By Lisa Jackson

Play article

( mins)

( )

Best travel insurance in Canada

KieferPix / Shutterstock

You’ve packed your bags, mapped your itinerary, and set your “out of office” message – it’s vacation time! But what about travel insurance?

According to a 2019 study by the Travel Health Insurance Association of Canada, 13% of Canadians aren’t sure if they have travel insurance before they go on vacation. Of those who have bought insurance, 17% don’t know what their policy covers.

As a professional travel writer, I find this rather alarming. Canadian health insurance is not valid outside Canada, and your provincial or territorial health plan may not cover all the costs even if you’re travelling domestically. If you suffer an accident or get sick abroad, unexpected medical bills can bankrupt you. It’s why the Canadian government advises all travellers to buy travel insurance , and I never leave the country without it. Whether you’re taking a two-week trip or a gap year abroad, every one needs the best travel insurance in Canada, regardless of age, health status, destination, or length of vacation.

World Nomads: Best for thrill seekers

Designed for adrenaline lovers with wanderlust, World Nomads insures a long list of adventure sports, activities and volunteer/work experiences, as well as sporting equipment delay/loss/theft. You also get access to a 24/7 hotline that provides information that adventure travellers may need: weather reports and travel advisories, assistance locating the nearest trail, and finding a gear shop.

The standard policy covers emergency medical expenses up to $5 million, emergency dental, trip cancellation/interruption/delay, baggage delays/theft/damage, and more. The downside: you must be under 66 years of age to qualify.

CAA Travel Insurance: Best for families

A long-trusted Canadian institution, CAA travel Insurance offers flexible travel plans to suit every type of traveller and vacation, but their policies are particularly great for families. Their stand-alone emergency medical policy of up to $5 million in health coverage is extremely comprehensive, even including medical repatriation, emergency dental, and reimbursements for pet care and kenneling.

The Vacation Package Plan provides full cancellation/interruption insurance – ideal for prepaid, all-inclusive vacation packages – as well as family transportation and escort of children during emergencies. Anyone can buy CAA travel insurance, but members get a 10% discount.

CAA’s emergency medical plans also now include coverage for COVID-19-related illnesses for vaccinated customers. Coverage is up to $2.5 million if partially vaccinated and up to $5 million if fully vaccinated.

Blue Cross: Best for seniors and retirees

Blue Cross has been around for more than 70 years, and 1 in 4 Canadians utilize its travel insurance. Blue Cross’s emergency medical covers up to $5 million. It has special “snowbird” travel insurance packages designed for Canadians who head to warmer climates each year, making Blue Cross ideal for retirees.

Part of the package is the recently launched Serenity Service. This free perk provides a range of benefits if your flight is delayed, including access to an airport lounge or even a hotel room (depending on the length of the delay). Pre-existing conditions are generally not covered.

Travel CUTS Bon Voyage Insurance: Best for budget travellers

Starting at only $1.36 a day, Travel CUTS Bon Voyage Insurance offers very affordable travel insurance packages, and it’s personally been my “go-to” travel policy for years. Yes, it’s geared toward students (e.g., you can swap your travel dates at no charge due to an exam schedule conflict), but anyone between 15 and 50 years of age can purchase a policy.

The standard package includes hospital and medical up to $1 million, dental care, air ambulance evacuation, flight accident, accidental death or dismemberment, and trip interruption/cancellation insurance. Adventure and extreme sports are also covered.

Manulife CoverMe: Best for Canadians with pre-existing medical conditions

Manulife CoverMe offers highly comprehensive Canadian travel insurance packages for those travelling as a family, a visitor to Canada, or a student. You also get access to the TravelAid mobile app, which provides directions to the nearest medical facility and local emergency telephone numbers.

However, the stand-out feature is arguably TravelEase – a special policy designed to cover fully disclosed medical conditions. For travellers with pre-existing conditions, it insures a bunch of expenses for health services and transportation. It provides up to $10 million in emergency medical benefits – a unicorn in the travel insurance world.

Medipac Travel Insurance: Best for emergency medical assistance

Medipac is one of the only travel insurance companies out there that is staffed by their own team of trained medical professionals, via their Medipac Assistance hotline. Medipac’s medical professionals are your first point of contact in an emergency medical situation. This service is also helpful for dealing with foreign medical systems and helping to prevent unnecessary expenses when dealing with a large deductible.

Medipac offers several competitive features for their travel insurance plans, including no age limits, a claim-free discount, and a 90-day stability period for most pre-existing conditions. If your pre-existing medical condition isn’t covered by a standard Medipac insurance plan, Medipac also offers personalized, underwritten insurance policies to help you meet your needs.

Medipac is offering a 5% Vaccine Discount to clients who have received a minimum of one dose of a COVID-19 vaccine, as well as the new MedipacMAX option. This COVID insurance option provides maximum coverage of up to $5 million USD for COVID-19, in addition to its other benefits.

Allianz Travel Insurance: Best for frequent travellers

Touted as a world leader in the Canadian travel insurance and assistance industry, Allianz Travel Insurance is a major provider of travel insurance, corporate assistance, and concierge services. It seeks to help its customers find solutions to various travel-related problems. Allianz Travel has partnered with many reputable companies, including travel agencies, airlines, resorts, websites, event ticket brokers, corporations, universities, and credit card companies.

Allianz Travel Insurance is a great choice for anyone looking for travel insurance. Its single-trip plans are perfect for those leaving home and visiting another destination (or destinations) before going back home. Its parent company, Allianz Global Assistance, has five plans to choose from, all offering different levels of protection and coverage.

Allianz Travel Insurance’s annual/multi-trip plans are perfect for both personal and professional travelers who take multiple trips in a year. It offers four distinct options to choose from.

Will my provincial insurance be valid overseas?

No! If you get sick or injured overseas, the Canadian government will not cough up a dime to cover your medical costs. Here are the sobering facts:

- Canadian public health insurance is not valid outside of Canada.

- Foreign hospitals can be extremely expensive and may demand payment before treating you.

- The Canadian government will not pay a Canadian’s medical bills for an illness or accident suffered abroad. You’re on the hook for footing the bill!

Will my provincial insurance work in another province/territory?

Flash your valid provincial health card in another part of Canada, and you’ll likely be covered for some of the same services insured by your home provincial plan. This is because the provinces and territories (except Quebec) signed an agreement whereby the host province foots the bill for any medically necessary health care services and gets reimbursed by the home province later.

However, that doesn’t mean you’re completely out of the woods. Depending on your destination, a slew of other services may not be covered, such as an ambulance, hospital transfer, prescription drugs, transportation back to your home province, and procedures not currently approved by your home plan.

Plus, since Quebec wasn’t a signatory to the interprovincial billing agreement, you’ll likely be charged for any medical bills incurred there. For this reason, it’s recommended that you buy extra travel insurance (or verify your credit card’s travel insurance coverage ) to cover any uninsured health care services that may crop up during your trip.

What does the best travel insurance in Canada cover?

Every travel insurance policy is different and what’s covered depends on how much you’re willing to pay for coverage. Typical medical services that you can expect to be covered include:

- Emergency hospital and medical costs

- Ambulance and air ambulance costs

- Outpatient services

- Physician and laboratory costs

- Prescription drugs

- Direct payment to the hospitals and doctors caring for you

- Assistance with bringing a family member to your bedside

- Air ambulance or commercial repatriation home

- Return of your vehicle if you are ill and have to come home

Additional benefits may include:

- Trip cancellation for non-refundable monetary losses

- Trip interruption

- Baggage loss, rental car damage, out-of-pocket expenses

- Accidental death and dismemberment

How much coverage do I need?

