your people with all the information and guidelines they need on expected costs.

Changes to business travel policies

Many businesses have adopted a hybrid-working approach since the pandemic, which has forced them to think about what their employees can, and can't claim back as expenses.

Savings made by businesses from employees working at home will require policies to be updated or renewed to include a new employee allowance.

Travel policies which may have been appropriate pre-pandemic may no longer be fit for purpose and, as corporate travel remains a key economic driver, it will be important for the business community and their corporate travel management partners to ensure that policies are updated accordingly.

Technology will become even more important for business travel

With online booking such an essential element of so much corporate travel, there are also signs that self-booking is increasing in popularity, particularly for younger business travelers who may be more comfortable with its use during the booking process.

In addition, your people don't want to be thinking about collating multiple receipts needed for an expense report while travelling on business. They want to be focusing on the reason for the business trip.

Technology can play a huge part in streamlining the business travel process; whether it's a more efficient booking process, digital payment methods or managing your travel documents.

'Bleisure' travel: can employees mix business with leisure activities?

Along with a 44% increase in business travel airfares, which is expected to rise further in 2023, we can also expect to see a rise in bleisure travel with increasing numbers of business travellers using their time away from the office to accommodate leisure activities within their itineraries.

Remote working has been the driver of this. With employees able to work from virtually anywhere that has a good WiFi connection and charging points, travel can be extended by a few days or even weeks, depending on how far they have to travel.

Traveller safety

For the best travel managers, safety will remain one of the top priorities in corporate travel.

The pandemic has emphasised the importance of employee security when travelling for business and other recent external world events have only underlined this further.

Marine & Offshore Travel are the core of Clyde's business

Alongside Clyde’s wider corporate travel management activities, our core business is our specialist support for the marine and offshore industries.

We have a 30-year track record of helping to move crews safely around the globe for some of the world's largest ship owners. As part of the Northern Marine and the wider Stena Group, Clyde live and breathe the Marine sector.

Our performance over the pandemic is testament to our expertise in this area, with one of our customers quoting that the industry average was 25% behind in crew changes in 2020; however, they were only 8% behind because they had Clyde as the trusted travel management company.

We have an unrivalled understanding of the marine sector’s complexities and challenges. Our proprietary Consort technology, which helps businesses improve communication to speed up the booking process, makes us the ideal partner to get your people where they need to be safely, efficiently and cost-effectively.

With over 100 global marine airline contracts and wholly owned operations in the UK, US, Sweden, Norway, Denmark, Netherlands and an offshore service centre in India, we have the content, knowledge and infrastructure to support some of the largest ship owners and managers in the world.

We also work closely partner agencies across the globe to ensure we deliver the best marine and offshore fares, with the flexibility required for your company and crew.

Our specialist expertise enables us to safely mobilise thousands of seafarers across the globe each year from across Europe and other key territories including the Philippines, Russia, India and Ukraine.

Our expert teams have an average length of service of nine years, can deploy unique products and technology specifically tailored to mobilising crew and access airfare savings through our farewatch and unused tickets tracking, providing our customers with tangible cost and efficiency savings.

Want to know more about what to expect for business travel in 2023? Get in touch with our corporate travel experts today.

Recent News

Get in touch with us

New enquiries can be made using the contact form opposite.

Existing customers are reminded to contact their designated travel team using the email or telephone numbers provided to their organisation, to ensure their enquiry is dealt with by the correct team.

An official website of the United States Government

- Kreyòl ayisyen

- Search Toggle search Search Include Historical Content - Any - No Include Historical Content - Any - No Search

- Menu Toggle menu

- INFORMATION FOR…

- Individuals

- Business & Self Employed

- Charities and Nonprofits

- International Taxpayers

- Federal State and Local Governments

- Indian Tribal Governments

- Tax Exempt Bonds

- FILING FOR INDIVIDUALS

- How to File

- When to File

- Where to File

- Update Your Information

- Get Your Tax Record

- Apply for an Employer ID Number (EIN)

- Check Your Amended Return Status

- Get an Identity Protection PIN (IP PIN)

- File Your Taxes for Free

- Bank Account (Direct Pay)

- Payment Plan (Installment Agreement)

- Electronic Federal Tax Payment System (EFTPS)

- Your Online Account

- Tax Withholding Estimator

- Estimated Taxes

- Where's My Refund

- What to Expect

- Direct Deposit

- Reduced Refunds

- Amend Return

Credits & Deductions

- INFORMATION FOR...