Securing a policy with a minimum of $1M maximum payable is a safe bet. But don’t just look at the numbers when choosing a policy – read the fine print. Every insurer has a list of situations in which coverage is not provided, otherwise known as “exclusions.” Check whether your provider includes coverage or has provisions for the following:

- Pre-existing medical conditions: According to the International Association for Medical Assistance to Travelers, a pre-existing condition is “something that happened (or started to happen) before you were insured.” Some policies may cover claims relating to pre-existing conditions that are “stable and controlled,” but read the definitions carefully. If you don’t declare a condition, the entire policy could be invalidated!

- Medical evacuation: Ensure the policy covers medical evacuation to the nearest hospital and/or to Canada and the costs of a medical escort to accompany you to your final destination.

- Repatriation in case of death: On the grim side, ensure that your plan covers the preparation and return of your remains to Canada.

- Adventurous Activities: If you plan on engaging in “high-risk” activities on your trip, you may need to shell out extra dough for a more comprehensive plan. Many policies don’t cover “risky” activities, such as skiing or snowboarding “out of bounds,” skydiving, scuba diving, white-water rafting, mountaineering, or participation in any rodeo activity. To cover your bases, ask questions and get specifics before purchasing a policy.

You may have to pay more to have these things included, but a few extra bucks may be worth it for peace of mind.

Should I buy “a la carte” travel insurance or get a travel credit card with free insurance?

A credit card with travel insurance is always a good thing to carry in your wallet. The best travel credit cards in Canada usually cover everything from emergency medical costs to trip cancellation/interruption to flight delay to rental car insurance, which could save you a wad of cash.

The Scotiabank Gold American Express ® Card has saved my butt a few times, and I’ve filed several travel-related claims through my card. I cancelled my trip to Portugal a few years ago due to a death in the family, and I got a full refund on my hotel deposit and flights for myself, my husband, and my baby. It totally justified the $120 annual fee.

That being said, don’t rely on your credit card to take care of all your travel insurance needs. It usually includes a basic policy, meaning it offers low (or no!) travel medical insurance as part of the package. Like any travel insurance company policy, you’ve really got to read the fine print and understand the conditions of your policy to avoid sticky situations.

For instance, the Scotiabank Gold American Express ® Card requires a cardholder to have charged at least 75% of trip expenses to make a trip cancellation/interruption insurance claim. So if you book an all-inclusive vacation for $5,000 and then cancel due to illness, at least $3,750 must have been charged onto your AMEX to qualify for a claim. If you didn’t do that, you’re out of luck.

Can I still purchase insurance if i’ve already started my vacation?

The short answer: most insurance providers won’t cover you after your departure date. However, a handful of insurers (such as World Nomads) will allow you to purchase a policy while already overseas. Just know that it can come with sky-high costs and/or conditions: World Nomads has a 48-hour waiting period before coverage kicks in. The bottom line? It’s always best to buy travel insurance before leaving the country.

Can I get travel insurance for part of a trip?

Some plans offer insurance coverage options that will allow you to customize your coverage, but you’ll have to research to find one that works for your unique circumstances. Alternatively, you could take out an insurance policy for each destination and/or segment of your trip.

For instance, you could get a World Nomads policy for the two weeks you’re scuba diving in Australia, followed by a basic Travel CUTS Bon Voyage insurance to cover a month-long trip to Europe. However, when you buy Canadian travel insurance, you must select a trip start and end date – meaning you must know the exact dates for travelling to those places.

Should I carry a printout of my policy with me at all times?

I recommend carrying the travel insurance card in your wallet and locking it up in the hotel safe with other important travel documents like my passport. But don’t rely totally on paper: Wallets get lost or stolen, luggage can be delayed or M.I.A., and papers are easy to misplace when you’re on the road. My advice is to send a copy of the policy to your email and save it on your iCloud or another storage system that can be accessed anywhere, anytime.

Recommended reads

- What’s the Added Value of a Credit Card with Travel Insurance?

- The Best Travel Rewards Programs in Canada

- Aeroplan vs. AIR MILES vs. Avion

About our author

Lisa Jackson is a freelance personal finance and travel journalist, editor, and blogger who contributes to various online and print media outlets in Canada and abroad, including The Globe & Mail, Toronto Star, Islands Magazine, Fodors, BRIDES, Huffington Post Canada, CAA Magazine, The Food Network, West Jet Magazine, NUVO Magazine, and many others. When she's not writing from her home office, she's busy globe-trotting to new destinations in search of her next story.

Latest Articles

Toronto airports authority announces 'decade-long investment' in Pearson Airport

Stormy weather, 'sluggish' spending push MTY Food Group's Q1 profits, revenue down

Corus ceo hopeful tv advertisers will return as company posts $9.8m q2 loss.

Home prices expected to climb 4.9% in 2024 as sales rise last month: CREA

Asking rent prices in March up 8.8% from year ago, but down from February: Urbanation

S&p/tsx composite down, u.s. stock markets also lower.

The content provided on Money.ca is information to help users become financially literate. It is neither tax nor legal advice, is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Tax, investment and all other decisions should be made, as appropriate, only with guidance from a qualified professional. We make no representation or warranty of any kind, either express or implied, with respect to the data provided, the timeliness thereof, the results to be obtained by the use thereof or any other matter.

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

11 Best Travel Insurance Companies in April 2024

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

If the past few years have shown us anything, it’s that travelers need to be prepared for the unexpected — from a pandemic to flight troubles to the crowded airport terminals so many of us have encountered.

Whether you’re looking for an international travel insurance plan, emergency medical care or a policy that includes extreme sports, these are the best travel insurance providers to get you covered.

How we found the best travel insurance

We looked at quotes from various companies for a 10-day trip to Mexico in September 2024. The traveler was a 55-year-old woman from Florida who spent $3,000 total on the trip, including airfare.

On average, the price of each company’s most basic coverage plan was $126.53. The costs displayed below do not include optional add-ons, such as Cancel For Any Reason coverage or pre-existing medical condition coverage.

Read our full analysis about the average cost of travel insurance so you can budget better for your next trip.

However, depending on the plan, you may be able to customize at an added cost.

As we continue to evaluate more travel insurance companies and receive fresh market data, this collection of best travel insurance companies is likely to change. See our full methodology for more details.

Best insurance companies

Types of travel insurance

What does travel insurance cover, what’s not covered, how much does it cost, do i need travel insurance, how to choose the best travel insurance policy, what are the top travel destinations in 2024, more resources for travel insurance shoppers, top credit cards with travel insurance, methodology, best travel insurance overall: berkshire hathaway travel protection.

Berkshire Hathaway Travel Protection

- ExactCare Value (basic) plan is among the least expensive we surveyed.

- Speciality plans available for road trips, luxury travel, adventure activities, flights and cruises.

- Company may reimburse claimants faster than average, including possible same-day compensation.

- Multiple "Trip Delay" coverage types might make claims confusing.

- Cheapest plan only includes fixed amounts for its coverage.

Under the direction of chair and CEO Warren Buffett, Berkshire Hathaway Travel Protection has been around since 2014. Its plans provide numerous opportunities for travelers to customize coverage to their needs.

At $135 for our sample trip, the ExactCare Value (basic) plan from Berkshire Hathaway Travel Protection offers protection roughly $10 above the average price.

Want something cheaper? Air travelers looking for inexpensive, less comprehensive protections might opt for a basic AirCare plan that includes fixed amounts for its coverage .

Read our full review of Berkshire Hathaway .

What else makes Berkshire Hathaway Travel Protection great:

Pre-existing medical condition exclusion waivers available at no extra cost.

Plans available for travelers going on a cruise, participating in extreme sports or taking a luxury trip.

ExactCare Value (basic) plan was among the least expensive we surveyed.

Best for emergency medical coverage: Allianz Global Assistance

Annual or single-trip policies are available.

- Multiple types of insurance available.

- All plans include access to a 24/7 assistance hotline.

- More expensive than average.

- CFAR upgrades are not available.

- Rental car protection is only available by adding the One Trip Rental Car protector to your plan or by purchasing a standalone rental car plan.

Allianz Global Assistance is a reputable travel insurance company offering plans for over 25 years. Customers can choose from a variety of single and annual policies to fit their needs. On top of comprehensive coverage, some travelers might opt for the more affordable OneTrip Cancellation Plus, which is geared toward domestic travelers looking for trip protections but don’t need post-departure benefits like emergency medical or baggage lost.

For our test trip, Allianz Global Assistance’s basic coverage cost $149, about $22 above average.

What else makes Allianz Global Assistance great:

Annual and single-trip plans.

Plans are available for international and domestic trips.

Stand-alone and add-on rental car damage product available.

Read our full review of Allianz Global Assistance .

Best for travelers with pre-existing medical conditions: Travel Guard by AIG

Travel Guard by AIG

- Offers last-minute coverage.

- Pre-Existing Medical Conditions Exclusion Waiver available at all plan levels.

- Plan available for business travelers.

- Cancel For Any reason coverage only available for higher-level plans, and only reimburses up to 50% of the trip cost.

- Trip interruption coverage doesn't apply to trips paid for with points and miles.

Travel Guard by AIG offers a variety of plans and coverages to fit travelers’ needs. On top of more standard trip protections like trip cancellation, interruption, baggage and medical coverage, the Cancel For Any Reason upgrade is available on certain Travel Guard plans, which allows you to cancel a trip for any reason and get 50% of your nonrefundable deposit back as long as the trip is canceled at least two days before the scheduled departure date.

At $107 for our sample trip, the Essential plan was below average, saving roughly $20.

What else makes Travel Guard by AIG great:

Three comprehensive plans and a Pack N' Go plan for last-minute travelers who don't need cancellation benefits.

Flight protection, car rental, and medical evacuation coverage, as well as annual plans available.

Pre-existing medical conditions exclusion waiver available on all plan levels, as long as it's purchased within 15 days.

Read our full review of Travel Guard by AIG .

Best for those who pack expensive equipment: Travel Insured International

Travel Insured International

- Higher-level plan include optional add-ons for event tickets and for electronic equipment

- Rental car protection add-on for just $8 per day, even on lower-level plan.

- Many of the customizations are only available on the higher-tier plan.

- Coverage cost comes in above average in our latest analysis.

Travel Insured International offers several customization options. For instance, those going to see a show may want to add on event ticket registration fee protection. Traveling with expensive gear?Consider adding on coverage for electronic equipment for up to $2,000 in coverage.

Be sure to check which policies are available in your state. You will need to input your destination, residence, trip dates and the number of travelers to get a quote and see coverages.

What else makes Travel Insured International great:

Comprehensive plans include medical expense reimbursement accidents, sickness, evacuation and pre-existing conditions, depending on the plan.

Flight plans include coverage for missed and canceled flights and lost or stolen baggage.

Read our full review of Travel Insured International .

Best for adventurous travelers: World Nomads

World Nomads

- Travelers can extend coverage mid-trip.

- The standard plan covers up to $300,000 in emergency evacuation costs.

- Plans automatically cover 200+ adventurous activities.

- No Cancel For Any Reason upgrades are available.

- No pre-existing medical condition waivers are available.

Many travel insurance plans contain exclusions for adventure sports activities. If you plan to ski, bungee jump, windsurf or parasail, this might be a plan to consider.

Note that the Standard plan ($72 for our sample trip), while the most affordable, provides less coverage than other plans. But it can be a good choice for travelers who are satisfied with trip cancellation and interruption coverage of $2,500 or less, do not need rental car damage protection, find the limits to be sufficient and do not need coverage for certain more adventurous activities.

What else makes World Nomads great:

Comprehensive international travel insurance plans.

Coverage available for adventure activities, such as trekking, mountain biking and scuba diving.

Read our full review of World Nomads .

Best for medical coverage: Travelex Insurance Services

Travelex Insurance Services

- Top-tier plan doesn’t break the bank and provides more customization opportunities.

- Offers a plan specifically for domestic travel.

- Sells a post-departure medical coverage plan.

- Fewer customization opportunities on the Basic plan.

- Though perhaps a plus for domestic travelers, keep in mind the Travel America plan only covers domestic trips.

For starters, basic coverage from Travelex Insurance Services came in at $125, almost exactly average for our sample trip.

Travelex’s plans focus heavily on providing protections that are personalized to your travel style and trip type.

While the company does offer comprehensive plans that include medical benefits, you can also choose between cheaper plans that don’t provide cancellation coverage but do offer protections during your travels.

Read our full review of Travelex Insurance Services .

What else makes Travelex Insurance Services great:

Three comprehensive plans available, two of which cover international trips.

Offers a post-departure plan geared exclusively toward disruptions after you leave home.

Two flight insurance plans available.

Best if you have travel credit card coverage: Seven Corners

Seven Corners

- Annual, medical-only and backpacker plans are available.

- Cancel For Any Reason upgrade is available for the cheapest plan.

- Cheapest plan also features a much less costly Interruption for Any Reason add-on.

- Offers only one annual policy option.

Each Seven Corners plan offers several optional add-ons. Among the more unique is a Trip Interruption for Any Reason, which allows you to interrupt a trip 48 hours after the scheduled departure date (for any reason) and receive a refund of up to 75% of your unused nonrefundable deposits.

The basic coverage plan for our trip to Mexico costs $124 — right around the average.

What else makes Seven Corners great:

Comprehensive plans for U.S. residents and foreigners, including travelers visiting the U.S.

Cheap add-ons for rental car damage, sporting equipment rental or trip interruption for any reason.

Read our full review of Seven Corners .

Best for long-term travelers: IMG

- Coverage available for adventure travelers.

- Special medical insurance for ship captains and crew members, international students and missionaries.

- Claim approval can be lengthy.

While some travel insurance companies offer just a handful of plans, with IMG, you’ll really have your pick. Though this requires a bit more research, it allows you to search for coverage that fits your travel needs.

However, travelers will want to be aware that IMG’s iTravelInsured Travel Lite is expensive. Coming in at $149.85, it’s the costliest plan on our list.

Read our full review of IMG .

What else makes IMG great:

More affordable than average.

Many plans to choose from to fit your needs.

Best for travelers with unpredictable work demands: Tin Leg

- In addition Cancel For Any Reason, some plans offer cancel for work reason coverage.

- Adventure sports-specific coverage is available.

- Plans have overlap that can be hard to distinguish.

- Only one plan includes Rental Car Damage coverage available as an add-on.

Tin Leg’s Basic plan came in at $134 for our sample trip, adding about $8 onto the average basic policy cost. Note that you’ll pay a lot more if you shop for the most comprehensive coverage, and there are eight plans to choose from for trips abroad.

The multitude of plans can help you find coverage that fits your needs, but with so many to choose from, deciding can be daunting.

The only real way to figure out your ideal plan is to compare them all, look at the plan details and decide which features and coverage suit you and your travel style best.

Read our full Tin Leg review .

Best for booking travel with points and miles: TravelSafe

- Covers up to $300 redepositing points and miles on eligible canceled award flights.

- Optional add-on protection for business equipment or sports rentals.

- Multi-trip or year-long plans aren’t available.

Selecting your travel insurance plan with TravelSafe is a fairly straightforward process. The company’s website also makes it easy to visualize how optional add-on elements influence the total cost, displaying the final price as soon as you click the coverage.

However, at $136, the Basic plan was among the more expensive for our trip to Mexico.

What else makes TravelSafe great:

Rental car damage coverage add-on is available on both plans.

Cancel For Any Reason coverage available on the TravelSafe Classic plan.