- Businesses & Self-Employed

- Earned Income Credit (EITC)

- Child Tax Credit

- Clean Energy and Vehicle Credits

- Standard Deduction

- Retirement Plans

Forms & Instructions

- POPULAR FORMS & INSTRUCTIONS

- Form 1040 Instructions

- Form 4506-T

- POPULAR FOR TAX PROS

- Form 1040-X

- Circular 230

Future Developments

Who should use this publication.

Users of employer-provided vehicles.

Who doesn’t need to use this publication.

Volunteers.

Comments and suggestions.

Getting answers to your tax questions.

Getting tax forms, instructions, and publications.

Ordering tax forms, instructions, and publications.

- Useful Items - You may want to see:

Travel expenses defined.

Members of the Armed Forces.

Main place of business or work.

No main place of business or work.

Factors used to determine tax home.

Tax Home Different From Family Home

Temporary assignment vs. indefinite assignment.

Exception for federal crime investigations or prosecutions.

Determining temporary or indefinite.

Going home on days off.

Probationary work period.

Separating costs.

Travel expenses for another individual.

Business associate.

Bona fide business purpose.

Lavish or extravagant.

50% limit on meals.

Actual Cost

Incidental expenses.

Incidental-expenses-only method.

50% limit may apply.

Who can use the standard meal allowance.

Use of the standard meal allowance for other travel.

Amount of standard meal allowance.

Federal government's fiscal year.

Standard meal allowance for areas outside the continental United States.

Special rate for transportation workers.

Travel for days you depart and return.

Trip Primarily for Business

Trip primarily for personal reasons.

Public transportation.

Private car.

Travel entirely for business.

Travel considered entirely for business.

Exception 1—No substantial control.

Exception 2—Outside United States no more than a week.

Exception 3—Less than 25% of time on personal activities.

Exception 4—Vacation not a major consideration.

Travel allocation rules.

Counting business days.

Transportation day.

Presence required.

Day spent on business.

Certain weekends and holidays.

Nonbusiness activity on the way to or from your business destination.

Nonbusiness activity at, near, or beyond business destination.

Other methods.

Travel Primarily for Personal Reasons

Daily limit on luxury water travel.

Meals and entertainment.

Not separately stated.

Convention agenda.

North American area.

Reasonableness test.

Cruise Ships

Deduction may depend on your type of business.

Exceptions to the Rules

Entertainment events.

Entertainment facilities.

Club dues and membership fees.

Gift or entertainment.

Other rules for meals and entertainment expenses.

Costs to include or exclude.

Application of 50% limit.

When to apply the 50% limit.

Taking turns paying for meals.

1—Expenses treated as compensation.

2—Employee's reimbursed expenses.

3—Self-employed reimbursed expenses.

4—Recreational expenses for employees.

5—Advertising expenses.

6—Sale of meals.

Individuals subject to “hours of service” limits.

Incidental costs.

Exceptions.

- Illustration of transportation expenses.

Temporary work location.

No regular place of work.

Two places of work.

Armed Forces reservists.

Commuting expenses.

Parking fees.

Advertising display on car.

Hauling tools or instruments.

Union members' trips from a union hall.

Office in the home.

Examples of deductible transportation.

Choosing the standard mileage rate.

Standard mileage rate not allowed.

Five or more cars.

Personal property taxes.

Parking fees and tolls.

Sale, trade-in, or other disposition.

Business and personal use.

Employer-provided vehicle.

Interest on car loans.

Taxes paid on your car.

Sales taxes.

Fines and collateral.

Casualty and theft losses.

Depreciation and section 179 deductions.

Car defined.

Qualified nonpersonal use vehicles.

More information.

More than 50% business use requirement.

Limit on the amount of the section 179 deduction.

Limit for sport utility and certain other vehicles.

Limit on total section 179 deduction, special depreciation allowance, and depreciation deduction.

Cost of car.

Basis of car for depreciation.

When to elect.

How to elect.