Read our full TravelSafe review .

Best for group travel insurance: HTH Insurance

HTH Travel Insurance

- Covers travelers up to 95 years old.

- Includes direct pay option so members can avoid having to pay up front for services.

- A 24-hour delay is required for baggage delay coverage on the TripProtector Economy plan.

- No waivers for pre-existing conditions on the lower-level plan.

HTH offers single-trip and multitrip medical insurance coverage as well as trip protection plans.

At around $125, the Trip Protector Economy policy is at the average mark for plans we reviewed.

You can choose to insure group trips for educators, crew, religious missionaries and corporate travelers.

What else makes HTH Insurance great:

Medical-only coverage and trip protection coverage.

Lots of options for group travelers.

Read our full review of HTH Insurance .

As you shop for travel insurance, you’ll find many of the same coverage categories across numerous plans.

Trip cancellation

This covers the prepaid costs you make for your trip in cases when you need to cancel for a covered reason. This coverage helps you recoup upfront costs paid for flights and nonrefundable hotel reservations.

Trip interruption

Trip interruption benefits generally involve disruptions after you depart. It helps reimburse costs incurred for flight delays, cancellations and plenty of other covered disruptions you might encounter during your travels.

This coverage can cover the costs for you to return home or reimburse unexpected expenses like an extra hotel stay, meals and ground transportation.

Trip delay coverage helps cover unexpected costs when your trip is delayed. This is another coverage that helps offset the costs of flight trouble or other travel disruptions.

Note that many policies have a total amount a traveler can claim, with caps on per diem benefits, too.

Cancel For Any Reason

Cancel For Any Reason coverage allows you to recoup some of the upfront costs you paid for a trip even if you’re canceling for a reason not otherwise covered by your standard travel insurance policy.

Typically, adding this protection to your plan costs extra.

Baggage delay

This coverage helps cover the costs of essential items you might need when your luggage is delayed. Think toiletries, clothing and other immediate items you might need if your luggage didn’t make it on your flight.

Many travel insurance plans with baggage delay protection will specify how long (six, 12, 24 hours, etc.) your luggage must be delayed before you can make a claim.

Lost baggage

Used for travelers whose luggage is lost or stolen, this helps recoup the lost value of the items in your bag.

You’ll want to make sure you closely follow the correct procedures for your plan. Many plans include a maximum total amount you can claim under this coverage and a per-item cap.

Travel medical insurance

This covers out-of-pocket medical costs when travelers run into an emergency.

Because many travelers’ health insurance plans don’t cover medical care overseas, travel medical insurance can help offset out-of-pocket health care costs.

In addition to emergency medical coverage, many plans have medical evacuation or repatriation coverage for costs incurred when you must be taken to a hospital or return to your home country because of a medical situation.

Most travel insurance plans cover many trip protections that can help you be prepared for unexpected travel disruptions and expenses.

These coverages are generally aimed at protecting the money you put into your trip, expenses you incur because of travel trouble and costs incurred if you have a medical emergency overseas.

On top of core coverages like trip cancellation and interruption and travel medical coverage, some plans offer add-on options like waivers for pre-existing conditions, rental car collision damage waivers or adventure sports riders. These usually cost extra or must be added within a specified timeframe.

Typical travel insurance policies offer coverage for many unforeseen events, but as you research to select a plan, consider your needs. Though every plan differs, there are some commonly excluded coverages.

For instance, you typically can’t get coverage for a named storm if you bought the coverage after the storm was named. In other words, if you have a trip to the Caribbean booked for Sept. 25 and on Sept. 20 a hurricane develops and is named, you generally won’t be able to buy a travel insurance plan Sept. 21 in hopes of getting your money back.

Many plans also don’t cover activities performed under the influence of drugs or alcohol or any extreme sports. If the latter applies to you, you might want to consider a plan with specific coverages for adventure-seekers.

For numerous plans, a few other situations don’t qualify as an acceptable reason to cancel and make a claim, such as fear of travel, medical tourism or pregnancies (unless you booked a trip and bought insurance before you became pregnant or there are complications with the pregnancy). This is where a Cancel For Any Reason add-on to your coverage can be helpful.

You can also run into trouble if you give up on a trip too soon: a minor (or even multihour) flight delay likely isn’t sufficient to cancel your entire trip and get reimbursed through your plan. Be sure to review what requirements your specific plan has when it comes to canceling a trip, claiming trip interruption, etc.

Travel insurance costs vary widely. The final price of your plan will fluctuate based on your age, length of trip and destination.

It will also depend on how much coverage you need, whether you add on specialized policies (like Cancel For Any Reason or pre-existing conditions coverage), whether you plan to participate in extreme sports and other factors.

In our examples above, for instance, the 35-year-old traveler taking a $2,000 trip to Italy would have spent an average $76 for a basic plan to get coverage for things like trip cancellation and interruption, baggage protection, etc. That’s a little less than 4% of the total trip cost — lower than average.

If there were multiple members in a traveling party or if they were going on, say, a rock-climbing or bungee-jumping excursion, the costs would go up.

On average, travel insurance comes to about 5% to 10% of the trip cost. However, considering many of the plans reimburse up to 100% of the trip cost (or more) for disruptions like trip cancellation or interruption, it can be a worthwhile expense if something goes wrong.

It depends. Consider the following factors that might affect your decision: You’re young and healthy, all your bookings are refundable or cancelable without a penalty, your flights are nonstop, you’re not checking bags and a credit card you carry offers some travel protections . In that case, travel insurance might not be necessary.

On the other hand, if you prepaid a large chunk of money for a nonrefundable African safari, you’re going on a Caribbean cruise in the middle of a hurricane season or you’re going somewhere where the cost of health care is high, it’s not a bad idea to buy a travel insurance plan. Here’s how to find the best travel insurance coverage for you.

If you’re thinking of booking a trip and not planning to buy travel insurance, you may want to consider at least booking refundable airfare and not prepaying for hotel, rental car and activity reservations. That way, if something goes wrong, you can cancel without losing any money.

Selecting the best travel insurance policy comes down to your needs, concerns, preferences and budget.

As you book, take a few minutes to consider what most concerns you. Is it getting stranded because of flight trouble? Having the ability to cancel for any reason you see fit without losing money? Getting sick or injured right before departure and needing to postpone the trip? Injuring yourself or falling ill while overseas?

Ultimately, you want a plan that protects you, your money and the large investment in your trip — but doesn’t cost too much, either.

Medical coverage. If your priority is having adequate medical coverage abroad, you might want to look for plans with high limits for medical emergencies and medical evacuation.

Complex travel itinerary. If your itinerary has lots of flight connections, prepaid hotels and deposits for activities you can’t get back, prioritizing a plan with the best coverage for trip cancellations or interruptions may land at the top of your list.

Travel uncertainty. If you’re on the fence about a trip and have nonrefundable reservations, you may want to select a plan with a Cancel For Any Reason coverage option, which can help you recoup about 50% to 75% of the costs. This helps provide peace of mind, placing the decision on whether to travel entirely in your hands.

Car rentals. If you’re renting a car, a collision damage waiver is often worth looking into.

The following destinations are the top insured destinations in 2024, according to Squaremouth (a NerdWallet partner).

The Bahamas.

Costa Rica.

Antarctica.

In 2022, travelers spent about 25.53% more on trips than they did before the pandemic.

As of December, NerdWallet analysis determined travel prices are 10% higher than pre-pandemic. Each statistic makes a strong case for protecting your travel investment as you plan your next trip.

Bookmark these resources to help you make smart money moves as you shop for travel insurance.

What is travel insurance?

CFAR explained.

Is travel insurance worth getting?

10 credit cards that provide travel insurance.

Here is the list of travel cards offered by Chase that include various forms of travel insurance.

Having one of these in your wallet is a good start to protecting your travel investments and preventing expensive accidents; however, savvy travelers check card terms closely and sometimes supplement with a third-party policy, like from one of the companies above, to better protect themselves.

on Chase's website

• Trip delay: Up to $500 per ticket for delays more than 12 hours.

• Trip cancellation: Up to $10,000 per person and $20,000 per trip. Maximum benefit of $40,000 per 12-month period.

• Trip interruption: Up to $10,000 per person and $20,000 per trip. Maximum benefit of $40,000 per 12-month period.

• Baggage delay: Up to $100 per day for five days.

• Lost luggage: Up to $3,000 per passenger.

• Trip delay: Up to $500 per ticket for delays more than 6 hours.

• Trip delay: Up to $500 per trip for delays more than 12 hours.

• Car rentals: Theft and collision damage for most cars in the U.S. and abroad.

• Trip cancellation: Up to $1,500 per person and $6,000 per trip.

• Trip interruption: Up to $1,500 per person and $6,000 per trip.

• Baggage delay: Up to $100 per day for three days.

We used the following factors to choose insurance providers to highlight:

Breadth of coverage: We looked at how many plans each company offered plus the range of their standard plans.

Depth of coverage: We considered two data points to get a sense of how much each company pays out for common travel issues — the maximum caps for trip cancellation and trip interruption claims.

Cost: By looking at the costs for basic coverage across multiple companies, we determined an average cost for shoppers to benchmark plan prices against.

Customizability: While standard plans can cover a lot of ground, sometimes you need something a little more personal.

Customer satisfaction. Using data from Squaremouth when available, and Google Reviews as a backup, we can give kudos to companies with better track records from their clients.

No, it doesn’t necessarily get more expensive the longer you wait to purchase. However, as you put off buying insurance, you may lose access to potential plans and coverage options.

In general, buying travel insurance within a few days to two weeks of prepaying or making an initial deposit for your trip is your best bet. Assuming you’re not booking last-minute, this will provide you with access to the widest possible range of coverage options. It also helps prevent any medical conditions or storms that pop up between booking and buying a plan from ending up as excluded situations, which won’t be covered by your plan.

But, generally, many plans do allow you to buy coverage quite close to your departure date.

To get the most out of your travel insurance plan, buy it soon after making your initial prepayment or deposit to ensure you have access to the biggest menu of plans possible.

Select a plan that’s comprehensive enough to cover the travel scenarios you’re most concerned about or likely to encounter but not too expensive or laden with protections you’d never likely need.

Whatever your coverage, thoroughly review the plan so you understand what’s covered and what’s not, plus how to adhere to the plan’s rules for making a claim.

Travelers frequently use phrases like “trip insurance” and “travel insurance,” as well as “trip protection,” interchangeably, but they do mean different things, according to Stan Sandberg, founder of insurance comparison site TravelInsurance.com.

Trip insurance, or trip protection, generally refers to predeparture (or preevent) coverage if you need to cancel. You may see these plans sold by airlines, online travel agencies or even ticketed event sellers.

“You could refer to it as the portion that protects the investment in the trip,” Sandberg says.

A travel insurance plan typically includes that — plus more comprehensive benefits to protect you during your trip, from medical coverage to trip delay and lost baggage protections, and many more elements, depending on the plan.

Though travel insurance is typically not required for international trips, your personal circumstances will play a key role in whether it’s a good investment.

For instance, young, healthy travelers with few prepaid trip expenses embarking on a relatively risk-free trip may not see a need to buy a plan.

Older travelers with complicated itineraries who are visiting destinations where they could potentially fall ill or get injured — or who could encounter bad weather or some other disrupting factor along the way — may want to buy coverage.

Consider a few key questions:

How well would your health insurance plan cover you if you needed to visit a hospital overseas?

How much did you prepay for a hotel or rental car?

How much money would you be out if weather or some other flight issue derailed your itinerary?

Could you afford an unexpected night in a city where you have a connecting flight?

Do you already have a credit card that provides some travel protections?

Your answers to these questions can help you decide whether you need travel insurance for your international trip.

In general, buying travel insurance

within a few days to two weeks of prepaying or making an initial deposit

for your trip is your best bet. Assuming you’re not booking last-minute, this will provide you with access to the widest possible range of coverage options. It also helps prevent any medical conditions or storms that pop up between booking and buying a plan from ending up as excluded situations, which won’t be covered by your plan.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2024 , including those best for:

Flexibility, point transfers and a large bonus: Chase Sapphire Preferred® Card

No annual fee: Bank of America® Travel Rewards credit card

Flat-rate travel rewards: Capital One Venture Rewards Credit Card

Bonus travel rewards and high-end perks: Chase Sapphire Reserve®

Luxury perks: The Platinum Card® from American Express

Business travelers: Ink Business Preferred® Credit Card

On a similar note...

HelloSafe » Travel Insurance

Best travel insurance in Canada for 2024

comparatorTitles.name

Travel, whether for leisure, business, or work, has become integral to our modern lives. While it opens doors to diverse experiences, travel insurance is crucial in providing peace of mind against unforeseen expenses like medical emergencies and trip disruptions, particularly during unpredictable events.

But choosing the right travel insurance can be a challenge and demands careful consideration of factors like coverage, individual needs, exceptions, and more. We've got you covered.

In this guide, we take you through everything from coverage types and costs to the best plans and how to find cheap travel insurance. You can use our comparator at the top of this page to compare plans, get free quotes , and find a policy that truly fits your needs.

Top 10 travel insurance Canada plans

- soNomad travel insurance: Straightforward and affordable

- Allianz travel insurance: Affordable Plans Starting At $27

- Tugo travel insurance: Tailored solutions

- Destination travel insurance: Specialized coverage

- Manulife travel insurance: Flexible policies

- Blue Cross Travel Insurance Canada: Flexible plans for every need

- CAA travel insurance: Best for CAA members

- RBC travel insurance: Coverage from a reputed bank

- TD travel insurance: High coverage limits

- BCAA travel insurance: Budget-friendly options

Before we explore the best plans in the market, let's look at the basics of this coverage first.

What is travel insurance?

Travel insurance is a policy that protects your investment in a trip. It reimburses for financial losses of a canceled or interrupted trip, as well as emergency medical care during travel, emergency evacuation, damage to a rental car, lost luggage, and more. The medical care component is critical in a country like Canada. Out-of-province care costs more and offers less than in patients' home province.

It takes different forms. You can purchase it as an individual policy or as an add-on to a travel purchase like a flight. It may even be included as a credit card benefit when you use yours to make a travel purchase.

What is international travel insurance?

International travel insurance is a subset of travel insurance, specifically tailored for trips abroad, while the latter can cover domestic and international trips. The key difference is that international coverage is designed to address the unique challenges and risks associated with international journeys, such as medical emergencies, visa issues, and currency exchange, in addition to covering the same aspects as standard travel coverage, like trip cancellations and lost baggage.

How does travel insurance work?

Here's how it typically works:

- Purchase a Policy: Before your trip, you buy a policy, specifying the coverage, trip duration, and other relevant details.

- Traveling: During your trip, if you encounter covered events like medical emergencies, trip cancellations, lost baggage, or other unexpected issues, you can contact your insurance provider or its 24/7 assistance line.

- Claim Submission: Submit a claim with the required documentation, such as medical bills or receipts for lost items, to your insurer for reimbursement.

- Reimbursement: If your claim is approved, the insurance provider reimburses you for eligible expenses, helping you manage unexpected costs and disruptions during your travels.

What does travel insurance cover?

What is covered depends on the insurer and the level of coverage you choose. It commonly covers emergency medical care, trip cancellation, trip interruption, and lost or damaged baggage.