Revoking an election.

Recapture of section 179 deduction.

Dispositions.

Combined depreciation.

Qualified car.

Election not to claim the special depreciation allowance.

Placed in service.

Car placed in service and disposed of in the same year.

Methods of depreciation.

More-than-50%-use test.

Qualified business use.

Use of your car by another person.

Business use changes.

Use for more than one purpose.

Change from personal to business use.

Unadjusted basis.

Improvements.

Car trade-in.

Effect of trade-in on basis.

Traded car used only for business.

Traded car used partly in business.

Modified Accelerated Cost Recovery System (MACRS).

Recovery period.

Depreciation methods.

MACRS depreciation chart.

Depreciation in future years.

Disposition of car during recovery period.

How to use the 2023 chart.

Trucks and vans.

Car used less than full year.

Reduction for personal use.

Section 179 deduction.

Deductions in years after the recovery period.

Unrecovered basis.

The recovery period.

How to treat unrecovered basis.

- Table 4-1. 2023 MACRS Depreciation Chart (Use To Figure Depreciation for 2023)

Qualified business use 50% or less in year placed in service.

Qualified business use 50% or less in a later year.

Excess depreciation.

Deductible payments.

Fair market value.

Figuring the inclusion amount.

Leased car changed from business to personal use.

Leased car changed from personal to business use.

Reporting inclusion amounts.

Casualty or theft.

Depreciation adjustment when you used the standard mileage rate.

Depreciation deduction for the year of disposition.

Documentary evidence.

Adequate evidence.

Canceled check.

Duplicate information.

Timely kept records.

Proving business purpose.

Confidential information.

Exceptional circumstances.

Destroyed records.

Separating expenses.

Combining items.

Car expenses.

Gift expenses.

Allocating total cost.

If your return is examined.

Reimbursed for expenses.

Examples of Records

Self-employed.

Both self-employed and an employee.

Statutory employees.

Reimbursement for personal expenses.

Income-producing property.

Value reported on Form W-2.

Full value included in your income.

Less than full value included in your income.

No reimbursement.

Reimbursement, allowance, or advance.

Reasonable period of time.

Employee meets accountable plan rules.

Accountable plan rules not met.

Failure to return excess reimbursements.

Reimbursement of nondeductible expenses.

Adequate Accounting

Related to employer.

The federal rate.

Regular federal per diem rate.

The standard meal allowance.

High-low rate.

Prorating the standard meal allowance on partial days of travel.

The standard mileage rate.

Fixed and variable rate (FAVR).

Reporting your expenses with a per diem or car allowance.

Allowance less than or equal to the federal rate.

Allowance more than the federal rate.

Travel advance.

Unproven amounts.

Per diem allowance more than federal rate.

Reporting your expenses under a nonaccountable plan.

Adequate accounting.

How to report.

Contractor adequately accounts.

Contractor doesn’t adequately account.

High-low method.

Regular federal per diem rate method.

Federal per diem rate method.

Information on use of cars.

Standard mileage rate.

Actual expenses.

Car rentals.

Transportation expenses.

Employee business expenses other than nonentertainment meals.

Non-entertainment-related meal expenses.

“Hours of service” limits.

Reimbursements.

Allocating your reimbursement.

After you complete the form.

Limits on employee business expenses.

1. Limit on meals and entertainment.

2. Limit on total itemized deductions.

Member of a reserve component.

Officials Paid on a Fee Basis

Special rules for married persons.

Where to report.

Impairment-Related Work Expenses of Disabled Employees

Preparing and filing your tax return.

Free options for tax preparation.

Using online tools to help prepare your return.

Need someone to prepare your tax return?

Employers can register to use Business Services Online.

IRS social media.

Watching IRS videos.

Online tax information in other languages.

Free Over-the-Phone Interpreter (OPI) Service.

Accessibility Helpline available for taxpayers with disabilities.

Getting tax forms and publications.

Getting tax publications and instructions in eBook format.

Access your online account (individual taxpayers only).

Get a transcript of your return.

Tax Pro Account.

Using direct deposit.

Reporting and resolving your tax-related identity theft issues.

Ways to check on the status of your refund.

Making a tax payment.

What if I can’t pay now?

Filing an amended return.