Travel insurance is customized based on the needs of your specific trip. A basic plan covering just flight cancellation may be fine if you already have supplemental individual medical coverage and are traveling within Canada. On the other hand, if you are planning a ski trip to the French Alps, a comprehensive plan with emergency medical care and evacuation back home could help set your mind at ease if you experience a bad fall on the slopes.

Manulife’s CoverMe is one of the most popular providers in Canada, and here is what their Single Trip All-inclusive plan offers:

What does it not cover?

Common exclusions typically include:

- Pre-existing Medical Conditions: Coverage may not extend to pre-existing medical conditions without a specific waiver or rider.

- High-Risk Activities: Activities like extreme sports or dangerous hobbies may require additional coverage or be excluded.

- Traveling Against Advisories: Trips to countries under travel advisories or travel restrictions may not be covered, depending on the policy.

What are the different types of travel insurance?

The most common categories are:

- Baggage insurance - Did you make it to that Caribbean island or European capital, but your luggage did not? It does not have to ruin your trip. This insurance will give you some spending money to get essentials due to a delay or replace it in case it is lost.

- Emergency medical insurance - You cannot put a price on your health. This protects you if you get injured or sick while away.

- Trip cancellation - Have an emergency back home before your trip? If you are unable to travel, this coverage will reimburse what you spent on nonrefundable travel.

- Trip interruption - Miss a connection flight? Maybe you need to return home early? That is okay, you are covered. This is similar to trip cancellation insurance but covers you during a trip rather than before it.

- All-inclusive policies - Want to be prepared for anything? These policies include all of the above insurance types.

Finally, consider how much you will be traveling in the year. Single-trip and annual coverage options exist. Annual plans may save you money if you intend to travel two or more times per year.

What is travel medical insurance?

Travel medical insurance provides coverage for medical emergencies during your trip, including doctor's visits, hospitalization, and emergency medical evacuation. It is a subset of travel insurance, which covers a wider range of risks such as trip cancellations, lost baggage, and non-medical aspects of travel. You can often purchase stand-alone medical coverage if you primarily need health-related coverage for your trip.

How much is travel insurance?

A basic plan for a 30-year-old single traveler could be as little as $26 for a week, while a comprehensive plan could cost that same traveler $125.

How much travel insurance costs depends on the length of your trip, the destination, the desired coverage, and your age. We recommend plans that include emergency medical coverage.

How much is travel insurance in Canada?

On average, a basic single-trip policy for a one-week trip may cost around $25 to $50 CAD for an individual, while an annual multi-trip policy can range from $100 to $300 CAD. More comprehensive coverage or longer trips can increase the cost. Seniors and individuals with pre-existing conditions may pay higher premiums.

It's essential to compare quotes from different providers to find a policy that suits your needs and budget. Try our comparison tool below to get free personalized travel insurance quotes for your upcoming trip. Compare rates, explore options, and find the best policy for you in just seconds.

Prepare for your trip Compare. Choose. Save.

What does travel insurance for seniors cover?

Travel insurance for seniors offers increased medical coverage over other plans and coverage for stable pre-existing conditions. It works like any other emergency medical insurance plan but is adapted to the needs of senior travelers.

Leading plans medical travel insurance for seniors Canada plans offer:

You can use our comparator at the top of this page to find the best Canadian travel insurance for seniors based on their unique needs. It only takes a few steps and you have free quotes in seconds.

How much is travel insurance for Canadian seniors?

The cost of travel insurance for Canadian seniors can vary based on factors like age, health, destination, and trip duration. On average, a comprehensive single-trip policy for a senior traveler may range from $50 to $200 or more, while an annual multi-trip plan could cost approximately $300 to $1,000 or higher, depending on coverage limits and individual circumstances. Pre-existing conditions may also alter the coverage you can access.

What is the best travel insurance for visitors to Canada?

Leading Canadian travel insurance companies offer medical travel insurance to visitors. These can be perfect for non-residents in the country on vacation, business, or visiting family. These plans can be a lifeline for people living in Canada who have not yet qualified for public healthcare.

The best travel insurance for visitors to Canada depends on the traveler’s needs. Additionally, plans may be available to them from their home country.

Is it mandatory to have travel insurance to visit Canada?

No, you do not need private travel coverage to visit Canada. It is not mandatory for all visitors to Canada, but it is highly recommended. Canada's public healthcare system does not cover visitors, and some provinces may require health insurance for entry. Having travel coverage provides financial protection and peace of mind for medical emergencies and unexpected events. Policies and requirements can change, so check with Canadian authorities for the latest information.

Good to know

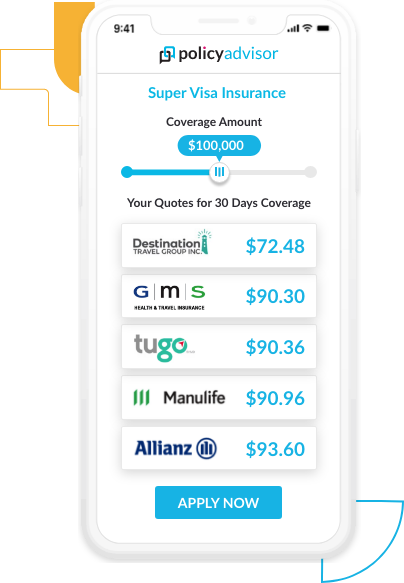

If you are sponsoring a parent or grandparent to visit you in Canada, did you know that you are required to purchase super visa insurance? Learn more and compare the best super visa insurance plan in Canada in our super visa guide .

How to get the cheapest travel insurance Canada plans?

So how to get travel insurance? Most importantly, how to get the most affordable plans? Follow these 5 steps to get the best deals.

- Compare Multiple Quotes: Obtain quotes from various insurance providers to find the best price for your desired coverage.

- Choose Essential Coverage: Select coverage that matches your specific travel needs, avoiding unnecessary add-ons.

- Consider Annual Policies: If you travel frequently, annual policies often offer more value than single-trip coverage.

- Review Deductibles: Higher deductibles can lower your premium, but be prepared to pay more in case of a claim.

- Utilize Membership Discounts: Check if your memberships or affiliations offer discounted coverage options.

While finding the cheapest travel insurance Canada plan or to other regions may seem like a daunting process, we've got you covered. You can simply use our free comparator below to compare plans, and coverage, check on discounts, and get free quotes in no time.

When should I buy travel insurance?

Travel insurance can be purchased anytime between booking and departure, but we recommend buying a plan at the same time that you book your trip.

Booking as soon as possible ensures greater protection. The ideal time to purchase is right after making your initial trip payment, typically within 10-21 days. Buying it early allows you to access coverage for pre-existing medical conditions and other benefits . You can often obtain last-minute insurance up to the day before departure, but some coverages may be limited.

But when is it too late to buy travel insurance? Once you've begun your trip or used any part of it, you generally cannot purchase coverage for trip cancellations or interruptions. However, annual multi-trip policies can be purchased at any time, with coverage beginning from the policy's start date.

What are the best travel insurance plans in 2024?

Please note that the specific coverage, terms, and pricing may vary based on individual circumstances and plan options. It's essential to review the policies in detail and obtain personalized quotes to make an informed decision for your needs. You can do that using our comparator below. Compare multiple plans and get free quotes in no time right here.

Other popular companies include the following :

You can find more on these options by clicking on them:

- AMA travel insurance

- CIBC travel insurance

- Costco travel insurance Canada

- BMO travel insurance (also includes BMO World Elite Mastercard travel insurance)

- Medipac travel insurance

- Medoc travel insurance

- World nomads travel insurance

- Scotiabank travel insurance

What are the FAQs on travel insurance Canada plans?

How does credit card travel insurance work.

Travel coverage is a benefit on many credit cards. It is worth checking what your card includes before purchasing a separate policy. You may already have sufficient coverage.

Credit cards with travel insurance usually only cover expenses purchased on that card. Buy your plane tickets on one card, but the hotel on another? The first company will not reimburse you for a hotel issue. Additionally, terms and exclusions may be more restrictive than a standalone plane. Credit card travel insurance is a wonderful benefit, but weigh whether its coverage is sufficient for you and your trip.

The best travel insurance credit cards have offerings like this:

Does travel insurance cover COVID-19?

Many plans now specifically cover COVID-19 cancellation and medical expenses or offer stand-alone COVID travel insurance. They may reimburse costs incurred from a mandatory quarantine, COVID-19 medical expenses, and trip interruption and cancellation . Some specific COVID plans only cover COVID-19 expenses and do not automatically include coverage for other medical needs.

It is worth verifying details carefully before deciding on a Covid-19 travel insurance policy. Covid-19 coverage and news change frequently, so check with your service providers for the latest information.

There are a few important points to consider:

- Coverage may be explicitly excluded in your policy if the destination countries or regions are under an “avoid non-essential travel” or “avoid all travel” advisory at the time of purchase.

- Your Covid-19 vaccination status may affect your coverage. If you are unvaccinated by choice, your insurer may declare your claims ineligible.

Do I need private health care coverage when traveling outside Canada?

Yes, we always recommend travel medical insurance when traveling abroad. Healthcare prices and standards can be very different while traveling. Some public provincial plans offer some coverage, but it may be insufficient. Your provincial plan covers may only pay what the cost would be back at home, not the actual price at your destination. Even then, you likely have to pay out-of-pocket and request reimbursement later.

In some countries, healthcare facilities may request treatment upfront. They may refuse treatment if you are unable to pay. This alone makes emergency medical insurance extremely valuable.

Do I need travel insurance to USA from Canada?

Getting a private travel protection plan is highly recommended when traveling from Canada to the USA, as it provides essential medical coverage. Medical expenses in the USA can be exorbitant, and without insurance, a simple hospital visit can lead to substantial bills, potentially running into thousands of dollars.

For example, a basic emergency room visit for minor treatment might cost around $1,000 to $2,000 , while more serious medical procedures or surgeries can lead to bills that range from $10,000 to tens of thousands of dollars, or even more for complex surgeries or prolonged hospital stays.

Do I need travel insurance within Canada?

We recommend getting medical travel insurance Canada plans while traveling within the country. Specific plans are available for domestic travelers. While Canadian citizens and residents are guaranteed basic emergency care by the Canada Health Act, this does not include prescription drugs and ambulance services. Your OHIP coverage from Ontario will not cover you for a private hospital, laboratory, or paramedic services while visiting British Columbia.

Additionally, payment for medical services may be required upfront, leaving you responsible for seeking reimbursement from your home province upon your return. Canadian residents traveling within Canada may qualify for a discount on their medical travel insurance.

When traveling outside of your province or territory without adequate coverage, you assume risk. Note that you may already have sufficient coverage if you have a supplemental individual or group private health insurance policy.

Want to protect yourself while traveling in Canada? Compare the best travel insurance medical plans anonymously today using our comparator at the top of this page.

What does travel insurance for snowbirds cover?

Travel medical insurance for snowbirds commonly covers the following medical expenses:

- Medical treatments

- Prescription medications

- Paramedics and ambulance rides

- Repatriation to Canada

- Emergency dental care

Snowbird insurance policies do not usually cover elective treatments. Those should wait until you have returned to Canada.

But who are Snowbirds? Snowbirds are people who travel to warmer climates during the cold Canadian winter. They are usually retirees. Therefore, getting adequate protection for their travels is particularly important for these groups. Many of them go to warm parts of the United States, the country with the world’s highest medical care costs.

Snowbirds may be more at risk for a medical emergency while away due to the length of their trips and underlying health conditions.

To learn more, see our guide to snowbird travel insurance.

How do I buy travel insurance online?

The easiest way to purchase a travel plan is by using an online comparison tool like ours. See rates and coverage options quickly without giving up personal data. Alternatively, you may purchase it through an agent, a broker, your private individual or group health insurer, or a travel credit card.

How much travel insurance do I need?

The amount of coverage you need depends on various factors, including the destination, duration, and activities of your trip. As a general guideline, consider coverage for emergency medical expenses, trip cancellations, and lost baggage.

Aim for a coverage amount that provides financial protection for potential unexpected costs while keeping your budget and specific travel plans in mind. It's essential to balance adequate protection with affordability.

What is the best travel insurance for cancer patients?

The best protection plan for cancer patients depends on individual circumstances, including the stage of cancer and current health. It's advisable to look for insurance providers that specialize in covering pre-existing medical conditions, offer comprehensive coverage, and have experience handling cancer-related claims.

Companies like Allianz and IMG Global among others often provide options for travelers with pre-existing conditions, including cancer*. However, it's essential for cancer patients to compare policies, disclose their medical history accurately, and consider consulting their healthcare providers when selecting the most suitable coverage.

Does travel insurance cover cruises?

Yes, travel coverage plans frequently cover cruises. When shopping for a plan, be sure to verify that yours offers cruise coverage. To give an example, RBC offers two popular examples, their Deluxe and TravelCare (for seniors) packages.

They cover:

- Cruise cancellation or interruption due to mechanical failure or weather

- Catch-up costs for a missed departure due to a canceled flight

- Unused shore excursion tickets (due to illness or injury)

- Last-minute cancellations due to a covered reason

- Lost luggage, passports, and medications

- Eligible emergency medical expenses

- 24-hour worldwide emergency medical and travel assistance

- Repatriation costs

See our guides on travel insurance in Canada:

- Is soNomad insurance best for you? Review 2024

- Is Red Cross Travel Insurance Good in 2024?

- Best Travel Insurance South Africa Plans 2024

- Expat Travel Insurance: A Complete Guide (2024)

- What is the best Travel Insurance Hong Kong for 2024?

- What is Canada's best travel health insurance (2024)?

- What are the Best Travel Insurance BC Plans in 2024?

- Best Travel Insurance Dubai Plans for Canadians (2024)

- What is the best group travel insurance in 2024?

- Best Travel Insurance for Backpackers 2024

- Travel Insurance UK: Complete Guide (2024)

- Annual Travel Insurance Canada: Full Guide 2024

- Travel Insurance for Schengen Visa: 2024 Guide

- How does Multi Trip Travel Insurance work? Full guide 2024

- How does student travel insurance work? A full guide 2024

- Is CoverMe Travel Insurance worth it? Review 2024

- Is Air Canada travel insurance worth it? 2024 Review

- Is Cooperators Travel Insurance worth it? Review 2024

- How to get the best European travel insurance in 2024?

- Is Sun Life Travel Insurance the best in 2024? Review

- Is Canada Life Travel Insurance worth it? Review 2024

- How to get travel insurance for visitors to Canada in 2024?

- Is TuGo Travel Insurance right for you? Review 2024

- Is World Nomads travel insurance the best in 2024?

- Is Green Shield travel insurance the best in 2024?

- Is RIMI travel insurance the best in 2024?

- Is MEDOC Travel Insurance the best in 2024?

- Is Travel Guardian insurance the best in 2024?

- Is Costco Travel Insurance worth it? Review 2024

- Is WestJet Travel Insurance the Best in 2024?

- How to get the best travel Insurance for seniors in 2024?

- Is Blue Cross Travel Insurance in Canada worth it? 2024 Review

- How does trip cancellation insurance work in Canada in 2024?

- Should you buy travel insurance to the USA?

- Is RBC travel insurance the best in 2024?

- Is AIG Travel Insurance Canada Good? Review 2024

- [Map] In which countries of the world is it common to tip and how much?