Checking the status of your amended return.

Understanding an IRS notice or letter you’ve received.

Responding to an IRS notice or letter.

Contacting your local TAC.

What Is TAS?

How can you learn about your taxpayer rights, what can tas do for you, how can you reach tas, how else does tas help taxpayers, low income taxpayer clinics (litcs), appendix a-1. inclusion amounts for passenger automobiles first leased in 2018, appendix a-2. inclusion amounts for passenger automobiles first leased in 2019, appendix a-3. inclusion amounts for passenger automobiles first leased in 2020, appendix a-4. inclusion amounts for passenger automobiles first leased in 2021, appendix a-5. inclusion amounts for passenger automobiles first leased in 2022, appendix a-6. inclusion amounts for passenger automobiles first leased in 2023, publication 463 - additional material, publication 463 (2023), travel, gift, and car expenses.

For use in preparing 2023 Returns

Publication 463 - Introductory Material

For the latest information about developments related to Pub. 463, such as legislation enacted after it was published, go to IRS.gov/Pub463 .

Standard mileage rate. For 2023, the standard mileage rate for the cost of operating your car for business use is 65.5 cents ($0.655) per mile. Car expenses and use of the standard mileage rate are explained in chapter 4.

Depreciation limits on cars, trucks, and vans. The first-year limit on the depreciation deduction, special depreciation allowance, and section 179 deduction for vehicles acquired before September 28, 2017, and placed in service during 2023, is $12,200. The first-year limit on depreciation, special depreciation allowance, and section 179 deduction for vehicles acquired after September 27, 2017, and placed in service during 2023 increases to $20,200. If you elect not to claim a special depreciation allowance for a vehicle placed in service in 2023, the amount increases to $12,200. Depreciation limits are explained in chapter 4.

Section 179 deduction. The maximum amount you can elect to deduct for section 179 property (including cars, trucks, and vans) you placed in service in tax years beginning in 2023 is $1,160,000. This limit is reduced by the amount by which the cost of section 179 property placed in service during the tax year exceeds $2,890,000. Section 179 deduction is explained in chapter 4.Also, the maximum section 179 expense deduction for sport utility vehicles placed in service in tax years beginning in 2023 is $28,900.

Temporary deduction of 100% business meals. The 100% deduction on certain business meals expenses as amended under the Taxpayer Certainty and Disaster Tax Relief Act of 2020, and enacted by the Consolidated Appropriations Act, 2021, has expired. Generally, the cost of business meals remains deductible, subject to the 50% limitation. See 50% Limit in chapter 2 for more information.

Photographs of missing children. The IRS is a proud partner with the National Center for Missing & Exploited Children® (NCMEC) . Photographs of missing children selected by the Center may appear in this publication on pages that would otherwise be blank. You can help bring these children home by looking at the photographs and calling 800-THE-LOST (800-843-5678) if you recognize a child.

Per diem rates. Current and prior per diem rates may be found on the U.S. General Services Administration (GSA) website at GSA.gov/travel/plan-book/per-diem-rates .

Introduction

You may be able to deduct the ordinary and necessary business-related expenses you have for:

Non-entertainment-related meals,

Transportation.

This publication explains:

What expenses are deductible,

How to report them on your return,

What records you need to prove your expenses, and

How to treat any expense reimbursements you may receive.

You should read this publication if you are an employee or a sole proprietor who has business-related travel, non-entertainment-related meals, gift, or transportation expenses.

If an employer-provided vehicle was available for your use, you received a fringe benefit. Generally, your employer must include the value of the use or availability of the vehicle in your income. However, there are exceptions if the use of the vehicle qualifies as a working condition fringe benefit (such as the use of a qualified nonpersonal use vehicle).

A working condition fringe benefit is any property or service provided to you by your employer, the cost of which would be allowable as an employee business expense deduction if you had paid for it.

A qualified nonpersonal use vehicle is one that isn’t likely to be used more than minimally for personal purposes because of its design. See Qualified nonpersonal use vehicles under Actual Car Expenses in chapter 4.

For information on how to report your car expenses that your employer didn’t provide or reimburse you for (such as when you pay for gas and maintenance for a car your employer provides), see Vehicle Provided by Your Employer in chapter 6.