- Is PC Financial travel Insurance good? Review 2024

- Which is the best Credit Card with Travel Insurance in 2024?

- Is TD travel insurance the best in ?

- Is CIBC travel insurance the best in ?

- Is BMO travel insurance the best in ?

- Is Scotiabank travel insurance the best in ?

- Is Medipac travel insurance the best in ?

- Is Johnson travel insurance the best in ?

- Is Goose travel insurance the best in ?

- Is GMS travel insurance the best in ?

- Is CARP travel insurance the best in ?

- Is BCAA travel insurance the best in ?

- Is 21st Century travel insurance the best in ?

- Is Desjardins travel insurance the best in 2024?

- Is AMA travel insurance worth it in 2024?

- Is Allianz travel insurance the best in 2024?

- Is Manulife travel insurance the best in 2024?

- Is CAA the best travel insurance in Canada in 2024?

- [Survey] Only 25% of Canadians plan to go on holiday this summer

- [Survey] Only 29% of Ontarians plan to go on holiday this summer

- What is the best Covid travel insurance in Canada for 2024?

- [Travel] Covid travel insurance still mandatory in 41 countries across the world this summer

- What's the best Super Visa insurance in Canada for 2024?

- [Survey] The pandemic has reduced the desire to travel for over 51% of Canadians

- Best travel insurance for snowbirds in 2024

- [Map] How is the vaccination passport applied worldwide?

- [Tourism] Another $ 52 billion loss for the industry across Canada in 2021 compared to 2019

- Where Can Canadians Still Travel Abroad ?

Alexandre Desoutter has been working as editor-in-chief and head of press relations at HelloSafe since June 2020. A graduate of Sciences Po Grenoble, he worked as a journalist for several years in French media, and continues to collaborate as a as a contributor to several publications.

This message is a response to . Cancel

I have had BCAA travel insurance in the past and nothing has changed regarding my medical needs. Am I able to apply for insurance without having to go through all the questions again?

Hi Marylou, Thank you for reaching out to us. You should be able to renew your policy without having to go through the whole process again. Here is a link to help you with the same. https://www.bcaa.com/Apps/Travel/FullTravelMedical/Renewal Please feel free to reach out to us if you have any further doubts. Thank you!

I am wanting a quote for travel/medical insurance

Hi Patricia, You can use the comparator tool at the top of the page to find the perfect insurance policy for you. You can then contact the company of your choice directly to get a quote.

Have a nice day, The HelloSafe team

If we go to Portugal for one week and France for another, do we buy separate insurance?

Hi Julie, It depends. Some insurances contracts cover any trips in a given period, while others are meant to cover a specific destination. You can use the comparison tool at the top of the page to find the perfect contract for you and ask for a quote.

Hello, how are you? Does travel insuance covering breast biospys overseas?

Hi Nour, Each travel insurance covers different medical services. Please contact the insurer of your choice for more detail about a potential contract.

Does anybody ever answer the phone at caa Ins. Tried several times and waited half hr or more with no response. I am member but find this very irritating.

Hi Brian, We are not related to CAA Insurance and therefore we cannot help you.

The Best Travel Insurance for Canadians: Short and Long-Term Options

Wanting peace of mind from unexpected costs, we always buy travel insurance when travelling outside of Canada.

I recently spent a lot of time researching travel insurance for Canadians, primarily for an upcoming four month long multi-destination trip.

It was a much longer process than I initially expected! This post provides a shortcut to the results of my research.

While the main focus is travel insurance options for Canadians , I will also share some travel insurance basics.

I also felt it was important to list some specific travel insurance considerations for Canadian travellers that I don’t often see mentioned.

Insurance is never going to be an exciting topic but I hope I can help reduce the amount of time you spend thinking about it!

Published February 2024 . There are affiliate links in this post. If you make a purchase via one of these links, we may receive a percentage of the sale.

Travel insurance basics

Before delving into the specifics of travel insurance for Canadians, I’d like to quickly touch on some insurance basics.

If you’re new to buying travel insurance, the terminology can be a little confusing. And since there is a lot of small print involved with every policy, it’s essential to understand what you are actually purchasing.

When searching for insurance as a Canadian, you’ll soon notice two types of coverage:

- Emergency medical

- Trip cancellation, interruption, delays and lost baggage

As you may guess, the first type provides coverage for emergency medical expenses while travelling outside of Canada. I always buy a policy with at least $5 million of coverage.

Emergency medical policies usually also include coverage for medical evacuations to Canada and repatriation in case of death (the return of your remains).

The second type of insurance provides coverage in the event you need to cancel the trip, return early, or stay longer than planned.

This kind of insurance typically also includes coverage for baggage that is lost, damaged or stolen during your trip.

The cost of trip cancellation travel insurance is usually tied to the overall cost of your trip. It can be purchased separately or bundled together with an emergency medical insurance policy.

Single, annual/multiple-trip or long-term?

- Single-trip travel insurance covers one trip to a destination (or destinations) and ends when you return home

- Multi-trip travel insurance covers multiple short trips (usually 30 days or less) within 12 months. It is also referred to as an annual travel insurance policy. Multi-trip policies can be a money saver for people travelling twice or more a year

- Long-term travel insurance has a loose definition, but it generally refers to a policy that is between 30 days and 1 year in length (or longer)

Pre-existing conditions

Travel insurance providers usually exclude pre-existing conditions from coverage.

So if you have medical conditions or are currently going through a diagnosis process, be aware that you may not be able to claim for any potential medical costs related to your pre-existing condition .

Some insurers do cover pre-existing conditions, as long as there have been no recent changes (i.e. the condition being treated and is considered stable).

Policies that cover pre-existing conditions are usually more expensive than those that do not. Always contact the insurance provider if you’re unsure.

Depending on your age, you may need to complete a medical questionnaire when applying for travel insurance.

Deductibles

A deductible is the amount of money you will have to pay before the travel insurance provider will cover the balance of the claim.

The lower the deductible on a policy, the higher the initial purchase price. The ductible is sometimes referred to as an ‘excess.’

I prefer to buy insurance with the lowest deductible possible. We are lucky and have only ever had to claim for small amounts on travel insurance (less than $1,000). I like knowing that these ‘small amounts’ are covered as they can add up, especially on longer trips.

Important considerations: travel insurance for Canadians

There are some unique considerations to keep in mind when searching for travel insurance as a Canadian.

As a relatively new Canadian citizen, I would have no idea about these issues if I had not read the small print of travel insurance policies!

Provincial healthcare eligibility

Most Canadian travel insurance policies require you to have valid provincial healthcare coverage for the length of your intended trip.

If you do not have provincial healthcare coverage and purchase a travel insurance policy that requires it, it is unlikely that you will be able to claim for emergency medical costs.

Each province and territory has different eligibility criteria for provincial healthcare coverage.

For example, British Columbia requires residents ‘ to be physically present in BC for at least six months in a calendar year. ‘ There is the possibility to extend this time, but only on a limited basis (up to 24 months once in a five-year period).

If you are Canadian but primarily resident in another country (and hence not covered by the provincial healthcare system), I would suggest researching insurance providers in the country you currently live in.

Live in the UK or EU? Consider purchasing a policy with True Traveller . To buy a policy with True Traveller, you must have a residential address and the ‘unrestricted and unconditional right of entry’ to the country you currently live in.

Starting a trip from your home province

Another important condition featured in the ‘small print’ of most Canadian travel insurance policies is the requirement to start your trip from your home province.

For most Canadian travellers this clause doesn’t present any issue. The vast majority of people start their travel trip from home.

But if you plan to visit friends or family in another province or territory before leaving on your trip, be sure to find an appropriate insurance policy for you.

This is also important if you plan to fly internationally from a different province than the one you live in, especially if you need to travel a long distance to reach the airport (or stay overnight).